Exam 6: Differential Analysis: the Key to Decision Making

Exam 1: Managerial Accounting and Cost Concepts299 Questions

Exam 2: Costvolumeprofit Relationships260 Questions

Exam 3: Joborder Costing: Calculating Unit Product Costs292 Questions

Exam 4: Variable Costing and Segment Reporting: Tools for Management291 Questions

Exam 5: Activitybased Costing: a Tool to Aid Decision Making213 Questions

Exam 6: Differential Analysis: the Key to Decision Making203 Questions

Exam 7: Capital Budgeting Decisions179 Questions

Exam 8: Master Budgeting236 Questions

Exam 9: Flexible Budgets and Performance Analysis417 Questions

Exam 10: Standard Costs and Variances247 Questions

Exam 11: Performance Measurement in Decentralized Organizations180 Questions

Exam 12: Cost of Quality66 Questions

Exam 13: Analyzing Mixed Costs82 Questions

Exam 14: Activity-Based Absorption Costing20 Questions

Exam 15: the Predetermined Overhead Rate and Capacity42 Questions

Exam 16: Super-Variable Costing49 Questions

Exam 17: Time-Driven Activity-Based Costing: a Microsoft Excel-Based Approach123 Questions

Exam 18: Pricing Decisions149 Questions

Exam 19: the Concept of Present Value16 Questions

Exam 20: Income Taxes and the Net Present Value Method150 Questions

Exam 21: Predetermined Overhead Rates and Overhead Analysis in a Standard Costing System177 Questions

Exam 22: Transfer Pricing102 Questions

Exam 22: Service Department Charges44 Questions

Select questions type

Which of the following costs are always irrelevant in decision making?

(Multiple Choice)

4.8/5  (43)

(43)

Fixed costs are irrelevant in decisions about whether a product should be dropped.

(True/False)

4.9/5 (38)

The management of Wengel Corporation is considering dropping product B90D. Data from the company's accounting system appear below:

All fixed expenses of the company are fully allocated to products in the company's accounting system. Further investigation has revealed that $173,000 of the fixed manufacturing expenses and $150,000 of the fixed selling and administrative expenses are avoidable if product B90D is discontinued.

Required:

What would be the financial advantage (disadvantage) of dropping B90D? Should the product be dropped? Show your work!

All fixed expenses of the company are fully allocated to products in the company's accounting system. Further investigation has revealed that $173,000 of the fixed manufacturing expenses and $150,000 of the fixed selling and administrative expenses are avoidable if product B90D is discontinued.

Required:

What would be the financial advantage (disadvantage) of dropping B90D? Should the product be dropped? Show your work!

(Essay)

4.8/5 (38)

Wood Carving Corporation manufactures three products. Because of a recent lack of skilled wood carvers, the corporation has had a shortage of available labor hours. The following per unit data relates to the three products of the corporation:  Assume that Wood Carving only has 1,800 labor hours available next month. Also assume that Wood Carving can only sell 800 units of each product in a given month. What is the maximum amount of contribution margin that Wood Carving can generate next month given this labor hour shortage?

Assume that Wood Carving only has 1,800 labor hours available next month. Also assume that Wood Carving can only sell 800 units of each product in a given month. What is the maximum amount of contribution margin that Wood Carving can generate next month given this labor hour shortage?

(Multiple Choice)

4.9/5 (39)

A customer has requested that Lewelling Corporation fill a special order for 9,000 units of product S47 for $20.50 a unit. While the product would be modified slightly for the special order, product S47's normal unit product cost is $14.40:  Assume that direct labor is a variable cost. The special order would have no effect on the company's total fixed manufacturing overhead costs. The customer would like modifications made to product S47 that would increase the variable costs by $5.00 per unit and that would require an investment of $36,000 in special molds that would have no salvage value. This special order would have no effect on the company's other sales. The company has ample spare capacity for producing the special order. The annual financial advantage (disadvantage) for the company as a result of accepting this special order should be:

Assume that direct labor is a variable cost. The special order would have no effect on the company's total fixed manufacturing overhead costs. The customer would like modifications made to product S47 that would increase the variable costs by $5.00 per unit and that would require an investment of $36,000 in special molds that would have no salvage value. This special order would have no effect on the company's other sales. The company has ample spare capacity for producing the special order. The annual financial advantage (disadvantage) for the company as a result of accepting this special order should be:

(Multiple Choice)

4.9/5 (30)

The book value of an old machine is always considered an opportunity cost in a decision.

