Exam 5: Consolidated Financial Statementsintra-Entity Asset Transactions

Exam 1: The Equity Method of Accounting for Investments119 Questions

Exam 2: Consolidation of Financial Information118 Questions

Exam 3: Consolidationssubsequent to the Date of Acquisition122 Questions

Exam 4: Consolidated Financial Statements and Outside Ownership115 Questions

Exam 5: Consolidated Financial Statementsintra-Entity Asset Transactions127 Questions

Exam 6: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues115 Questions

Exam 7: Foreign Currency Transactions and Hedging Foreign Exchange Risk93 Questions

Exam 8: Translation of Foreign Currency Financial Statements97 Questions

Exam 9: Partnerships: Formation and Operation88 Questions

Exam 10: Partnerships: Termination and Liquidation69 Questions

Exam 11: Accounting for State and Local Governments Part 178 Questions

Exam 12: Accounting for State and Local Governments Part 251 Questions

Select questions type

Which of the following statements is true concerning an intra-entity transfer of a depreciable asset?

(Multiple Choice)

4.7/5  (25)

(25)

Virginia Corp. owned all of the voting common stock of Stateside Co. Both companies use the perpetual inventory method, and Virginia decided to use the partial equity method to account for this investment. During 2010, Virginia made cash sales of $400,000 to Stateside. The gross profit rate was 30% of the selling price. By the end of 2010, Stateside had sold 75% of the goods to outside parties for $420,000 cash.

Prepare the consolidation entries that should be made at the end of 2010.

(Essay)

4.8/5 (38)

Stark Company, a 90% owned subsidiary of Parker, Inc., sold land to Parker on May 1, 2010, for $80,000. The land originally cost Stark $85,000. Stark reported net income of $200,000, $180,000, and $220,000 for 2010, 2011, and 2012, respectively. Parker sold the land purchased from Stark in 2010 for $92,000 in 2012.

Compute the gain or loss relating to the land that will be reported in consolidated net income for 2012.

(Multiple Choice)

4.9/5 (37)

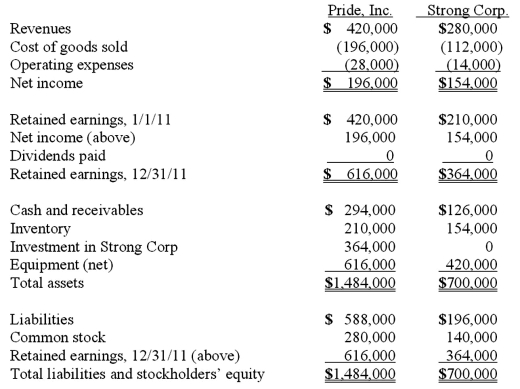

On January 1, 2011, Pride, Inc. acquired 80% of the outstanding voting common stock of Strong Corp. for $364,000. There is no active market for Strong's stock. Of this payment, $28,000 was allocated to equipment (with a five-year life) that had been undervalued on Strong's books by $35,000. Any remaining excess was attributable to goodwill which has not been impaired.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the consolidated total of non-controlling interest appearing in the balance sheet?

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the consolidated total of non-controlling interest appearing in the balance sheet?

(Multiple Choice)

4.9/5 (33)

Throughout 2011, Cleveland Co. sold inventory to Leeward Co., its subsidiary. From a consolidated point of view, when will the gain on this transfer be earned?

(Essay)

4.7/5 (44)

Clemente Co. owned all of the voting common stock of Snider Co. On January 2, 2010, Clemente sold equipment to Snider for $125,000. The equipment had cost Clemente $140,000. At the time of the sale, the balance in accumulated depreciation was $40,000. The equipment had a remaining useful life of five years and a $0 salvage value. Straight-line depreciation is used by both Clemente and Snider.

At what amount should the equipment (net of depreciation) be included in the consolidated balance sheet dated December 31, 2010?

(Multiple Choice)

4.7/5 (38)

During 2011, Edwards Co. sold inventory to its parent company, Forsyth Corp. Forsyth still owned the entire inventory purchased at the end of 2011. Why must the gross profit on the sale be deferred when consolidated financial statements are prepared at the end of 2011?

(Essay)

4.9/5 (34)

On January 1, 2010, Smeder Company, an 80% owned subsidiary of Collins, Inc., transferred equipment with a 10-year life (six of which remain with no salvage value) to Collins in exchange for $84,000 cash. At the date of transfer, Smeder's records carried the equipment at a cost of $120,000 less accumulated depreciation of $48,000. Straight-line depreciation is used. Smeder reported net income of $28,000 and $32,000 for 2010 and 2011, respectively. All net income effects of the intra-entity transfer are attributed to the seller for consolidation purposes.

Compute Collins' share of Smeder's net income for 2011.

(Multiple Choice)

4.9/5 (40)

Wilson owned equipment with an estimated life of 10 years when it was acquired for an original cost of $80,000. The equipment had a book value of $50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends:

Compute the gain on transfer of equipment reported by Wilson for 2010.

