Exam 1: Economics: Foundations and Models

Exam 1: Economics: Foundations and Models142 Questions

Exam 2: Trade-Offs, comparative Advantage, and the Market System152 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply149 Questions

Exam 4: Economic Efficiency, government Price Setting, and Taxes137 Questions

Exam 5: Externalities, environmental Policy, and Public Goods139 Questions

Exam 6: Elasticity: The Responsiveness of Demand and Supply149 Questions

Exam 7: The Economics of Health Care117 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance140 Questions

Exam 9: Comparative Advantage and the Gains From International Trade124 Questions

Exam 10: Consumer Choice and Behavioral Economics154 Questions

Exam 11: Technology, production, and Costs174 Questions

Exam 12: Firms in Perfectly Competitive Markets153 Questions

Exam 13: Monopolistic Competition: The Competitive Model in a More Realistic Setting137 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets129 Questions

Exam 15: Monopoly and Antitrust Policy148 Questions

Exam 16: Pricing Strategy134 Questions

Exam 17: The Markets for Labor and Other Factors of Production149 Questions

Exam 18: Public Choice, taxes, and the Distribution of Income134 Questions

Exam 19: GDP: Measuring Total Production and Income135 Questions

Exam 20: Unemployment and Inflation148 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles130 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies134 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run157 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis145 Questions

Exam 25: Money, banks, and the Federal Reserve System144 Questions

Exam 26: Monetary Policy145 Questions

Exam 27: Fiscal Policy155 Questions

Exam 28: Inflation, unemployment, and Federal Reserve Policy135 Questions

Exam 29: Macroeconomics in an Open Economy145 Questions

Exam 30: The International Financial System139 Questions

Select questions type

The revenue received from the sale of ________ of a product is a marginal benefit to the firm.

(Multiple Choice)

4.9/5  (47)

(47)

Recent changes occurring within the U.S.health care system,including lower insurance reimbursement rates,have resulted in

(Multiple Choice)

4.9/5 (40)

When production reflects consumer preferences,________ occurs.

(Multiple Choice)

4.9/5 (27)

Scarcity is a problem that will eventually disappear as technology advances.

(True/False)

4.9/5 (44)

Which of the following is an example of an efficiency-equity trade-off faced by economic agents?

(Multiple Choice)

4.9/5 (38)

Economists assume that rational people do all of the following except

(Multiple Choice)

4.7/5 (47)

In the market for factors of production,firms earn income by selling goods and services to households.

(True/False)

4.8/5 (33)

"An increase in the price of gasoline will increase the demand for hybrid vehicles." This statement is an example of a positive economic statement.

(True/False)

5.0/5 (32)

Optimal decisions are made at the point where marginal cost equals zero.

(True/False)

4.9/5 (37)

In economics,the accumulated skills and training that workers have is known as

(Multiple Choice)

4.8/5 (50)

"The distribution of income should be left to the market" is an example of a positive economic statement.

(True/False)

4.8/5 (38)

Who receives the most of what is produced in a market economy?

(Multiple Choice)

4.9/5 (29)

Which of the following is not an example of an economic trade-off that a firm has to make?

(Multiple Choice)

4.8/5 (36)

All of the following contributed to the downfall of the Soviet Union in 1991 except

(Multiple Choice)

4.8/5 (35)

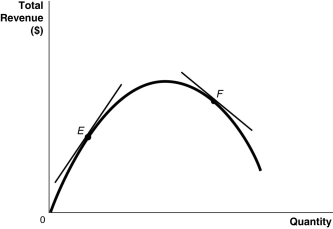

Figure 1-4  -Refer to Figure 1-4.Which of the following statements is false?

-Refer to Figure 1-4.Which of the following statements is false?

(Multiple Choice)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)