Exam 6: Differential Analysis: the Key to Decision Making

Exam 1: Managerial Accounting and Cost Concepts299 Questions

Exam 2: Costvolumeprofit Relationships260 Questions

Exam 3: Joborder Costing: Calculating Unit Product Costs292 Questions

Exam 4: Variable Costing and Segment Reporting: Tools for Management291 Questions

Exam 5: Activitybased Costing: a Tool to Aid Decision Making213 Questions

Exam 6: Differential Analysis: the Key to Decision Making203 Questions

Exam 7: Capital Budgeting Decisions179 Questions

Exam 8: Master Budgeting236 Questions

Exam 9: Flexible Budgets and Performance Analysis417 Questions

Exam 10: Standard Costs and Variances247 Questions

Exam 11: Performance Measurement in Decentralized Organizations180 Questions

Exam 12: Cost of Quality66 Questions

Exam 13: Analyzing Mixed Costs82 Questions

Exam 14: Activity-Based Absorption Costing20 Questions

Exam 15: the Predetermined Overhead Rate and Capacity42 Questions

Exam 16: Super-Variable Costing49 Questions

Exam 17: Time-Driven Activity-Based Costing: a Microsoft Excel-Based Approach123 Questions

Exam 18: Pricing Decisions149 Questions

Exam 19: the Concept of Present Value16 Questions

Exam 20: Income Taxes and the Net Present Value Method150 Questions

Exam 21: Predetermined Overhead Rates and Overhead Analysis in a Standard Costing System177 Questions

Exam 22: Transfer Pricing102 Questions

Exam 22: Service Department Charges44 Questions

Select questions type

Ibsen Company makes two products from a common input. Joint processing costs up to the split-off point total $43,200 a year. The company allocates these costs to the joint products on the basis of their total sales values at the split-off point. Each product may be sold at the split-off point or processed further. Data concerning these products appear below:

Required:

a. What is financial advantage (disadvantage) of processing Product X beyond the split-off point?

b. What is financial advantage (disadvantage) of processing Product Y beyond the split-off point?

c. What is the minimum amount the company should accept for Product X if it is to be sold at the split-off point?

d. What is the minimum amount the company should accept for Product Y if it is to be sold at the split-off point?

Required:

a. What is financial advantage (disadvantage) of processing Product X beyond the split-off point?

b. What is financial advantage (disadvantage) of processing Product Y beyond the split-off point?

c. What is the minimum amount the company should accept for Product X if it is to be sold at the split-off point?

d. What is the minimum amount the company should accept for Product Y if it is to be sold at the split-off point?

(Essay)

4.8/5  (39)

(39)

The constraint at Pickrel Corporation is time on a particular machine. The company makes three products that use this machine. Data concerning those products appear below:  Assume that sufficient time is available on the constrained machine to satisfy demand for all but the least profitable product. Up to how much should the company be willing to pay to acquire more of this constrained resource? (Round your intermediate calculations to 2 decimal places.)

Assume that sufficient time is available on the constrained machine to satisfy demand for all but the least profitable product. Up to how much should the company be willing to pay to acquire more of this constrained resource? (Round your intermediate calculations to 2 decimal places.)

(Multiple Choice)

4.9/5 (45)

A study has been conducted to determine if one of the departments in Carry Corporation should be discontinued. The contribution margin in the department is $80,000 per year. Fixed expenses charged to the department are $95,000 per year. It is estimated that $50,000 of these fixed expenses could be eliminated if the department is discontinued. These data indicate that if the department is discontinued, the yearly financial advantage (disadvantage) for the company would be:

(Multiple Choice)

4.8/5 (37)

Consistency demands that a cost that is relevant in one decision be regarded as relevant in other decisions as well.

(True/False)

4.7/5 (39)

The opportunity cost of making a component part in a factory with excess capacity for which there is no alternative use is:

(Multiple Choice)

4.8/5 (35)

Banfield Corporation makes three products that use compound W, the current constrained resource. Data concerning those products appear below:  Rank the products in order of their current profitability from most profitable to least profitable. In other words, rank the products in the order in which they should be emphasized. (Round your intermediate calculations to 2 decimal places.)

Rank the products in order of their current profitability from most profitable to least profitable. In other words, rank the products in the order in which they should be emphasized. (Round your intermediate calculations to 2 decimal places.)

