Exam 8: Multinational Accounting: Foreign Currency Transactions and Financial Instruments

Exam 1: Intercorporate Acquisitions and Investments in Other Entities47 Questions

Exam 2: Reporting Intercorporate Investments and Consolidation of Wholly Owned Subsidiaries With No Differential39 Questions

Exam 3: The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries With No Differential39 Questions

Exam 4: Consolidation of Wholly Owned Subsidiaries Acquired at More Than Book Value47 Questions

Exam 5: Consolidation of Less-Than-Wholly-Owned Subsidiaries Acquired at More Than Book Value41 Questions

Exam 6: Intercompany Inventory Transactions51 Questions

Exam 7: Intercompany Transfers of Services and Noncurrent Assets46 Questions

Exam 8: Multinational Accounting: Foreign Currency Transactions and Financial Instruments56 Questions

Exam 9: Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements60 Questions

Exam 10: Partnerships: Formation, Operation, and Changes in Membership56 Questions

Exam 11: Partnerships: Liquidation49 Questions

Exam 12: Governmental Entities: Introduction and General Fund Accounting69 Questions

Exam 13: Governmental Entities: Special Funds and Government-Wide Financial Statements68 Questions

Select questions type

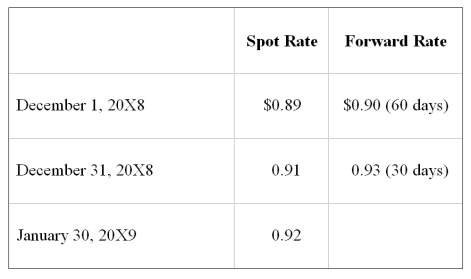

Taste Bits Inc. purchased chocolates from Switzerland for 200,000 Swiss francs (SFr) on December 1, 20X8. Payment is due on January 30, 20X9. On December 1, 20X8, the company also entered into a 60-day forward contract to purchase 100,000 Swiss francs. The forward contract is not designated as a hedge. The rates were as follows:  -Based on the preceding information, the entries on December 31, 20X8, include a:

-Based on the preceding information, the entries on December 31, 20X8, include a:

(Multiple Choice)

4.8/5  (44)

(44)

Taste Bits Inc. purchased chocolates from Switzerland for 200,000 Swiss francs (SFr) on December 1, 20X8. Payment is due on January 30, 20X9. On December 1, 20X8, the company also entered into a 60-day forward contract to purchase 100,000 Swiss francs. The forward contract is not designated as a hedge. The rates were as follows:

-Based on the preceding information, the entries on January 30, 20X9, include a:

(Multiple Choice)

4.8/5 (43)

If 1 British pound can be exchanged for 180 cents of U.S. currency, what fraction should be used to compute the indirect quotation of the exchange rate expressed in British pounds?

(Multiple Choice)

4.9/5 (46)

Taste Bits Inc. purchased chocolates from Switzerland for 200,000 Swiss francs (SFr) on December 1, 20X8. Payment is due on January 30, 20X9. On December 1, 20X8, the company also entered into a 60-day forward contract to purchase 100,000 Swiss francs. The forward contract is not designated as a hedge. The rates were as follows:

-Based on the preceding information, the entries on January 30, 20X9, include a:

(Multiple Choice)

4.8/5 (37)

Suppose the direct foreign exchange rates in U.S. dollars are:

1 Singapore dollar = $.7025

1 Cyprus pound = $2.5132

-Based on the information given above, how many Singapore dollars are required to purchase goods costing 10,000 U.S. dollars?

(Multiple Choice)

4.8/5 (34)

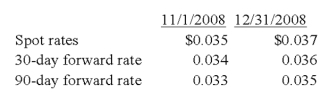

Levin Company entered into a forward contract to speculate in the foreign currency. It sold 100,000 foreign currency units under a contract dated November 1, 20X8, for delivery on January 31, 20X9:  In its income statement for the year ended December 31, 20X8, what amount of loss should Levin report from this forward contract?

In its income statement for the year ended December 31, 20X8, what amount of loss should Levin report from this forward contract?