(True/False)

4.8/5 (38)

Foto Company makes 50,000 units per year of a part it uses in the products it manufactures. The unit product cost of this part is computed as follows:

Direct materials \ 12.00 Direct labor 10.10 Variable manufacturing overhead 2.00 Fixed manufacturing overhead 14.10 Unit product cost \ 38.20 An outside supplier has offered to sell the company all of these parts it needs for $37.30 a unit. If the company accepts this offer, the facilities now being used to make the part could be used to make more units of a product that is in high demand. The additional contribution margin on this other product would be $310,000 per year.

If the part were purchased from the outside supplier, all of the direct labor cost of the part would be avoided. However, $9.70 of the fixed manufacturing overhead cost being applied to the part would continue even if the part were purchased from the outside supplier. This fixed manufacturing overhead cost would be applied to the company's remaining products.

Required:

a. How much of the unit product cost of $38.20 is relevant in the decision of whether to make or buy the part?

b. What is the financial advantage (disadvantage) of purchasing the part rather than making it?

c. What is the maximum amount the company should be willing to pay an outside supplier per unit for the part if the supplier commits to supplying all 50,000 units required each year?

(Essay)

4.9/5 (35)

Hodge Inc. has some material that originally cost $74,600. The material has a scrap value of $57,400 as is, but if reworked at a cost of $1,500, it could be sold for $54,400. What would be the financial advantage (disadvantage) of reworking and selling the material rather than selling it as is as scrap?

(Multiple Choice)

4.8/5 (31)

Marsdon Company has an annual production capacity of 15,000 units. The costs associated with production and sale of the company's product are given below:

Manufacturing costs: Variable \ 12 per unit Fixed (annual cost) \ 90,000 Selling and administrative costs: Variable (sales commissions) \ 3 per unit Fixed (annual cost) \ 60,000 The company presently is selling 12,000 units annually at a selling price of $28 each. A special order has been received from a distributor who wants to purchase 3,000 units at a special price of $20 each. Regular sales would not be affected by this order and the order could be filled without any impact on total fixed costs. Sales commissions on the special order would be reduced by one-third.

Required:

Determine whether the company should accept the special order.

(Essay)

4.9/5 (32)

Ahrends Corporation makes 70,000 units per year of a part it uses in the products it manufactures. The unit product cost of this part is computed as follows:  An outside supplier has offered to sell the company all of these parts it needs for $48.50 a unit. If the company accepts this offer, the facilities now being used to make the part could be used to make more units of a product that is in high demand. The additional contribution margin on this other product would be $273,000 per year.

If the part were purchased from the outside supplier, all of the direct labor cost of the part would be avoided. However, $8.20 of the fixed manufacturing overhead cost being applied to the part would continue even if the part were purchased from the outside supplier. This fixed manufacturing overhead cost would be applied to the company's remaining products.

How much of the unit product cost of $54.90 is relevant in the decision of whether to make or buy the part? (Round your intermediate calculations to 2 decimal places.)

An outside supplier has offered to sell the company all of these parts it needs for $48.50 a unit. If the company accepts this offer, the facilities now being used to make the part could be used to make more units of a product that is in high demand. The additional contribution margin on this other product would be $273,000 per year.

If the part were purchased from the outside supplier, all of the direct labor cost of the part would be avoided. However, $8.20 of the fixed manufacturing overhead cost being applied to the part would continue even if the part were purchased from the outside supplier. This fixed manufacturing overhead cost would be applied to the company's remaining products.

How much of the unit product cost of $54.90 is relevant in the decision of whether to make or buy the part? (Round your intermediate calculations to 2 decimal places.)

(Multiple Choice)

4.9/5 (35)

A cost that is traceable to a segment through activity-based costing is always an avoidable cost for decision making.

(True/False)

4.9/5 (32)

Accepting a special order will improve overall net operating income if the revenue from the special order exceeds:

(Multiple Choice)

4.8/5 (37)

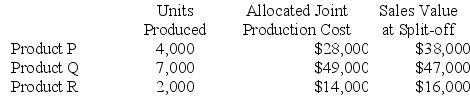

Bowen Company produces products P, Q, and R from a joint production process. Each product may be sold at the split-off point or be processed further. Joint production costs of $81,000 per year are allocated to the products based on the relative number of units produced. Data for Bowen's operations for the current year are as follows:

Product P can be processed beyond the split-off point for an additional cost of $10,000 and can then be sold for $50,000. Product Q can be processed beyond the split-off point for an additional cost of $35,000 and can then be sold for $65,000. Product R can be processed beyond the split-off point for an additional cost of $6,000 and can then be sold for $25,000.

