Exam 1: Economics: Foundations and Models

Exam 1: Economics: Foundations and Models444 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System498 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply475 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes419 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods266 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply295 Questions

Exam 7: The Economics of Health Care334 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance278 Questions

Exam 9: Comparative Advantage and the Gains From International Trade379 Questions

Exam 10: Consumer Choice and Behavioral Economics302 Questions

Exam 11: Technology, Production, and Costs330 Questions

Exam 12: Firms in Perfectly Competitive Markets298 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting276 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets262 Questions

Exam 15: Monopoly and Antitrust Policy271 Questions

Exam 16: Pricing Strategy263 Questions

Exam 17: The Markets for Labor and Other Factors of Production286 Questions

Exam 18: Public Choice, Taxes, and the Distribution of Income258 Questions

Exam 19: GDP: Measuring Total Production and Income266 Questions

Exam 20: Unemployment and Inflation292 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles257 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies268 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run306 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis284 Questions

Exam 25: Money, Banks, and the Federal Reserve System280 Questions

Exam 26: Monetary Policy277 Questions

Exam 27: Fiscal Policy303 Questions

Exam 28: Inflation, Unemployment, and Federal Reserve Policy257 Questions

Exam 29: Macroeconomics in an Open Economy278 Questions

Exam 30: The International Financial System262 Questions

Select questions type

You explain to your friend Haslina, who runs a catering service called "Meals in a Zip", about an economic theory which asserts that consumers will purchase less of a product at higher prices than they will at lower prices. She contends that the theory is incorrect because over the past two years she has raised the price of her catered meals and yet has seen a brisk increase in sales. How would you respond to Haslina?

(Multiple Choice)

4.9/5  (29)

(29)

Suppose a doctor can earn an additional $25,000 in revenue per year by keeping her office open on Sundays. At what additional cost would keeping the office open on Sundays not be considered economically rational?

(Essay)

4.9/5 (37)

Scenario 1-1

Suppose a cell phone manufacturer currently sells 20,000 cell phones per week and makes a profit of $5,000 per week. A manager at the plant observes, "Although the last 3,000 cell phones we produced and sold increased our revenue by $6,000 and our costs by $6,700, we are still making an overall profit of $5,000 per week so I think we're on the right track. We are producing the optimal number of cell phones."

-Refer to Scenario 1-1. Had the firm not produced and sold the last 3,000 cell phones, would its profit be higher or lower, and if so by how much?

(Multiple Choice)

4.7/5 (34)

The decision about what goods and services will be produced made in a centrally-planned economy is made by

(Multiple Choice)

4.9/5 (40)

Scenario 1-4

Suppose a cigar manufacturer currently sells 1,500 cigars per week and makes a profit of $3,000 per week. The plant foreman observes, "Although the last 500 cell cigars we produced and sold increased our revenue by $7,500 and our costs by $7,000, we are only making an overall profit of $3,000 per week so I think we need to cut back on production."

-Refer to Scenario 1-4. Had the firm not produced and sold the last 500 cigars, would its profit be higher or lower, and if so by how much?

(Multiple Choice)

4.8/5 (38)

An economic ________ is a simplified version of some aspect of economic life used to analyze an economic issue.

(Multiple Choice)

4.8/5 (39)

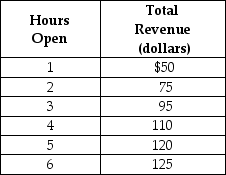

Table 1-1

Lydia runs a small nail salon in the town of New Hope. She is debating whether she should extend her hours of operation. Lydia figures that her sales revenue will depend on the number of hours the nail salon is open as shown in the table above. She would have to hire a worker for those hours at a wage rate of $10 per hour.

-Refer to Table 1-1. Using marginal analysis, how many hours should Lydia extend her nail salon's hours of operations?

Lydia runs a small nail salon in the town of New Hope. She is debating whether she should extend her hours of operation. Lydia figures that her sales revenue will depend on the number of hours the nail salon is open as shown in the table above. She would have to hire a worker for those hours at a wage rate of $10 per hour.

-Refer to Table 1-1. Using marginal analysis, how many hours should Lydia extend her nail salon's hours of operations?

(Multiple Choice)

4.8/5 (47)

Which of the following statements about economic resources is false?

(Multiple Choice)

4.9/5 (37)

The term "market" refers to trading arrangements by which buyers and sellers come together.

(True/False)

4.8/5 (43)

Scenario 1-3

Suppose a t-shirt manufacturer currently sells 5,000 t-shirts per week and makes a profit of $10,000 per week. A manager at the plant observes, "Although the last 400 t-shirts we produced and sold increased our revenue by $4,000 and our costs by $4,800, we are still making an overall profit of $10,000 per week so I think we're on the right track. We are producing the optimal number of t-shirts."

-Refer to Scenario 1-3. Using marginal analysis terminology, what is another economic term for the incremental cost of producing the last 400 t-shirts?

(Multiple Choice)

5.0/5 (35)

Which of the following is an example of a "how much" decision?

(Multiple Choice)

4.8/5 (41)

In economics, activities done for others, such as providing house cleaning or dental work, are referred to as

(Multiple Choice)

4.8/5 (34)

Which of the following is an example of an activity undertaken by an entrepreneur?

(Multiple Choice)

4.9/5 (33)

Which of the following statements about economic resources is true?

(Multiple Choice)

4.7/5 (34)

In a market economy, those who are willing and able to buy what is produced

(Multiple Choice)

4.8/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)