Exam 13: Return, Risk, and the Security Market Line

Exam 1: Introduction to Corporate Finance256 Questions

Exam 2: Financial Statements, Cash Flow, and Taxes412 Questions

Exam 3: Working With Financial Statements408 Questions

Exam 4: Long-Term Financial Planning and Corporate Growth379 Questions

Exam 5: Introduction to Valuation: the Time Value of Money280 Questions

Exam 6: Discounted Cash Flow Valuation413 Questions

Exam 7: Interest Rates and Bond Valuation393 Questions

Exam 8: Stock Valuation399 Questions

Exam 9: Net Present Value and Other Investment Criteria415 Questions

Exam 10: Making Capital Investment Decisions363 Questions

Exam 11: Project Analysis and Evaluation425 Questions

Exam 12: Lessons From Capital Market History329 Questions

Exam 13: Return, Risk, and the Security Market Line416 Questions

Exam 14: Cost of Capital377 Questions

Exam 15: Raising Capital337 Questions

Exam 16: Financial Leverage and Capital Structure Policy383 Questions

Exam 17: Dividends and Dividend Policy376 Questions

Exam 18: Short-Term Finance and Planning424 Questions

Exam 19: Cash and Liquidity Management374 Questions

Exam 20: Credit and Inventory Management384 Questions

Exam 21: International Corporate Finance369 Questions

Exam 22: Leasing269 Questions

Exam 23: Mergers and Acquisitions335 Questions

Exam 24: Enterprise Risk Management300 Questions

Exam 25: Options and Corporate Securities445 Questions

Exam 26: Behavioural Finance: Implications for Financial Management76 Questions

Select questions type

The market has an expected rate of return of 9.8%. Long-term government bonds are expected to yield 4.5% and Treasury bills are expected to yield 3.4%. The inflation rate is 3.1%. What is the market risk premium?

(Multiple Choice)

4.8/5  (43)

(43)

Why do we need to make the switch from historical to expected? Why not use historical returns or expected returns for all analysis?

(Essay)

4.8/5 (30)

The Inferior Goods Co. stock is expected to earn 14% in a recession, 6% in a normal economy, and lose 4% in a booming economy. The probability of a boom is 20% while the probability of a normal economy is 55% and the chance of a recession is 25%. What is the expected rate of return on this stock?

(Multiple Choice)

4.9/5 (36)

Draw the SML and plot asset C such that it has less risk than the market but plots above the SML, and asset D such that it has more risk than the market and plots below the SML. (Be sure to indicate where the market portfolio is on your graph.) Explain how assets like C or D can plot as they do and explain why such pricing cannot persist in a market that is in equilibrium.

(Essay)

4.8/5 (44)

Diversifiable risks are generally associated with an individual firm or industry.

(True/False)

4.7/5 (40)

The rate of return on the common stock of Flowers by Flo is expected to be 14% in a boom economy, 8% in a normal economy, and only 2% in a recessionary economy. The probabilities of these economic states are 20% for a boom, 70% for a normal economy, and 10% for a recession. What is the variance of the returns on the common stock of Flowers by Flo?

(Multiple Choice)

4.8/5 (33)

For a stock with beta equal to 1.5 signifies that the stock has a 50% higher expected return than the average stock.

(True/False)

4.9/5 (36)

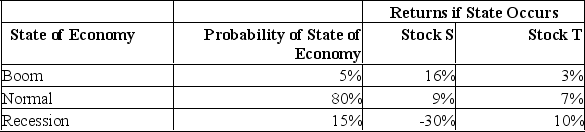

What is the standard deviation of a portfolio which is comprised of $8,400 invested in stock S and $3,600 in stock T?

(Multiple Choice)

4.7/5 (36)

What is the portfolio expected return and the portfolio beta if you invest 30% in A, 30% in B and 40% in the risk-free asset?

What is the portfolio expected return and the portfolio beta if you invest 30% in A, 30% in B and 40% in the risk-free asset?

(Multiple Choice)

4.7/5 (37)

The excess return earned by an asset that has a beta of 1.0 over that earned by a risk-free asset is referred to as the:

(Multiple Choice)

4.7/5 (36)

What is the portfolio weight of stock B given the following information?

(Multiple Choice)

5.0/5 (34)

Is it possible for an asset to have a negative beta? (Hint: yes) What would the expected return on such an asset be? Why?

(Essay)

4.7/5 (38)

You form a portfolio by investing equally in A (beta = 0.8), B (beta = 1.2), the risk-free asset, and the market portfolio. What is your portfolio beta?

(Multiple Choice)

4.7/5 (24)

An investment firm is considering a portfolio with equal weighting in a cyclical stock and a countercyclical stock. It is expected that there will be three economic states; Good, Average and Bad, each with equal probabilities of occurrence. The cyclical stock is expected to have returns of 12%, 5% and 1% in Good, Average and Bad economies respectively. The countercyclical stock is expected to have returns of -8%, 2% and 14% in Good, Average and Bad economies respectively. Given this information, calculate portfolio variance.

(Multiple Choice)

4.7/5 (33)

What is the expected return on asset A if it has a beta of 0.3, the expected market return is 14%, and the risk-free rate is 5%?

(Multiple Choice)

4.8/5 (36)

The standard deviation of a portfolio will tend to increase when:

(Multiple Choice)

4.9/5 (31)

Lower consumer spending than expected is considered an example of unsystematic risk.

(True/False)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)