Required:

Which products should be processed beyond the split-off point?

Product P can be processed beyond the split-off point for an additional cost of $10,000 and can then be sold for $50,000. Product Q can be processed beyond the split-off point for an additional cost of $35,000 and can then be sold for $65,000. Product R can be processed beyond the split-off point for an additional cost of $6,000 and can then be sold for $25,000.

Required:

Which products should be processed beyond the split-off point?

(Essay)

4.8/5 (39)

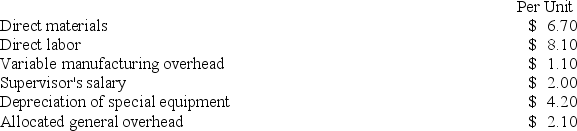

Norgaard Corporation makes 8,000 units of part G25 each year. This part is used in one of the company's products. The company's Accounting Department reports the following costs of producing the part at this level of activity:  An outside supplier has offered to make and sell the part to the company for $21.20 each. If this offer is accepted, the supervisor's salary and all of the variable costs, including direct labor, can be avoided. The special equipment used to make the part was purchased many years ago and has no salvage value or other use. The allocated general overhead represents fixed costs of the entire company. If the outside supplier's offer were accepted, only $2,000 of these allocated general overhead costs would be avoided. In addition, the space used to produce part G25 would be used to make more of one of the company's other products, generating an additional segment margin of $16,000 per year for that product.

The annual financial advantage (disadvantage) for the company as a result of buying part G25 from the outside supplier should be:

An outside supplier has offered to make and sell the part to the company for $21.20 each. If this offer is accepted, the supervisor's salary and all of the variable costs, including direct labor, can be avoided. The special equipment used to make the part was purchased many years ago and has no salvage value or other use. The allocated general overhead represents fixed costs of the entire company. If the outside supplier's offer were accepted, only $2,000 of these allocated general overhead costs would be avoided. In addition, the space used to produce part G25 would be used to make more of one of the company's other products, generating an additional segment margin of $16,000 per year for that product.

The annual financial advantage (disadvantage) for the company as a result of buying part G25 from the outside supplier should be:

(Multiple Choice)

4.9/5 (48)

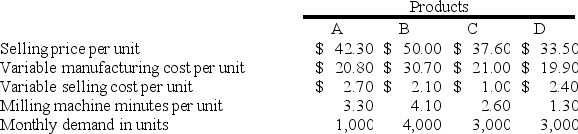

Cranston Corporation makes four products in a single facility. Data concerning these products appear below:  The milling machines are potentially the constraint in the production facility. A total of 28,200 minutes are available per month on these machines.

Which product makes the MOST profitable use of the milling machines? (Round your intermediate calculations to 2 decimal places.)

The milling machines are potentially the constraint in the production facility. A total of 28,200 minutes are available per month on these machines.

Which product makes the MOST profitable use of the milling machines? (Round your intermediate calculations to 2 decimal places.)

(Multiple Choice)

4.8/5 (32)

A cost that can be avoided by choosing one alternative over another is relevant for decision purposes.

(True/False)

4.8/5 (31)

The management of Schmader Corporation is considering dropping product M12C. Data from the company's accounting system appear below:

All fixed expenses of the company are fully allocated to products in the company's accounting system. Further investigation has revealed that $137,000 of the fixed manufacturing expenses and $79,000 of the fixed selling and administrative expenses are avoidable if product M12C is discontinued.

Required:

a. What is the net operating income earned by product M12C according to the company's accounting system? Show your work!

b. Determine the financial advantage (disadvantage) for the company of dropping product M12C. Should the product be dropped? Show your work!

All fixed expenses of the company are fully allocated to products in the company's accounting system. Further investigation has revealed that $137,000 of the fixed manufacturing expenses and $79,000 of the fixed selling and administrative expenses are avoidable if product M12C is discontinued.

Required:

a. What is the net operating income earned by product M12C according to the company's accounting system? Show your work!

b. Determine the financial advantage (disadvantage) for the company of dropping product M12C. Should the product be dropped? Show your work!

(Essay)

4.8/5 (37)

A complete income statement need not be prepared as part of a differential cost analysis.

(True/False)

4.9/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)