Exam 7: Perfect Competition

If the long-run market supply curve in a perfectly competitive industry is upward sloping, then the industry:

B

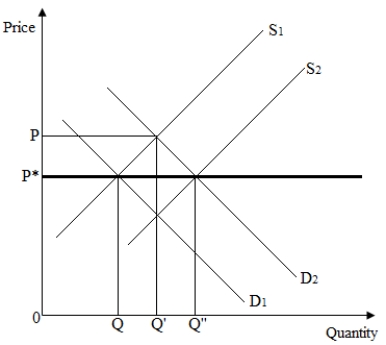

Derive the long-run supply curve of a perfectly competitive constant-cost industry. Use graphical analysis.

The initial point of equilibrium occurs where demand curve D1 intersects short-run supply curve S1, resulting in price P* and quantity Q.

When the demand curve shift outwards, the new equilibrium price in the short run will be higher than the initial equilibrium price (P > P*), output increases to Q', and firms will make positive economic profits. In a competitive market with free entry, new firms will enter the market. Since it is a constant cost industry, entry of new firms does not bid up input prices. Therefore, as new firms enter, the market supply curve shifts outward (to S2), industry output increases to Q", and price returns to its original level. (Joining the two equilibrium points generates the horizontal line at P*.) Therefore, for an industry with constant costs, the long-run supply curve is horizontal.

When the demand curve shift outwards, the new equilibrium price in the short run will be higher than the initial equilibrium price (P > P*), output increases to Q', and firms will make positive economic profits. In a competitive market with free entry, new firms will enter the market. Since it is a constant cost industry, entry of new firms does not bid up input prices. Therefore, as new firms enter, the market supply curve shifts outward (to S2), industry output increases to Q", and price returns to its original level. (Joining the two equilibrium points generates the horizontal line at P*.) Therefore, for an industry with constant costs, the long-run supply curve is horizontal.

Everything else remaining unchanged, an increase in demand will lead to:

C

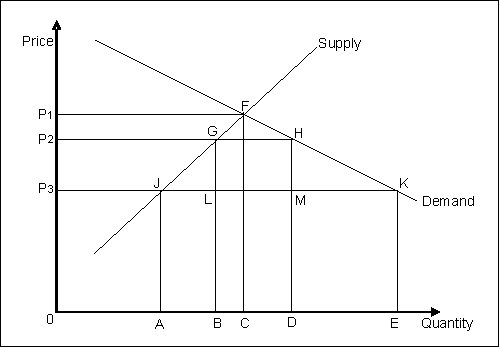

The following figure shows the domestic demand and supply curves for a good. With free trade, the price of the good in the domestic market is P3. The government introduces a 5% tariff in the market which raises the domestic price to P2.

Figure 7-1

-Refer to Figure 7-1. With the imposition of the tariff, the deadweight loss in the market is equal to:

-Refer to Figure 7-1. With the imposition of the tariff, the deadweight loss in the market is equal to:

How can supply and demand analysis be used to measure consumer surplus? How does consumer surplus change if the market price falls?

Derive the short-run supply curve of a firm under perfect competition.

A firm has the following cost function: C = 30 - 14Q + Q2. Derive the firm's supply curve from the total cost function.

Alex is the manager of a division of a paper firm that produces copier paper and sells it on the wholesale market. His firm's output represents about 1.5% of total copier paper sales. The wholesale price of copier paper is $3.95 per standard package. The firm's engineers report that, at projected volumes, labor costs are $1.00 per package, material costs are $2.00 per package, and other average fixed costs are about $.75 per package. What price should the firm charge for its copier paper?

The following figure shows the domestic demand and supply curves for a good. With free trade, the price of the good in the domestic market is P3. The government introduces a 5% tariff in the market which raises the domestic price to P2.

Figure 7-1

-Refer to Figure 7-1. If the government substitutes the tariff for a quota that raises the price in the domestic price to P2, the deadweight loss in the market would be equal to:

Demand for a good is given by: QD = 100 - P and supply by QS = .5P - 20, where P is the market price of the good. In equilibrium, price and output under perfect competition will be:

In order to maximize profits, a perfectly competitive firm will continue producing until:

With free trade, the market for a particular good or service is in equilibrium when:

The following figure shows the domestic demand and supply curves for a good. With free trade, the price of the good in the domestic market is P3. The government introduces a 5% tariff in the market which raises the domestic price to P2.

Figure 7-1

-Refer to Figure 7-1. When trade is not restricted, the level of imports to the domestic market is _____.

Discuss why many agricultural industries in the United States are primary examples of perfectly competitive markets.

Suppose a severe freeze damages the Florida orange crop. Everything else remaining unchanged, which of the following is most likely to be true?

The height of an individual demand curve at each level of output shows:

Explain why perfectly competitive firms cannot earn positive economic profits in the long run.

The marginal cost of a firm under perfect competition is given by the equation MC = 2QF − 20. The market price is $50 per unit. Determine the firm's profit-maximizing level of output. Write down the equation for the firm's supply curve.

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)