Exam 13: Monopolistic Competition: The Competitive Model in a More Realistic Setting

Exam 1: Economics: Foundations and Models142 Questions

Exam 2: Trade-Offs, comparative Advantage, and the Market System152 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply149 Questions

Exam 4: Economic Efficiency, government Price Setting, and Taxes137 Questions

Exam 5: Externalities, environmental Policy, and Public Goods139 Questions

Exam 6: Elasticity: The Responsiveness of Demand and Supply149 Questions

Exam 7: The Economics of Health Care117 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance140 Questions

Exam 9: Comparative Advantage and the Gains From International Trade124 Questions

Exam 10: Consumer Choice and Behavioral Economics154 Questions

Exam 11: Technology, production, and Costs174 Questions

Exam 12: Firms in Perfectly Competitive Markets153 Questions

Exam 13: Monopolistic Competition: The Competitive Model in a More Realistic Setting137 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets129 Questions

Exam 15: Monopoly and Antitrust Policy148 Questions

Exam 16: Pricing Strategy134 Questions

Exam 17: The Markets for Labor and Other Factors of Production149 Questions

Exam 18: Public Choice, taxes, and the Distribution of Income134 Questions

Exam 19: GDP: Measuring Total Production and Income135 Questions

Exam 20: Unemployment and Inflation148 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles130 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies134 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run157 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis145 Questions

Exam 25: Money, banks, and the Federal Reserve System144 Questions

Exam 26: Monetary Policy145 Questions

Exam 27: Fiscal Policy155 Questions

Exam 28: Inflation, unemployment, and Federal Reserve Policy135 Questions

Exam 29: Macroeconomics in an Open Economy145 Questions

Exam 30: The International Financial System139 Questions

Select questions type

Economists agree that a monopolistically competitive market structure

(Multiple Choice)

4.8/5  (36)

(36)

Productive efficiency does not hold for a profit-maximizing,monopolistically competitive firm in the long-run equilibrium because the firm operates along the diseconomies-of-scale region of its average total cost curve.

(True/False)

4.9/5 (37)

If Starbucks is successful at luring away competitor's customers with its new health and wellness stores,what will be the effect on Starbucks' demand and marginal revenue curves?

(Multiple Choice)

4.8/5 (29)

What is the difference between zero accounting profit and zero economic profit?

(Essay)

4.9/5 (33)

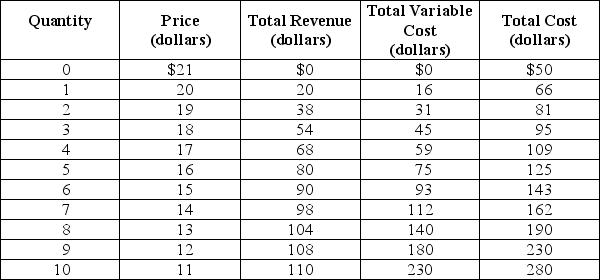

Table 13-3

Table 13-3 shows the demand and cost schedules for a monopolistically competitive firm.

-Refer to Table 13-3.What is the amount of the firm's loss at its optimal output level?

Table 13-3 shows the demand and cost schedules for a monopolistically competitive firm.

-Refer to Table 13-3.What is the amount of the firm's loss at its optimal output level?

(Multiple Choice)

4.9/5 (37)

Table 13-3

Table 13-3 shows the demand and cost schedules for a monopolistically competitive firm.

-Refer to Table 13-3.What is the best course of action for the firm in the short run?

(Multiple Choice)

4.8/5 (40)

Which of the following is true of a typical firm in a monopolistically competitive industry?

(Multiple Choice)

4.8/5 (35)

If buyers of a monopolistically competitive product feel the products of different sellers are strongly differentiated,then the demand for each seller's product is

(Multiple Choice)

4.8/5 (27)

You have just opened a new Italian restaurant in your hometown where there are three other Italian restaurants.Your restaurant is doing a brisk business and you attribute your success to your distinctive northern Italian cuisine using locally grown organic produce.What is likely to happen to your business in the long run?

(Multiple Choice)

4.9/5 (32)

Which of the following is an example of a factor that a firm's owners and managers can control in making the firm successful?

(Multiple Choice)

4.8/5 (34)

A firm that is first to the market with a new product frequently discovers that there are design flaws or problems with the product that were not anticipated.How do these problems affect the innovating firm?

(Multiple Choice)

4.8/5 (35)

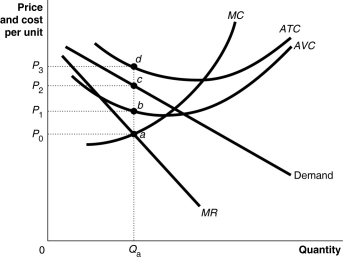

Figure 13-7  Figure 13-7

shows short-run cost and demand curves for a monopolistically competitive firm in the market for designer watches.

-Refer to Figure 13-7.If the diagram represents a typical firm in the designer watch market,what is likely to happen in the long run?

Figure 13-7

shows short-run cost and demand curves for a monopolistically competitive firm in the market for designer watches.

-Refer to Figure 13-7.If the diagram represents a typical firm in the designer watch market,what is likely to happen in the long run?

(Multiple Choice)

5.0/5 (25)

How does the long run equilibrium of a monopolistically competitive industry differ from that of a perfectly competitive industry?

(Multiple Choice)

4.7/5 (40)

A major difference between monopolistic competition and perfect competition is

(Multiple Choice)

4.7/5 (43)

Arturo runs a Taco Bell franchise.He is selling 250 Gordita Supremes per week at a price of $2.75.If he lowers the price to $2.70,he will sell 251 Gordita Supremes.What is the marginal revenue of the 251st Gordita Supreme? If selling the extra Gordita Supreme adds $0.20 to Arturo's costs,what will be the effect on his profit from selling 251 Gordita Supremes instead of 250?

(Essay)

4.8/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)