(Multiple Choice)

4.8/5 (45)

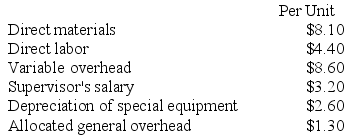

Recher Corporation uses part Q89 in one of its products. The company's Accounting Department reports the following costs of producing the 8,000 units of the part that are needed every year.

An outside supplier has offered to make the part and sell it to the company for $27.60 each. If this offer is accepted, the supervisor's salary and all of the variable costs, including direct labor, can be avoided. The special equipment used to make the part was purchased many years ago and has no salvage value or other use. The allocated general overhead represents fixed costs of the entire company. If the outside supplier's offer were accepted, only $3,000 of these allocated general overhead costs would be avoided. In addition, the space used to produce part Q89 could be used to make more of one of the company's other products, generating an additional segment margin of $16,000 per year for that product.

Required:

a. Prepare a report that shows the financial impact of buying part Q89 from the supplier rather than continuing to make it inside the company.

b. Which alternative should the company choose?

An outside supplier has offered to make the part and sell it to the company for $27.60 each. If this offer is accepted, the supervisor's salary and all of the variable costs, including direct labor, can be avoided. The special equipment used to make the part was purchased many years ago and has no salvage value or other use. The allocated general overhead represents fixed costs of the entire company. If the outside supplier's offer were accepted, only $3,000 of these allocated general overhead costs would be avoided. In addition, the space used to produce part Q89 could be used to make more of one of the company's other products, generating an additional segment margin of $16,000 per year for that product.

Required:

a. Prepare a report that shows the financial impact of buying part Q89 from the supplier rather than continuing to make it inside the company.

b. Which alternative should the company choose?

(Essay)

4.9/5 (37)

An avoidable fixed production cost incurred before the split-off point in a joint process is relevant in a sell or process further decision.

(True/False)

5.0/5 (45)

Product X-547 is one of the joint products in a joint manufacturing process. Management is considering whether to sell X-547 at the split-off point or to process X-547 further into Xylene. The following data have been gathered: I. Selling price of X-547

II) Variable cost of processing X-547 into Xylene.

III) The avoidable fixed costs of processing X-547 into Xylene.

IV) The selling price of Xylene.

V) The joint cost of the process from which X-547 is produced.

Which of the above items are relevant in a decision of whether to sell the X-547 as is or process it further into Xylene?

A) I, II, and IV.

B) I, II, III, and IV.

C) II, III, and V.

D) I, II, III, and V.

(Essay)

4.7/5 (35)

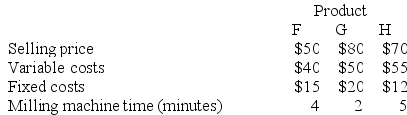

Garson, Inc. produces three products. Data concerning the selling prices and unit costs of the three products appear below:

Fixed costs are applied to the products on the basis of direct labor hours.

Demand for the three products exceeds the company's productive capacity. The milling machine is the constraint, with only 2,400 minutes of milling machine time available this week.

Required:

a. Given the milling machine constraint, which product should be emphasized? Support your answer with appropriate calculations.

b. Assuming that there is still unfilled demand for the product that the company should emphasize in part (a) above, up to how much should the company be willing to pay for an additional hour of milling machine time?

Fixed costs are applied to the products on the basis of direct labor hours.

Demand for the three products exceeds the company's productive capacity. The milling machine is the constraint, with only 2,400 minutes of milling machine time available this week.

Required:

a. Given the milling machine constraint, which product should be emphasized? Support your answer with appropriate calculations.

b. Assuming that there is still unfilled demand for the product that the company should emphasize in part (a) above, up to how much should the company be willing to pay for an additional hour of milling machine time?

(Essay)

4.8/5 (38)

Winder Corporation is a specialty component manufacturer with idle capacity. Management would like to use its extra capacity to generate additional profits. A potential customer has offered to buy 3,000 units of component QEA. Each unit of QEA requires 5 units of material F85 and 5 units of material E71. Data concerning these two materials follow:  Material F85 is in use in many of the company's products and is routinely replenished. Material E71 is no longer used by the company in any of its normal products and existing stocks would not be replenished once they are used up.

What would be the relevant cost of the materials, in total, for purposes of determining a minimum acceptable price for the order for product QEA?

Material F85 is in use in many of the company's products and is routinely replenished. Material E71 is no longer used by the company in any of its normal products and existing stocks would not be replenished once they are used up.

