Exam 33: Aggregate Demand and Aggregate Supply

Exam 1: What Is Economics59 Questions

Exam 2: Thinking Like an Economist54 Questions

Exam 3: The Market Forces of Supply and Demand56 Questions

Exam 4: Elasticity and Its Applications58 Questions

Exam 5: Background to Demand: Consumer Choices61 Questions

Exam 6: Background to Supply: Firms in Competitive Markets54 Questions

Exam 7: Consumers, Producers and the Efficiency of Markets56 Questions

Exam 8: Supply, Demand and Government Policies51 Questions

Exam 9: The Tax System48 Questions

Exam 10: Public Goods, Common Resources and Merit Goods58 Questions

Exam 11: Market Failure and Externalities61 Questions

Exam 12: Information and Behavioural Economics60 Questions

Exam 13: Firms Production Decisions47 Questions

Exam 14: Market Structures I: Monopoly57 Questions

Exam 15: Market Structures Ii: Monopolistic Competition59 Questions

Exam 16: Market Structures Iii: Oligopoly55 Questions

Exam 17: The Economics of Factor Markets60 Questions

Exam 18: Income Inequality and Poverty60 Questions

Exam 19: Interdependence and the Gains From Trade56 Questions

Exam 20: Measuring a Nations Well-Being60 Questions

Exam 21: Measuring the Cost of Living59 Questions

Exam 22: Production and Growth60 Questions

Exam 23: Unemployment60 Questions

Exam 24: Saving, Investment and the Financial System60 Questions

Exam 25: The Basic Tools of Finance57 Questions

Exam 26: Issues in Financial Markets59 Questions

Exam 27: The Monetary System60 Questions

Exam 28: Money Growth and Inflation59 Questions

Exam 29: Open-Economy Macroeconomics: Basic Concepts60 Questions

Exam 30: A Macroeconomic Theory of the Open Economy61 Questions

Exam 31: Business Cycles55 Questions

Exam 32: Keynesian Economics and the Is-Lm Analysis60 Questions

Exam 33: Aggregate Demand and Aggregate Supply60 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand41 Questions

Exam 35: The Short-Run Trade-Off Between Inflation and Unemployment52 Questions

Exam 36: Supply-Side Policies57 Questions

Exam 37: Common Currency Areas and European Monetary Union55 Questions

Exam 38: The Financial Crisis and Sovereign Debt60 Questions

Select questions type

Economists refer to fluctuations in output as the "business cycle" because movements in output are regular and predictable.

Free

(True/False)

4.8/5  (38)

(38)

Correct Answer: Verified

Verified

False

To say that nominal prices are sticky means

Free

(Multiple Choice)

4.8/5 (28)

Correct Answer:Verified

D

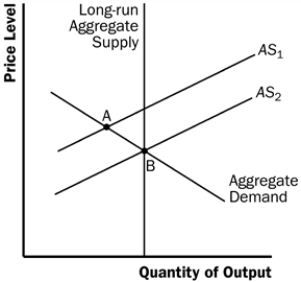

Suppose an economy is in recession. If the government does nothing, what ensures that the economy still eventually gets back to the natural rate of output? Create a chart to depict an economy in recession.

Free

(Essay)

4.8/5 (29)

Correct Answer:Verified

The graph below depicts an economy in a recession. The short-run aggregate supply curve is AS1 and the economy is in equilibrium at point A, which is to the left of the long-run aggregate supply curve. If policymakers take no action, the economy will return to the long-run aggregate supply curve over time since the actual price level will be below the price level that people expected. Individuals will eventually correct their expectations about the price level. As they do so, prices and wages will adjust accordingly, shifting the aggregate supply curve to the right to AS2. The economy's new equilibrium is at point B. The rightward shift in aggregate supply eventually causes output to rise back to the natural rate.

According to the interest rate effect, aggregate demand slopes downward (negatively) because lower prices

(Multiple Choice)

4.7/5 (37)

An increase in price expectations shifts the long-run aggregate supply curve to the left.

(True/False)

4.9/5 (41)

One reason that the aggregate demand slopes downward is the wealth effect: a decrease in the price level increases the value of money holdings and consumer spending rises.

(True/False)

4.8/5 (37)

Make a list of things that would shift the long-run aggregate supply curve to the right.

(Essay)

4.9/5 (30)

Suppose the economy is initially in long-run equilibrium. Then suppose there is a drought that destroys much of the wheat crop. If policymakers allow the economy to adjust to long-run equilibrium on its own, according to the model of aggregate demand and aggregate supply, what happens to prices and output in the long run?

(Multiple Choice)

4.7/5 (34)

Policy makers are said to "accommodate" an adverse supply shock if they

(Multiple Choice)

4.9/5 (26)

Explain how an increase in the price level changes interest rates. How does this change in interest rates lead to changes in investment and net exports?

(Essay)

4.8/5 (36)

The wealth effect, interest rate effect, and foreign trade effect all explain why the

(Multiple Choice)

4.8/5 (39)

Which of the following would not cause a shift in the long-run aggregate supply curve? An increase in:

(Multiple Choice)

4.8/5 (30)

The long-run effect of an increase in government spending that shifts the economy's aggregate demand curve to the right is to raise

(Multiple Choice)

4.9/5 (37)

According to classical macroeconomic theory, changes in the money supply affect

(Multiple Choice)

4.8/5 (32)

Which of the following events shifts the short-run aggregate supply curve to the right?

(Multiple Choice)

4.9/5 (32)

Which of the following is not a determinant of long-run aggregate supply?

(Multiple Choice)

4.8/5 (35)

Suppose the economy is initially in long-run equilibrium. Then suppose there is an increase in military spending due to rising international tensions. According to the model of aggregate demand and aggregate supply, what happens to prices and output in the long run?

(Multiple Choice)

4.9/5 (38)

Most economists believe that classical macroeconomic theory is a good description of the economy

(Multiple Choice)

4.9/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)