Exam 1: Economics: Foundations and Models

Exam 1: Economics: Foundations and Models142 Questions

Exam 2: Trade-Offs, comparative Advantage, and the Market System152 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply149 Questions

Exam 4: Economic Efficiency, government Price Setting, and Taxes137 Questions

Exam 5: Externalities, environmental Policy, and Public Goods139 Questions

Exam 6: Elasticity: The Responsiveness of Demand and Supply149 Questions

Exam 7: The Economics of Health Care117 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance140 Questions

Exam 9: Comparative Advantage and the Gains From International Trade124 Questions

Exam 10: Consumer Choice and Behavioral Economics154 Questions

Exam 11: Technology, production, and Costs174 Questions

Exam 12: Firms in Perfectly Competitive Markets153 Questions

Exam 13: Monopolistic Competition: The Competitive Model in a More Realistic Setting137 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets129 Questions

Exam 15: Monopoly and Antitrust Policy148 Questions

Exam 16: Pricing Strategy134 Questions

Exam 17: The Markets for Labor and Other Factors of Production149 Questions

Exam 18: Public Choice, taxes, and the Distribution of Income134 Questions

Exam 19: GDP: Measuring Total Production and Income135 Questions

Exam 20: Unemployment and Inflation148 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles130 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies134 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run157 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis145 Questions

Exam 25: Money, banks, and the Federal Reserve System144 Questions

Exam 26: Monetary Policy145 Questions

Exam 27: Fiscal Policy155 Questions

Exam 28: Inflation, unemployment, and Federal Reserve Policy135 Questions

Exam 29: Macroeconomics in an Open Economy145 Questions

Exam 30: The International Financial System139 Questions

Select questions type

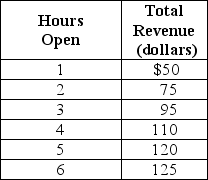

Table 1-1

Lydia runs a small nail salon in the town of New Hope. She is debating whether she should extend her hours of operation. Lydia figures that her sales revenue will depend on the number of hours the nail salon is open as shown in the table above. She would have to hire a worker for those hours at a wage rate of $10 per hour.

-Refer to Table 1-1.What is Lydia's marginal benefit if she decides to stay open for two hours instead of one hour?

Lydia runs a small nail salon in the town of New Hope. She is debating whether she should extend her hours of operation. Lydia figures that her sales revenue will depend on the number of hours the nail salon is open as shown in the table above. She would have to hire a worker for those hours at a wage rate of $10 per hour.

-Refer to Table 1-1.What is Lydia's marginal benefit if she decides to stay open for two hours instead of one hour?

(Multiple Choice)

4.8/5  (41)

(41)

If it costs Sinclair $300 to produce 3 suede jackets and $420 to produce 4 suede jackets,then the difference of $120 is the marginal cost of producing the 4th suede jacket.

(True/False)

4.7/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)