Exam 6: Background to Supply: Firms in Competitive Markets

Exam 1: What Is Economics59 Questions

Exam 2: Thinking Like an Economist54 Questions

Exam 3: The Market Forces of Supply and Demand56 Questions

Exam 4: Elasticity and Its Applications58 Questions

Exam 5: Background to Demand: Consumer Choices61 Questions

Exam 6: Background to Supply: Firms in Competitive Markets54 Questions

Exam 7: Consumers, Producers and the Efficiency of Markets56 Questions

Exam 8: Supply, Demand and Government Policies51 Questions

Exam 9: The Tax System48 Questions

Exam 10: Public Goods, Common Resources and Merit Goods58 Questions

Exam 11: Market Failure and Externalities61 Questions

Exam 12: Information and Behavioural Economics60 Questions

Exam 13: Firms Production Decisions47 Questions

Exam 14: Market Structures I: Monopoly57 Questions

Exam 15: Market Structures Ii: Monopolistic Competition59 Questions

Exam 16: Market Structures Iii: Oligopoly55 Questions

Exam 17: The Economics of Factor Markets60 Questions

Exam 18: Income Inequality and Poverty60 Questions

Exam 19: Interdependence and the Gains From Trade56 Questions

Exam 20: Measuring a Nations Well-Being60 Questions

Exam 21: Measuring the Cost of Living59 Questions

Exam 22: Production and Growth60 Questions

Exam 23: Unemployment60 Questions

Exam 24: Saving, Investment and the Financial System60 Questions

Exam 25: The Basic Tools of Finance57 Questions

Exam 26: Issues in Financial Markets59 Questions

Exam 27: The Monetary System60 Questions

Exam 28: Money Growth and Inflation59 Questions

Exam 29: Open-Economy Macroeconomics: Basic Concepts60 Questions

Exam 30: A Macroeconomic Theory of the Open Economy61 Questions

Exam 31: Business Cycles55 Questions

Exam 32: Keynesian Economics and the Is-Lm Analysis60 Questions

Exam 33: Aggregate Demand and Aggregate Supply60 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand41 Questions

Exam 35: The Short-Run Trade-Off Between Inflation and Unemployment52 Questions

Exam 36: Supply-Side Policies57 Questions

Exam 37: Common Currency Areas and European Monetary Union55 Questions

Exam 38: The Financial Crisis and Sovereign Debt60 Questions

Select questions type

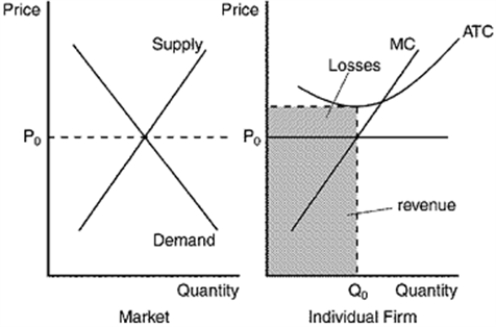

Use a graph to demonstrate the circumstances that would prevail in a perfectly competitive market where firms are experiencing economic losses. Identify costs, revenue, and the economic losses on your graph. Using your graph, determine whether an individual firm will shut down in the short run, or choose to remain in the market. Explain your answer.

Free

(Essay)

4.7/5  (37)

(37)

Correct Answer: Verified

Verified

The losses and revenues are identified on the individual firm's graph. Total cost is equal to the sum of the losses and revenue (because profit/loss=TR-TC, so TC=TR + profit/loss). The decision about whether this firm shuts down or remains in the market depends upon the position of average variable cost. If average variable cost is below P0 at output level Q0, the firm will remain in the market. If average variable cost is above P0 at output level Q0 the firm will shut down in the short run.

A firm maximizes profit when it produces output up to the point where marginal cost equals marginal revenue.

Free

(True/False)

4.9/5 (36)

Correct Answer:Verified

True

In the short run, the market supply curve for a good is the sum of the quantities supplied by each firm at each price.

Free

(True/False)

4.8/5 (37)

Correct Answer:Verified

True

Bob Edwards owns a bagel shop. Bob hires an economist who assesses the shape of the bagel shop's average total cost (ATC) curve as a function of the number of bagels produced. The results indicate a U-shaped average total cost curve. Bob's economist explains that ATC is U-shaped for two reasons. The first is the existence of diminishing marginal product, which causes it to rise. What would be the second reason? Assume that the marginal cost curve is linear. (Hint: The second reason relates to average fixed cost)

(Essay)

4.9/5 (33)

Wages and salaries paid to workers are an example of implicit costs of production.

(True/False)

4.9/5 (39)

Use a graph to demonstrate the circumstances that would prevail in a competitive market where firms are earning economic profits. Can this scenario be maintained in the long run? Explain your answer.

(Essay)

4.7/5 (26)

In the short run, the competitive firm's supply curve is the

(Multiple Choice)

4.8/5 (31)

Which of the following markets would most closely satisfy the requirements for a competitive market?

(Multiple Choice)

5.0/5 (33)

Russell's Shoe Repair also produces custom-made shoes. When Mr. Russell produces 12 pairs a week, the marginal cost (MC) of the twelfth pair is €84, and the marginal revenue (MR) of that unit is €70. What would you advise Mr. Russell to do?

(Multiple Choice)

4.8/5 (29)

In a perfectly competitive market, the horizontal sum of all the individual firms' supply curves is

(Multiple Choice)

4.7/5 (33)

In the long-run, some firms will exit the market if the price of the good offered for sale is less than

(Multiple Choice)

4.9/5 (37)

What are opportunity costs? How do explicit and implicit costs relate to opportunity costs?

(Essay)

5.0/5 (48)

Nicole owns a small pottery factory. She can make 1,000 pieces of pottery per year and sell them for €100 each. It costs Nicole €20,000 for the raw materials to produce the 1,000 pieces of pottery. She has invested €100,000 in her factory and equipment: €50,000 from her savings and €50,000 borrowed at 10 per cent. (Assume that she could have loaned her money out at 10 per cent, too.) Nicole can work at a competing pottery factory for €40,000 per year. The accounting profit at Nicole's pottery factory is

(Multiple Choice)

4.9/5 (35)

In the short run, if the price a firm receives for a good is above its average variable costs but below its average total costs of production, the firm will temporarily shut down.

(True/False)

4.9/5 (31)

If a production function exhibits diminishing marginal product, its slope

(Multiple Choice)

4.9/5 (34)

In long-run equilibrium in a competitive market, firms are operating at

(Multiple Choice)

4.8/5 (37)

Describe the difference between average revenue and marginal revenue. Why are both of these revenue measures important to a profit-maximizing firm?

(Essay)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)