Exam 24: Aggregate Demand and Aggregate Supply Analysis

Exam 1: Economics: Foundations and Models444 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System498 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply475 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes419 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods266 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply295 Questions

Exam 7: The Economics of Health Care334 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance278 Questions

Exam 9: Comparative Advantage and the Gains From International Trade379 Questions

Exam 10: Consumer Choice and Behavioral Economics302 Questions

Exam 11: Technology, Production, and Costs330 Questions

Exam 12: Firms in Perfectly Competitive Markets298 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting276 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets262 Questions

Exam 15: Monopoly and Antitrust Policy271 Questions

Exam 16: Pricing Strategy263 Questions

Exam 17: The Markets for Labor and Other Factors of Production286 Questions

Exam 18: Public Choice, Taxes, and the Distribution of Income258 Questions

Exam 19: GDP: Measuring Total Production and Income266 Questions

Exam 20: Unemployment and Inflation292 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles257 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies268 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run306 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis284 Questions

Exam 25: Money, Banks, and the Federal Reserve System280 Questions

Exam 26: Monetary Policy277 Questions

Exam 27: Fiscal Policy303 Questions

Exam 28: Inflation, Unemployment, and Federal Reserve Policy257 Questions

Exam 29: Macroeconomics in an Open Economy278 Questions

Exam 30: The International Financial System262 Questions

Select questions type

Explain the three reasons the aggregate demand curve slopes downward.

(Essay)

4.8/5  (39)

(39)

Article Summary

According to the International Energy Agency (IEA), increased oil production resulting from U.S. shale oil has invigorated the North American oil industry and has created a global supply shock. The shale oil and gas industry has generated tens of billions of dollars in revenues and hundreds of thousands of new jobs, and could result in the United States changing from being the world's largest oil importer to a net exporter within a few years. An IEA forecast predicts that because of shale oil, the United States will become the world's largest oil producer by 2017, with supply growing by 3.9 million barrels per day from 2012-2018.

Source: Denise Roland, and AFP, "US shale energy creates global oil 'supply shock'," Telegraph, May 14, 2013.

-Refer to the Article Summary. The supply shock mentioned in the article summary may well result in a decrease in the price of oil. After an unexpected decrease in the price of oil, the long-run adjustment ________ the price level and ________ the unemployment rate as they return to their original levels.

(Multiple Choice)

4.9/5 (33)

The proponents of rational expectations and monetarism think that the Federal Reserve should adopt

(Multiple Choice)

4.8/5 (34)

The process of an economy adjusting from a recession back to potential GDP in the long run without any government intervention is known as

(Multiple Choice)

4.9/5 (39)

Which of the following is one explanation as to why the aggregate demand curve slopes downward?

(Multiple Choice)

4.8/5 (29)

Stagflation occurs when aggregate supply and aggregate demand both increase.

(True/False)

4.8/5 (38)

The recession of 2007-2009 made many consumers pessimistic about their future incomes. How does this increased pessimism affect the aggregate demand curve?

(Multiple Choice)

4.9/5 (36)

When the economy enters a recession, your employer is unlikely to reduce your wages because ________ during a recession.

(Multiple Choice)

4.8/5 (36)

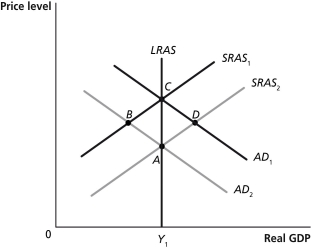

Figure 24-3  -Refer to Figure 24-3. Which of the points in the above graph are possible short-run equilibria but not long-run equilibria? Assume that Y1 represents potential GDP.

-Refer to Figure 24-3. Which of the points in the above graph are possible short-run equilibria but not long-run equilibria? Assume that Y1 represents potential GDP.

(Multiple Choice)

4.8/5 (38)

When the price of oil rises unexpectedly, the equilibrium price level ________ and the unemployment rate ________ in the short run.

(Multiple Choice)

4.8/5 (38)

________ of unemployment during ________ make it easier for workers to ________ wages.

(Multiple Choice)

4.9/5 (37)

Figure 24-3

-Refer to Figure 24-3. Which of the points in the above graph are possible short-run equilibria?

(Multiple Choice)

4.9/5 (38)

Just before, during, and after the recession of 2007-2009, net exports in the United States

(Multiple Choice)

4.8/5 (33)

An increase in government spending will result in an increase in the price level and an increase in real GDP in the long run.

(True/False)

4.9/5 (29)

Forecasts made by White House economists and economists at the Congressional Budget Office in 2011 projected that real GDP

(Multiple Choice)

4.7/5 (32)

The invention of the cotton gin ushered in the Industrial Revolution and began a long period of technological innovation. What did this technological change do the short-run supply curve?

(Multiple Choice)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)