(Multiple Choice)

4.8/5 (37)

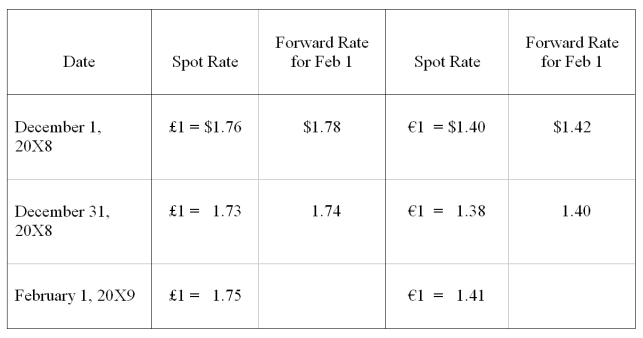

On December 1, 20X8, Hedge Company entered into a 60-day speculative forward contract to sell 200,000 British pounds ( ) at a forward rate of 1 = $1.78. On the same day it purchased a 60-day speculative forward contract to buy 100,000 euros (€) at a forward rate of €1 = $1.42.

The rates are as follows:  Hedge had no other speculation transactions in 20X8 and 20X9. Ignore taxes.

-Based on the preceding information, what is the overall effect of speculation on 20X8 net income?

Hedge had no other speculation transactions in 20X8 and 20X9. Ignore taxes.

-Based on the preceding information, what is the overall effect of speculation on 20X8 net income?

(Multiple Choice)

5.0/5 (34)

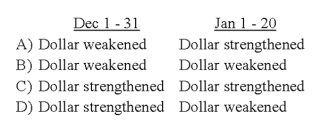

Heavy Company sold metal scrap to a Brazilian company for 200,000 Brazilian reals on December 1, 20X8, with payment due on January 20, 20X9. The exchange rates were:  -Based on the preceding information, which of the following is true of dollar's movement vis-à-vis Brazilian real during the period?

-Based on the preceding information, which of the following is true of dollar's movement vis-à-vis Brazilian real during the period?

(Multiple Choice)

4.9/5 (35)

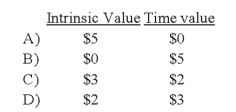

The fair market value of a near-month call option with a strike price of $45 is $5, when the stock is trading at $48.

-Based on the preceding information, which of the following is true of the intrinsic and time values associated with this option.

(Multiple Choice)

4.9/5 (35)

The fair market value of a near-month call option with a strike price of $45 is $5, when the stock is trading at $48.

-Based on the preceding information, the call option:

(Multiple Choice)

4.8/5 (46)

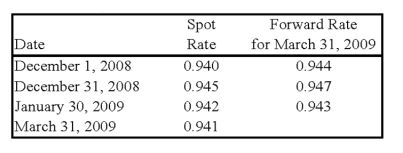

On December 1, 2008, Denizen Corporation entered into a 120-day forward contract to purchase 200,000 Canadian dollars (C$). Denizen's fiscal year ends on December 31. The forward contract was to hedge an anticipated purchase of electronic goods on January 30, 2009. The purchase took place on January 30, with payment due on March 31, 2009. The derivative is designated as a cash flow hedge. The company uses the forward exchange rate to measure hedge effectiveness. The direct exchange rates follow:  Required:

Prepare all journal entries for Denizen Corporation.

Required:

Prepare all journal entries for Denizen Corporation.

(Essay)

4.7/5 (36)