What would be the relevant cost of the materials, in total, for purposes of determining a minimum acceptable price for the order for product QEA?

(Multiple Choice)

4.9/5 (39)

Sunk costs and future costs that do not differ between the alternatives may or may not be relevant in a decision.

(True/False)

4.8/5 (29)

Mcniff Corporation makes a range of products. The company's predetermined overhead rate is $28 per direct labor-hour, which was calculated using the following budgeted data:

Variable manufacturing overhead \ 180,000 Fixed manufacturing overhead \ 380,000 Direct labor-hours 20,000 Management is considering a special order for 200 units of product O96S at $122 each. The normal selling price of product O96S is $149 and the unit product cost is determined as follows:

Direct materials \ 67.00 Direct labor 32.00 Manufacturing overhead applied 44.80 Unit product cost \ 143.80 If the special order were accepted, normal sales of this and other products would not be affected. The company has ample excess capacity to produce the additional units. Assume that direct labor is a variable cost, variable manufacturing overhead is really driven by direct labor-hours, and total fixed manufacturing overhead would not be affected by the special order.

Required:

The financial advantage (disadvantage) for the company as a result of accepting this special order would be:

(Essay)

4.8/5 (32)

A disadvantage of vertical integration is that by pooling demand for parts from a number of companies, a supplier may be able to enjoy economies of scale that result in higher quality and lower cost than if every company makes its own parts.

(True/False)

4.8/5 (29)

Mae Refiners, Inc., processes sugar cane that it purchases from farmers. Sugar cane is processed in batches. A batch of sugar cane costs $60 to buy from farmers and $13 to crush in the company's plant. Two intermediate products, cane fiber and cane juice, emerge from the crushing process. The cane fiber can be sold as is for $29 or processed further for $13 to make the end product industrial fiber that is sold for $61. The cane juice can be sold as is for $40 or processed further for $28 to make the end product molasses that is sold for $67. What is the financial advantage (disadvantage) for the company from processing the intermediate product cane juice into molasses rather than selling it as is?

(Multiple Choice)

4.7/5 (44)

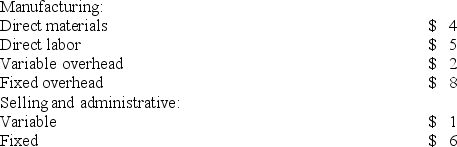

The following are Silver Corporation's unit costs of making and selling an item at a volume of 8,000 units per month (which represents the company's capacity):  Present sales amount to 7,000 units per month. An order has been received from a customer in a foreign market for 1,000 units. The order would not affect regular sales. Total fixed costs, both manufacturing and selling and administrative, would not be affected by this order. The variable selling and administrative costs would have to be incurred for this special order as well as all other sales. Assume that direct labor is a variable cost.

Assume the company has 50 units left over from last year which have small defects and which will have to be sold at a reduced price for scrap. The sale of these defective units will have no effect on the company's other sales. Which of the following costs is relevant in this decision?

Present sales amount to 7,000 units per month. An order has been received from a customer in a foreign market for 1,000 units. The order would not affect regular sales. Total fixed costs, both manufacturing and selling and administrative, would not be affected by this order. The variable selling and administrative costs would have to be incurred for this special order as well as all other sales. Assume that direct labor is a variable cost.

Assume the company has 50 units left over from last year which have small defects and which will have to be sold at a reduced price for scrap. The sale of these defective units will have no effect on the company's other sales. Which of the following costs is relevant in this decision?

(Multiple Choice)

4.9/5 (35)

Two or more products that are produced from a common input are known as joint products.

(True/False)

4.9/5 (28)

Drew Cane Products, Inc., processes sugar cane in batches. The company buys a batch of sugar cane from farmers for $90 which is then crushed in the company's plant at a cost of $11. Two intermediate products, cane fiber and cane juice, emerge from the crushing process. The cane fiber can be sold as is for $21 or processed further for $13 to make the end product industrial fiber that is sold for $45. The cane juice can be sold as is for $41 or processed further for $29 to make the end product molasses that is sold for $103. What is the financial advantage (disadvantage) for the company from processing one batch of sugar cane into the end products industrial fiber and molasses rather than not processing that batch at all?

(Multiple Choice)

4.9/5 (37)

A product whose revenues do not cover its variable costs and its traceable fixed costs should usually be dropped.

(True/False)

4.9/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)