Exam 3: The Market Forces of Supply and Demand

Exam 1: What Is Economics59 Questions

Exam 2: Thinking Like an Economist54 Questions

Exam 3: The Market Forces of Supply and Demand56 Questions

Exam 4: Elasticity and Its Applications58 Questions

Exam 5: Background to Demand: Consumer Choices61 Questions

Exam 6: Background to Supply: Firms in Competitive Markets54 Questions

Exam 7: Consumers, Producers and the Efficiency of Markets56 Questions

Exam 8: Supply, Demand and Government Policies51 Questions

Exam 9: The Tax System48 Questions

Exam 10: Public Goods, Common Resources and Merit Goods58 Questions

Exam 11: Market Failure and Externalities61 Questions

Exam 12: Information and Behavioural Economics60 Questions

Exam 13: Firms Production Decisions47 Questions

Exam 14: Market Structures I: Monopoly57 Questions

Exam 15: Market Structures Ii: Monopolistic Competition59 Questions

Exam 16: Market Structures Iii: Oligopoly55 Questions

Exam 17: The Economics of Factor Markets60 Questions

Exam 18: Income Inequality and Poverty60 Questions

Exam 19: Interdependence and the Gains From Trade56 Questions

Exam 20: Measuring a Nations Well-Being60 Questions

Exam 21: Measuring the Cost of Living59 Questions

Exam 22: Production and Growth60 Questions

Exam 23: Unemployment60 Questions

Exam 24: Saving, Investment and the Financial System60 Questions

Exam 25: The Basic Tools of Finance57 Questions

Exam 26: Issues in Financial Markets59 Questions

Exam 27: The Monetary System60 Questions

Exam 28: Money Growth and Inflation59 Questions

Exam 29: Open-Economy Macroeconomics: Basic Concepts60 Questions

Exam 30: A Macroeconomic Theory of the Open Economy61 Questions

Exam 31: Business Cycles55 Questions

Exam 32: Keynesian Economics and the Is-Lm Analysis60 Questions

Exam 33: Aggregate Demand and Aggregate Supply60 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand41 Questions

Exam 35: The Short-Run Trade-Off Between Inflation and Unemployment52 Questions

Exam 36: Supply-Side Policies57 Questions

Exam 37: Common Currency Areas and European Monetary Union55 Questions

Exam 38: The Financial Crisis and Sovereign Debt60 Questions

Select questions type

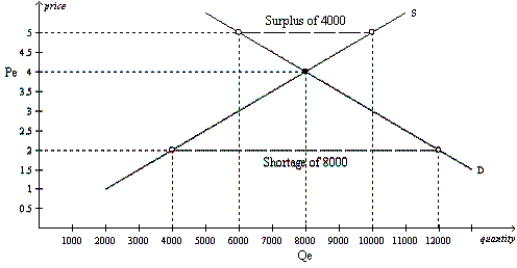

a) Given the table below, graph the demand and supply curves for flashlights. Make certain to label the equilibrium price and equilibrium quantity.

Price Quantity Demanded Per Month Quantity Supplied Per Month 5 6,000 10,000 4 8,000 8,000 3 10,000 6,000 2 12,000 4,000 1 14,000 2,000

b) What is the equilibrium price and the equilibrium quantity?

c) Suppose the price is currently €5. What problem would exist in the market? What would you expect to happen to price? Show this on your graph.

d) Suppose the price is currently €2. What problem would exist in the market? What would you expect to happen to price? Show this on your graph.

Free

(Essay)

4.9/5  (33)

(33)

Correct Answer: Verified

Verified

a.  b. The equilibrium price (Pe) is €4 and the equilibrium quantity (Qe) is 8,000.

b. The equilibrium price (Pe) is €4 and the equilibrium quantity (Qe) is 8,000.

c. A surplus of 4,000 flashlights would be the problem in the market, and we would expect the price to fall.

d. A shortage of 8,000 flashlights would be the problem in the market, and we would expect the price to rise.

Explain the difference between these two statements.

a. A rise in price leads to a decrease in quantity demanded.

b. A rise in price is caused by an increase in demand.

Free

(Essay)

4.8/5 (24)

Correct Answer:Verified

a. The law of demand states that if prices rise consumers will buy less.

b. It the demand curve shifts outwards to the right, then prices will rise as a new market equilibrium is reached. Demand might increase at each and every price for a product for a number of reasons including a rise in people's incomes or a rise in population.

When the price of a good is below the equilibrium price, it causes a surplus.

Free

(True/False)

4.9/5 (37)

Correct Answer:Verified

False

If Coke and Pepsi are substitutes, an increase in the price of Coke will cause an increase in the equilibrium price and quantity bought and sold in the market for Pepsi.

(True/False)

4.9/5 (40)

Explain why the relationship between price and quantity demanded is known as the 'law of demand'.

(Essay)

4.8/5 (23)

If a drought destroyed half of the French garlic crop at a time when the health benefits of garlic were being well publicized, economists would expect that in the market for garlic

(Multiple Choice)

5.0/5 (34)

Which of the following are most likely to be an inferior good?

(Multiple Choice)

4.7/5 (30)

Suppose that a large dairy farmer is able to raise the market price of milk by withholding milk supply from the market. In this instance,

(Multiple Choice)

4.8/5 (33)

Fill in the table below, showing whether equilibrium price and equilibrium quantity go up, go down, stay the same, or change ambiguously.

No Change in Supply An Increase in Supply A Decrease in Supply No Change in Demand An Increase in Demand A Decrease in Demand

(Essay)

4.9/5 (35)

Which of the following shifts the demand for watches to the right?

(Multiple Choice)

4.8/5 (31)

Suppose a frost destroys much of the Florida orange crop. At the same time, suppose consumer tastes shift toward orange juice. What would we expect to happen to the equilibrium price and quantity in the market for orange juice?

(Multiple Choice)

5.0/5 (39)

Because there are many buyers and sellers in a perfectly competitive market, neither has any power to influence price. They are said to be price takers.

(True/False)

4.8/5 (31)

Consider a market in equilibrium. Firms who advertise in this market are attempting to shift the

(Multiple Choice)

4.8/5 (30)

List at least five of the seven assumptions upon which the model of supply and demand is based.

(Essay)

4.9/5 (36)

Refer to Table 3-1. Given this data, the equilibrium price and quantity of CD players are ?

Table 3-1 QUANTITY QUANTITY DEMANDED SUPPLIED 100 1000 100 150 900 300 200 800 500 250 600 600 300 300 650

?

(Multiple Choice)

4.9/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)