Exam 15: Time-Series Forecasting and Index Numbers

Exam 1: Introduction to Statistics and Business Analytics180 Questions

Exam 2: Visualizing Data With Charts and Graphs113 Questions

Exam 3: Descriptive Statistics88 Questions

Exam 4: Probability104 Questions

Exam 5: Discrete Distributions98 Questions

Exam 6: Continuous Distributions105 Questions

Exam 7: Sampling and Sampling Distributions97 Questions

Exam 8: Statistical Inference: Estimation for Single Populations94 Questions

Exam 9: Statistical Inference: Hypothesis Testing for Single Populations123 Questions

Exam 10: Statistical Inferences About Two Populations97 Questions

Exam 11: Analysis of Variance and Design of Experiments133 Questions

Exam 12: Simple Regression Analysis and Correlation111 Questions

Exam 13: Multiple Regression Analysis90 Questions

Exam 14: Building Multiple Regression Models100 Questions

Exam 15: Time-Series Forecasting and Index Numbers103 Questions

Exam 16: Analysis of Categorical Data85 Questions

Exam 17: Nonparametric Statistics110 Questions

Exam 18: Statistical Quality Control99 Questions

Exam 19: Decision Analysis109 Questions

Select questions type

A stationary time-series data has only trend, but no cyclical or seasonal effects.

(True/False)

4.7/5  (45)

(45)

Calculating the "ratios of actuals to moving average" is a common step in time series decomposition.The results (the quotients)of this step estimate the ________.

(Multiple Choice)

4.8/5 (28)

Two popular general categories of smoothing techniques are exponential models and logarithmic models.

(True/False)

4.8/5 (39)

One of the main techniques for isolating the effects of seasonality is decomposition.

(True/False)

4.8/5 (36)

The first step of isolating seasonal effects is to remove the trend and cycles effects.

(True/False)

4.7/5 (32)

Linear regression models cannot be used to analyze quadratic trends in time-series data.

(True/False)

4.9/5 (42)

Given several years of quarterly data and finding the four quarter moving average from Q3 of the second year through Q2 of the third year would be placed on the decomposition table between which two quarters?

(Multiple Choice)

4.7/5 (31)

When constructing a weighted aggregate price index, the weights usually are _____.

(Multiple Choice)

4.9/5 (43)

The long-term general direction of data is referred to as series.

(True/False)

4.9/5 (30)

The effect of a four-quarter moving average on can be described as ______________ the seasonal effects of the data.

(Multiple Choice)

5.0/5 (28)

Use of a smoothing constant value greater than 0.5 in an exponential smoothing model gives more weight to ___________.

(Multiple Choice)

4.9/5 (40)

In exponential smoothing models, the value of the smoothing constant may be any number between ___________.

(Multiple Choice)

4.8/5 (31)

The following graph of a time-series data suggests a _______________ trend.

(Multiple Choice)

4.8/5 (35)

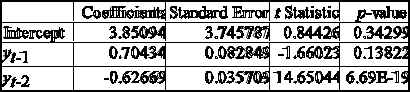

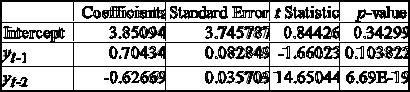

Analysis of data for an autoregressive forecasting model produced the following tables.

The forecasting model is __________.

The forecasting model is __________.

(Multiple Choice)

4.8/5 (34)

The motivation for using an index number is to ________________.

(Multiple Choice)

4.7/5 (43)

Forecast error is the difference between the value of the response variable and those of the explanatory variables.

(True/False)

4.7/5 (35)

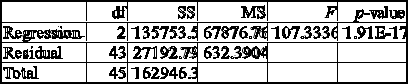

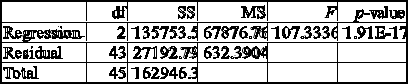

Analysis of data for an autoregressive forecasting model produced the following tables.

The actual values of this time series, y, were 228, 54, and 191 for May, June, and July, respectively.The predicted (forecast)value for August is __________.

The actual values of this time series, y, were 228, 54, and 191 for May, June, and July, respectively.The predicted (forecast)value for August is __________.

(Multiple Choice)

4.9/5 (33)

Time-series data are data gathered on a desired characteristic at a particular point in time.

(True/False)

4.8/5 (39)

If the trend equation is linear in time, the slope indicates the increase, or decrease when negative, in the forecasted value of the response value Y for the next time period.

(True/False)

4.8/5 (32)

Suppose that for a time-series model with one predictor, you compute a Durbin-Watson statistic D = 0.625.Assume that n = 30 and α = 0.05.Then your decision is ______.

(Multiple Choice)

4.9/5 (46)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)