Exam 7: Consumers, Producers and the Efficiency of Markets

Exam 1: What Is Economics59 Questions

Exam 2: Thinking Like an Economist54 Questions

Exam 3: The Market Forces of Supply and Demand56 Questions

Exam 4: Elasticity and Its Applications58 Questions

Exam 5: Background to Demand: Consumer Choices61 Questions

Exam 6: Background to Supply: Firms in Competitive Markets54 Questions

Exam 7: Consumers, Producers and the Efficiency of Markets56 Questions

Exam 8: Supply, Demand and Government Policies51 Questions

Exam 9: The Tax System48 Questions

Exam 10: Public Goods, Common Resources and Merit Goods58 Questions

Exam 11: Market Failure and Externalities61 Questions

Exam 12: Information and Behavioural Economics60 Questions

Exam 13: Firms Production Decisions47 Questions

Exam 14: Market Structures I: Monopoly57 Questions

Exam 15: Market Structures Ii: Monopolistic Competition59 Questions

Exam 16: Market Structures Iii: Oligopoly55 Questions

Exam 17: The Economics of Factor Markets60 Questions

Exam 18: Income Inequality and Poverty60 Questions

Exam 19: Interdependence and the Gains From Trade56 Questions

Exam 20: Measuring a Nations Well-Being60 Questions

Exam 21: Measuring the Cost of Living59 Questions

Exam 22: Production and Growth60 Questions

Exam 23: Unemployment60 Questions

Exam 24: Saving, Investment and the Financial System60 Questions

Exam 25: The Basic Tools of Finance57 Questions

Exam 26: Issues in Financial Markets59 Questions

Exam 27: The Monetary System60 Questions

Exam 28: Money Growth and Inflation59 Questions

Exam 29: Open-Economy Macroeconomics: Basic Concepts60 Questions

Exam 30: A Macroeconomic Theory of the Open Economy61 Questions

Exam 31: Business Cycles55 Questions

Exam 32: Keynesian Economics and the Is-Lm Analysis60 Questions

Exam 33: Aggregate Demand and Aggregate Supply60 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand41 Questions

Exam 35: The Short-Run Trade-Off Between Inflation and Unemployment52 Questions

Exam 36: Supply-Side Policies57 Questions

Exam 37: Common Currency Areas and European Monetary Union55 Questions

Exam 38: The Financial Crisis and Sovereign Debt60 Questions

Select questions type

Equilibrium in a competitive market maximizes total surplus.

Free

(True/False)

4.9/5  (38)

(38)

Correct Answer: Verified

Verified

True

Producer surplus is the area above the supply curve and below the price.

Free

(True/False)

4.9/5 (42)

Correct Answer:Verified

True

Which of the following best explains the source of consumer surplus for a good?

Free

(Multiple Choice)

4.8/5 (29)

Correct Answer:Verified

A

Other things being equal, what happens to producer surplus when the price of a good rises? Illustrate your answer on a supply curve.

(Essay)

4.8/5 (37)

If a benevolent social planner chooses to produce more than the equilibrium quantity of a good, then

(Multiple Choice)

4.9/5 (41)

Donald produces nails at a cost of €200 per ton. If he sells the nails for €350 per ton, his producer surplus per ton is

(Multiple Choice)

4.9/5 (34)

Suppose there are three identical vases available to be purchased. Buyer 1 is willing to pay €30 for one, buyer 2 is willing to pay €25 for one, and buyer 3 is willing to pay €20 for one. If the price is €25, how many vases will be sold and what is the value of consumer surplus in this market?

(Multiple Choice)

4.8/5 (33)

This table refers to five possible buyers' willingness to pay for a take-away meal. ?

Buyer Willingness To Pay David 8.50 Laura 7.00 Megan 5.50 Mallory 4.00 Audrey 3.50

?

Refer to the table above. Which of the following is not true?

?

(Multiple Choice)

4.8/5 (33)

This table refers to five possible buyers' willingness to pay for a take-away meal. ?

Buyer Willingness To Pay David 8.50 Laura 7.00 Megan 5.50 Mallory 4.00 Audrey 3.50

?

Refer to the table above. If the market price is €3.80,

?

(Multiple Choice)

4.9/5 (39)

An increase in the price of a good along a stationary supply curve

(Multiple Choice)

4.9/5 (28)

If Gina sells a shirt for €40, and her producer surplus from the sale is €32, her cost must have been

(Multiple Choice)

4.9/5 (34)

If your willingness to pay for a hamburger is €3.00 and the price is €2.00, your consumer surplus is €5.00.

(True/False)

4.9/5 (30)

If demand increases when supply is perfectly price elastic, then

(Multiple Choice)

4.9/5 (40)

In general, if a benevolent social planner wanted to maximize the total benefits received by buyers and sellers in a market, the planner should

(Multiple Choice)

4.7/5 (31)

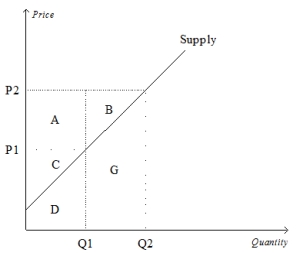

Refer to the image below. When the price is P2, producer surplus is

(Multiple Choice)

4.8/5 (39)

Free markets are efficient because they allocate output to buyers who have a willingness to pay that is below the price.

(True/False)

4.8/5 (29)

Other things equal, what happens to consumer surplus if the price of a good falls? Why? Illustrate using a demand curve.

(Essay)

4.9/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)