Exam 13: Monopolistic Competition: The Competitive Model in a More Realistic Setting

Exam 1: Economics: Foundations and Models142 Questions

Exam 2: Trade-Offs, comparative Advantage, and the Market System152 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply149 Questions

Exam 4: Economic Efficiency, government Price Setting, and Taxes137 Questions

Exam 5: Externalities, environmental Policy, and Public Goods139 Questions

Exam 6: Elasticity: The Responsiveness of Demand and Supply149 Questions

Exam 7: The Economics of Health Care117 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance140 Questions

Exam 9: Comparative Advantage and the Gains From International Trade124 Questions

Exam 10: Consumer Choice and Behavioral Economics154 Questions

Exam 11: Technology, production, and Costs174 Questions

Exam 12: Firms in Perfectly Competitive Markets153 Questions

Exam 13: Monopolistic Competition: The Competitive Model in a More Realistic Setting137 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets129 Questions

Exam 15: Monopoly and Antitrust Policy148 Questions

Exam 16: Pricing Strategy134 Questions

Exam 17: The Markets for Labor and Other Factors of Production149 Questions

Exam 18: Public Choice, taxes, and the Distribution of Income134 Questions

Exam 19: GDP: Measuring Total Production and Income135 Questions

Exam 20: Unemployment and Inflation148 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles130 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies134 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run157 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis145 Questions

Exam 25: Money, banks, and the Federal Reserve System144 Questions

Exam 26: Monetary Policy145 Questions

Exam 27: Fiscal Policy155 Questions

Exam 28: Inflation, unemployment, and Federal Reserve Policy135 Questions

Exam 29: Macroeconomics in an Open Economy145 Questions

Exam 30: The International Financial System139 Questions

Select questions type

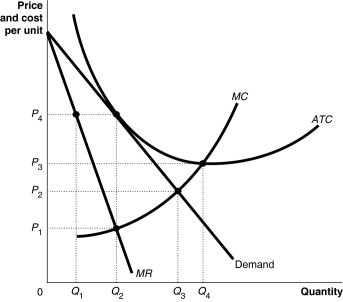

Figure 13-6  -Refer to Figure 13-6.What is the productively efficient output for the firm represented in the diagram?

-Refer to Figure 13-6.What is the productively efficient output for the firm represented in the diagram?

(Multiple Choice)

4.8/5  (38)

(38)

Why do most firms in monopolistic competition typically make zero profit in the long run?

(Multiple Choice)

4.8/5 (35)

A monopolistically competitive firm earning profits in the short run will find the demand for its product decreasing and becoming more elastic in the long run as new firms move into the industry until

(Multiple Choice)

4.9/5 (37)

Figure 13-6

-Refer to Figure 13-6.What is the amount of excess capacity?

(Multiple Choice)

4.8/5 (28)

Figure 13-13  -Refer to Figure 13-13.Assume Starbucks is successful with its new health and wellness stores,and as a result it is able to earn economic profits.Which of the graphs in the figure above reflects this?

-Refer to Figure 13-13.Assume Starbucks is successful with its new health and wellness stores,and as a result it is able to earn economic profits.Which of the graphs in the figure above reflects this?

(Multiple Choice)

5.0/5 (37)

Figure 13-12  -Refer to Figure 13-12 to answer the following questions.

a.What is the productively efficient output?

b.What is the allocatively efficient output?

c.What is the amount of excess capacity?

d.Suppose the firm is currently producing 14 units.What happens if it increases output to 17 units?

-Refer to Figure 13-12 to answer the following questions.

a.What is the productively efficient output?

b.What is the allocatively efficient output?

c.What is the amount of excess capacity?

d.Suppose the firm is currently producing 14 units.What happens if it increases output to 17 units?

(Essay)

4.8/5 (41)

For a profit-maximizing monopolistically competitive firm,for the last unit sold,the marginal cost of production is less than the marginal benefit received by a customer from the purchase of that unit.

(True/False)

4.8/5 (36)

A successful trademark is one that becomes a generic name for a product,for example,"Kleenex" has become a generic term for tissues.

(True/False)

4.8/5 (40)

Recent research has shown that the first firm to enter a market often does not have a long-term advantage over later entrants into the market.An example that has been used to illustrate this is

(Multiple Choice)

4.8/5 (30)

If a monopolistically competitive firm breaks even,the firm

(Multiple Choice)

4.8/5 (24)

When a monopolistically competitive firm cuts its price to increase its sales,it experiences a loss in revenue due to the income effect and a gain in revenue due to the substitution effect.

(True/False)

4.9/5 (33)

Assume that price exceeds average variable cost over the relevant range of demand.If a monopolistically competitive firm is producing at an output where marginal revenue is $111.11 and marginal cost is $118,then to maximize profits the firm should increase its output.

(True/False)

4.8/5 (37)

As customers switch from renting DVDs to downloading or streaming movies from the Internet,Netflix will likely find it ________ to remain profitable as they face ________ competition with streaming movies than with mail order DVD rental.

(Multiple Choice)

4.9/5 (40)

Is a monopolistically competitive firm productively efficient?

(Multiple Choice)

4.9/5 (36)

One reason why the coffeehouse market is competitive is that

(Multiple Choice)

4.8/5 (28)

Consumers in monopolistically competitive markets face a tradeoff between paying prices greater than marginal costs and purchasing products that are more closely suited to their tastes.

(True/False)

4.8/5 (41)

In theory,in the long run,monopolistically competitive firms earns zero profits.However,in reality there are some ways by which a firm can avoid losing profits.Which of the following is one such way?

(Multiple Choice)

4.8/5 (35)

A monopolistically competitive industry that earns economic profits in the short run will be able to expand its market share even if the market size remains constant.

(True/False)

4.7/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)