Exam 13: Return, Risk, and the Security Market Line

Exam 1: Introduction to Corporate Finance256 Questions

Exam 2: Financial Statements, Cash Flow, and Taxes412 Questions

Exam 3: Working With Financial Statements408 Questions

Exam 4: Long-Term Financial Planning and Corporate Growth379 Questions

Exam 5: Introduction to Valuation: the Time Value of Money280 Questions

Exam 6: Discounted Cash Flow Valuation413 Questions

Exam 7: Interest Rates and Bond Valuation393 Questions

Exam 8: Stock Valuation399 Questions

Exam 9: Net Present Value and Other Investment Criteria415 Questions

Exam 10: Making Capital Investment Decisions363 Questions

Exam 11: Project Analysis and Evaluation425 Questions

Exam 12: Lessons From Capital Market History329 Questions

Exam 13: Return, Risk, and the Security Market Line416 Questions

Exam 14: Cost of Capital377 Questions

Exam 15: Raising Capital337 Questions

Exam 16: Financial Leverage and Capital Structure Policy383 Questions

Exam 17: Dividends and Dividend Policy376 Questions

Exam 18: Short-Term Finance and Planning424 Questions

Exam 19: Cash and Liquidity Management374 Questions

Exam 20: Credit and Inventory Management384 Questions

Exam 21: International Corporate Finance369 Questions

Exam 22: Leasing269 Questions

Exam 23: Mergers and Acquisitions335 Questions

Exam 24: Enterprise Risk Management300 Questions

Exam 25: Options and Corporate Securities445 Questions

Exam 26: Behavioural Finance: Implications for Financial Management76 Questions

Select questions type

It is NOT possible to construct a portfolio with zero variance of expected returns from assets whose expected returns have positive variance individually.

(True/False)

4.9/5  (43)

(43)

What is the value of systematic risk for a portfolio with 75% of the funds invested in A and 25% of the funds invested in B?

What is the value of systematic risk for a portfolio with 75% of the funds invested in A and 25% of the funds invested in B?

(Multiple Choice)

4.8/5 (29)

Unsystematic risk is rewarded when it exceeds the market level of unsystematic risk.

(True/False)

4.8/5 (33)

What is the portfolio beta if 75% of your money is invested in the market portfolio, and the remainder is invested in a risk-free asset?

(Multiple Choice)

4.7/5 (31)

If the portfolio beta is greater than one then the portfolio has more risk than the overall market.

(True/False)

4.8/5 (41)

If the standard deviation of return on the stocks of the S&P/TSX Composite Index has been approximately 24% per year over the last decade, it must be true that half of the firms in the index have a standard deviation of return below 24% over the same period.

(True/False)

4.8/5 (30)

What is the standard deviation of a portfolio with weights of 60% in security A and the remainder in security B?

(Multiple Choice)

4.8/5 (37)

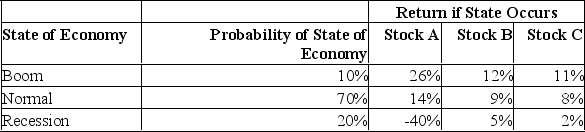

What is the standard deviation of a portfolio which is invested 10% in stock A, 35% in stock B and 55% in stock C?

(Multiple Choice)

4.8/5 (29)

Consider a portfolio made up of two risky assets and a risk-free asset. You invest 40% in asset A with a beta of 1.25 and 40% in asset B with a beta of 1.15. What is the beta of the portfolio?

(Multiple Choice)

4.7/5 (34)

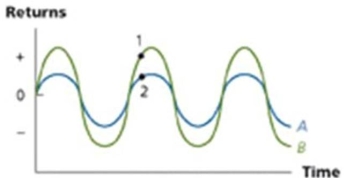

What relationship are the volatilities of stock A and B exhibiting?

(Multiple Choice)

4.8/5 (33)

The systematic risk principle implies that the _____ an asset depends only on that asset's systematic risk.

(Multiple Choice)

4.8/5 (32)

What is the beta of a portfolio comprised of the following securities?

(Multiple Choice)

4.7/5 (40)

The percentage of a portfolio's total value invested in a particular asset is called that asset's:

(Multiple Choice)

4.8/5 (29)

Which one of the following is an example of a nondiversifiable risk?

(Multiple Choice)

4.9/5 (33)

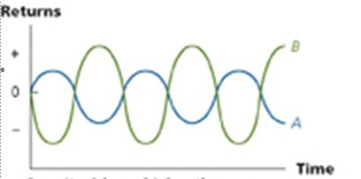

What relationship are the volatilities of stock A and B exhibiting?

(Multiple Choice)

4.8/5 (34)

A portfolio is comprised of five risky stocks. The standard deviations of these stocks are 5.6%, 12.8%, 2.3%, 8.9%, and 10.2%. The standard deviation of the portfolio:

(Multiple Choice)

4.8/5 (36)

Diversification works because firm-specific risk can be dramatically reduced if not eliminated.

(True/False)

4.8/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)