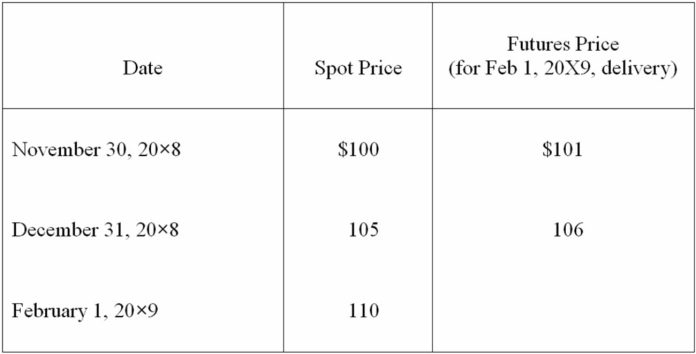

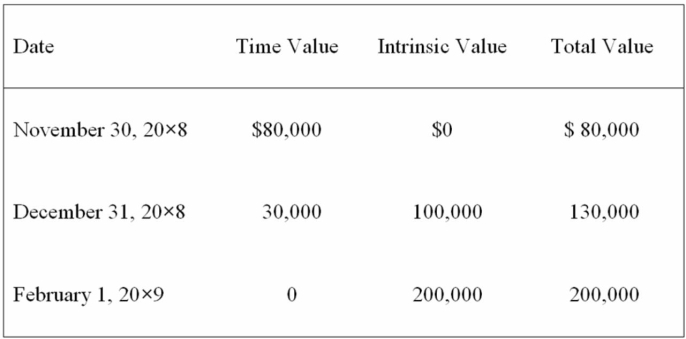

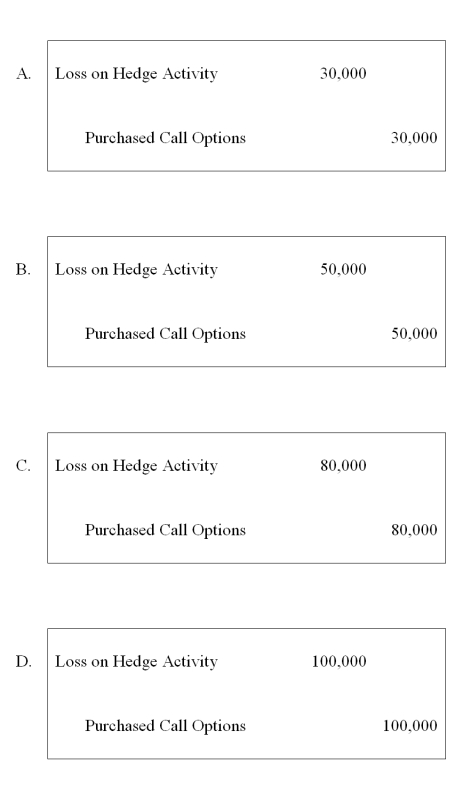

Spiralling crude oil prices prompted AMAR Company to purchase call options on oil as a price-risk-hedging device to hedge the expected increase in prices on an anticipated purchase of oil. On November 30, 20X8, AMAR purchases call options for 20,000 barrels of oil at $100 per barrel at a premium of $4 per barrel, with a February 1, 20X9, call date. The following is the pricing information for the term of the call:  The information for the change in the fair value of the options follows:

The information for the change in the fair value of the options follows:  On February 1, 20X9, AMAR sells the options at their value on that date and acquires 20,000 barrels of oil at the spot price. On April 1, 20X9, AMAR sells the oil for $112 per barrel.

-Based on the preceding information, which of the following adjusting entries would be required on December 31, 20X8?

On February 1, 20X9, AMAR sells the options at their value on that date and acquires 20,000 barrels of oil at the spot price. On April 1, 20X9, AMAR sells the oil for $112 per barrel.

-Based on the preceding information, which of the following adjusting entries would be required on December 31, 20X8?

(Multiple Choice)

4.8/5 (28)

Spiralling crude oil prices prompted AMAR Company to purchase call options on oil as a price-risk-hedging device to hedge the expected increase in prices on an anticipated purchase of oil. On November 30, 20X8, AMAR purchases call options for 20,000 barrels of oil at $100 per barrel at a premium of $4 per barrel, with a February 1, 20X9, call date. The following is the pricing information for the term of the call: The information for the change in the fair value of the options follows: On February 1, 20X9, AMAR sells the options at their value on that date and acquires 20,000 barrels of oil at the spot price. On April 1, 20X9, AMAR sells the oil for $112 per barrel.

