Exam 25: Consolidation: Intragroup Transactions

Exam 1: The Conceptual Framework of the Iasb30 Questions

Exam 2: Shareholders Equity: Share Capital and Reserves28 Questions

Exam 3: Fair Value Measurement30 Questions

Exam 4: Revenue30 Questions

Exam 5: Provisions, Contingent Liabilities and Contingent Assets30 Questions

Exam 6: Income Taxes28 Questions

Exam 7: Financial Instruments30 Questions

Exam 8: Share-Based Payments28 Questions

Exam 9: Inventories29 Questions

Exam 10: Employee Benefits29 Questions

Exam 11: Property, Plant and Equipment28 Questions

Exam 12: Leases27 Questions

Exam 13: Intangible Assets28 Questions

Exam 14: Business Combinations30 Questions

Exam 15: Impairment of Assets28 Questions

Exam 16: Accounting for Mineral Resources26 Questions

Exam 17: Agriculture26 Questions

Exam 18: Financial Statement Presentation29 Questions

Exam 19: Statement of Cash Flows28 Questions

Exam 20: Earnings Per Share20 Questions

Exam 21: Operating Segments30 Questions

Exam 22: Operating Segments29 Questions

Exam 23: Consolidation: Controlled Entities29 Questions

Exam 24: Consolidation: Wholly Owned Subsidiaries26 Questions

Exam 25: Consolidation: Intragroup Transactions27 Questions

Exam 26: Consolidation: Non-Controlling Interest25 Questions

Exam 27: Consolidation: Other Issues29 Questions

Exam 28: Translation of the Financial Statements of Foreign Entities28 Questions

Exam 29: Associates and Joint Ventures26 Questions

Exam 30: Joint Arrangements26 Questions

Select questions type

A consolidation adjustment entry made to eliminate the intragroup sales of inventory at a profit would take the following form:

(Multiple Choice)

4.8/5  (50)

(50)

Angelo Limited sold inventory to its parent entity at a profit of $4 000. The inventory cost Angelo Limited $16 000. At the end of the reporting period the parent had sold 50% of the inventory to an external party. The consolidation adjustment entry (excluding tax effects) will eliminate unrealised profit amounting to:

(Multiple Choice)

4.9/5 (40)

A subsidiary sold inventory to a parent entity for $10 000. The inventory originally cost the subsidiary $6000. At the end of the reporting period the parent had sold 50% of the inventory to an external party. The company tax rate is 30%. The deferred tax item that is recognised on consolidation is:

(Multiple Choice)

4.8/5 (29)

Equipment costing $10 000 was sold by one entity within a group to another for $4000. Accumulated depreciation at date of sale was $3000. The consolidation entry will contain the following adjustment to the amount of the Equipment:

(Multiple Choice)

4.9/5 (34)

IFRS 10 Consolidated Financial Statements, requires that intragroup transactions be:

(Multiple Choice)

4.8/5 (42)

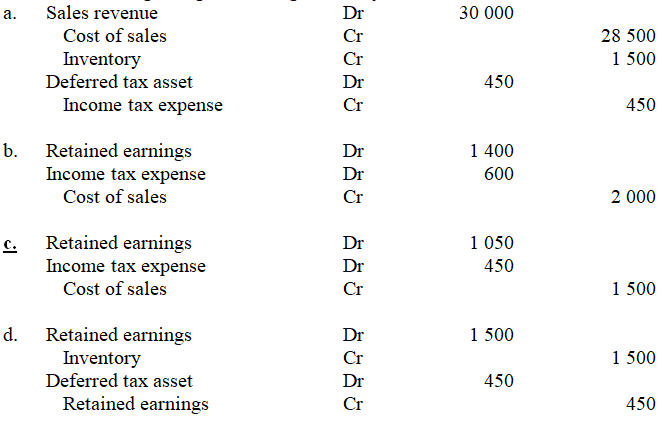

During the year ended 30 June 20X7 a subsidiary entity sold inventory to a parent entity for $30 000. The inventory had previously cost the subsidiary entity $24 000. By 30 June 20X7 the parent entity had sold 75% of the inventory to a party outside the group. The company tax rate is 30%. The adjustment entry in the consolidation worksheet at 30 June 20X8 is:

(Essay)

4.7/5 (34)

During the year ended 30 June 20X7, a parent entity rents a warehouse from a subsidiary entity for $100 000. The company tax rate is 30%. The consolidation adjustment entry needed at reporting date is:

(Multiple Choice)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)