(Multiple Choice)

4.7/5 (41)

Wilson owned equipment with an estimated life of 10 years when it was acquired for an original cost of $80,000. The equipment had a book value of $50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends:

Compute the amortization of gain through a depreciation adjustment for 2012 for consolidation purposes.

(Multiple Choice)

4.9/5 (38)

During 2010, Von Co. sold inventory to its wholly-owned subsidiary, Lord Co. The inventory cost $30,000 and was sold to Lord for $44,000. From the perspective of the combination, when is the $14,000 gain realized?

(Multiple Choice)

4.8/5 (32)

Stark Company, a 90% owned subsidiary of Parker, Inc., sold land to Parker on May 1, 2010, for $80,000. The land originally cost Stark $85,000. Stark reported net income of $200,000, $180,000, and $220,000 for 2010, 2011, and 2012, respectively. Parker sold the land purchased from Stark in 2010 for $92,000 in 2012.

Compute the gain or loss on the intra-entity sale of land.

(Multiple Choice)

5.0/5 (40)

What is the purpose of the adjustments to depreciation expense within the consolidation process when there has been an intra-entity transfer of a depreciable asset?

(Essay)

4.7/5 (34)

Pot Co. holds 90% of the common stock of Skillet Co. During 2011, Pot reported sales of $1,120,000 and cost of goods sold of $840,000. For this same period, Skillet had sales of $420,000 and cost of goods sold of $252,000.

Included in the amounts for Skillet's sales were Skillet's sales of merchandise to Pot for $140,000. There were no sales from Pot to Skillet. Intra-entity sales had the same markup as sales to outsiders. Pot still had 40% of the intra-entity sales as inventory at the end of 2011. What are consolidated sales and cost of goods sold for 2011?

(Multiple Choice)

4.9/5 (43)

Strickland Company sells inventory to its parent, Carter Company, at a profit during 2010. One-third of the inventory is sold by Carter in 2010.

In the consolidation worksheet for 2010, which of the following choices would be a debit entry to eliminate the intra-entity transfer of inventory?

(Multiple Choice)

4.8/5 (32)

Stark Company, a 90% owned subsidiary of Parker, Inc., sold land to Parker on May 1, 2010, for $80,000. The land originally cost Stark $85,000. Stark reported net income of $200,000, $180,000, and $220,000 for 2010, 2011, and 2012, respectively. Parker sold the land purchased from Stark in 2010 for $92,000 in 2012.

Compute income from Stark reported on Parker's books for 2012.

(Multiple Choice)

4.7/5 (29)

Tara Company owns 80 percent of the common stock of Stodd Inc. In the current year, Tara reports sales of $5,000,000 and cost of goods sold of $3,500,000. For the same period, Stodd has sales of $500,000 and cost of goods sold of $400,000. During the year, Stodd sold merchandise to Tara for $40,000 at a price based on the normal markup. At the end of the year, Tara still possesses 20 percent of this inventory. Prepare the consolidation entry to defer the unrealized gain.

(Essay)

4.9/5 (41)

Stiller Company, an 80% owned subsidiary of Leo Company, purchased land from Leo on March 1, 2010, for $75,000. The land originally cost Leo $60,000. Stiller reported net income of $125,000 and $140,000 for 2010 and 2011, respectively. Leo uses the equity method to account for its investment.

Compute income from Stiller on Leo's books for 2011.

(Multiple Choice)

4.9/5 (30)

Several years ago Polar Inc. acquired an 80% interest in Icecap Co. The book values of Icecap's asset and liability accounts at that time were considered to be equal to their fair values. Polar's acquisition value corresponded to the underlying book value of Icecap so that no allocations or goodwill resulted from the transaction.

The following selected account balances were from the individual financial records of these two companies as of December 31, 2011:

Polar sold a building to Icecap on January 1, 2010 for $112,000, although the book value of this asset was only $70,000 on that date. The building had a five-year remaining useful life and was to be depreciated using the straight-line method with no salvage value.

Required:

For the consolidated financial statements for 2011, determine the balances that would appear for the following accounts: (1) Buildings (net), (2) Operating expenses, and (3) Non-controlling Interest in Subsidiary's Net Income.

(Essay)

4.7/5 (35)

Edgar Co. acquired 60% of Stendall Co. on January 1, 2011. During 2011, Edgar made several sales of inventory to Stendall. The cost and selling price of the goods were $140,000 and $200,000, respectively. Stendall still owned one-fourth of the goods at the end of 2011. Consolidated cost of goods sold for 2011 was $2,140,000 because of a consolidating adjustment for intra-entity sales less the entire profit remaining in Stendall's ending inventory.

How would consolidated cost of goods sold have differed if the inventory transfers had been for the same amount and cost, but from Stendall to Edgar?

(Multiple Choice)

4.8/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)