-Based on the preceding information, the entries made on April 1, 20X9 will include:

(Multiple Choice)

5.0/5 (37)

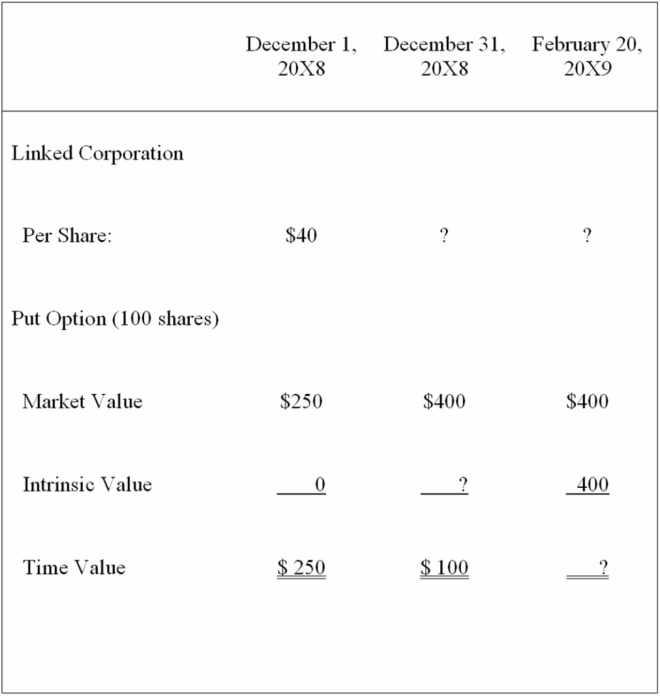

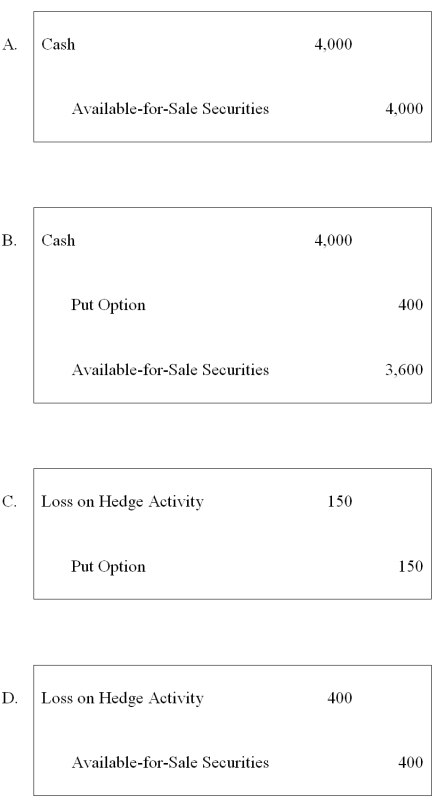

On December 1, 20X8, Winston Corporation acquired 100 shares of Linked Corporation at a cost of $40 per share. Winston classifies them as available-for-sale securities. On this same date, it decides to hedge against a possible decline in the value of the securities by purchasing, at a cost of $250, an at-the-money put option to sell the 100 shares at $40 per share. The option expires on February 20, 20X9. Selected information concerning the fair values of the investment and the options follow:  Assume that Winston exercises the put option and sells Linked shares on February 20, 20X9.

-Based on the preceding information, which of the following journal entries will be made on February 20, 20X9?

Assume that Winston exercises the put option and sells Linked shares on February 20, 20X9.

-Based on the preceding information, which of the following journal entries will be made on February 20, 20X9?

(Multiple Choice)

4.9/5 (38)

On December 1, 20X8, Hedge Company entered into a 60-day speculative forward contract to sell 200,000 British pounds ( ) at a forward rate of 1 = $1.78. On the same day it purchased a 60-day speculative forward contract to buy 100,000 euros (€) at a forward rate of €1 = $1.42.

The rates are as follows: Hedge had no other speculation transactions in 20X8 and 20X9. Ignore taxes.

-Based on the preceding information, what is the effect of the euro speculative contract on 20X9 net income?

(Multiple Choice)

4.9/5 (35)

On December 1, 20X8, Winston Corporation acquired 100 shares of Linked Corporation at a cost of $40 per share. Winston classifies them as available-for-sale securities. On this same date, it decides to hedge against a possible decline in the value of the securities by purchasing, at a cost of $250, an at-the-money put option to sell the 100 shares at $40 per share. The option expires on February 20, 20X9. Selected information concerning the fair values of the investment and the options follow: Assume that Winston exercises the put option and sells Linked shares on February 20, 20X9.

-Based on the preceding information, what is the market price of Linked Corporation stock on February 20, 20X9?

(Multiple Choice)

4.9/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)