Exam 13: Return, Risk, and the Security Market Line

Exam 1: Introduction to Corporate Finance256 Questions

Exam 2: Financial Statements, Cash Flow, and Taxes412 Questions

Exam 3: Working With Financial Statements408 Questions

Exam 4: Long-Term Financial Planning and Corporate Growth379 Questions

Exam 5: Introduction to Valuation: the Time Value of Money280 Questions

Exam 6: Discounted Cash Flow Valuation413 Questions

Exam 7: Interest Rates and Bond Valuation393 Questions

Exam 8: Stock Valuation399 Questions

Exam 9: Net Present Value and Other Investment Criteria415 Questions

Exam 10: Making Capital Investment Decisions363 Questions

Exam 11: Project Analysis and Evaluation425 Questions

Exam 12: Lessons From Capital Market History329 Questions

Exam 13: Return, Risk, and the Security Market Line416 Questions

Exam 14: Cost of Capital377 Questions

Exam 15: Raising Capital337 Questions

Exam 16: Financial Leverage and Capital Structure Policy383 Questions

Exam 17: Dividends and Dividend Policy376 Questions

Exam 18: Short-Term Finance and Planning424 Questions

Exam 19: Cash and Liquidity Management374 Questions

Exam 20: Credit and Inventory Management384 Questions

Exam 21: International Corporate Finance369 Questions

Exam 22: Leasing269 Questions

Exam 23: Mergers and Acquisitions335 Questions

Exam 24: Enterprise Risk Management300 Questions

Exam 25: Options and Corporate Securities445 Questions

Exam 26: Behavioural Finance: Implications for Financial Management76 Questions

Select questions type

You would like to combine a risky stock with a beta of 1.8 with Treasury bills in such a way that the risk level of the portfolio is equivalent to the risk level of the overall market. What percentage of the portfolio should be invested in Treasury bills?

(Multiple Choice)

4.8/5  (37)

(37)

Delta is needed to estimate the amount of additional reward you will receive for purchasing a risky asset instead of a risk-free asset.

(True/False)

4.8/5 (48)

The principle of diversification states that spreading an investment over a number of assets will eliminate:

(Multiple Choice)

4.8/5 (34)

An investment firm is considering a portfolio with equal weighting in a cyclical stock and a countercyclical stock. It is expected that there will be three economic states; Good, Average and Bad, each with equal probabilities of occurrence. The cyclical stock is expected to have returns of 12%, 5% and 1% in Good, Average and Bad economies respectively. The countercyclical stock is expected to have returns of -8%, 2% and 14% in Good, Average and Bad economies respectively. Given this information, calculate portfolio expected return.

(Multiple Choice)

4.8/5 (29)

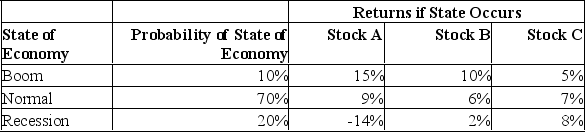

You own the following portfolio of stocks. What is the portfolio weight of stock C?

(Multiple Choice)

4.7/5 (33)

The majority of the benefits from portfolio diversification can generally be achieved with just _____ diverse securities.

(Multiple Choice)

4.9/5 (40)

Assume all of the stocks in a given industry fall as a result of an announcement about the general health of the economy. This is an example of systematic risk.

(True/False)

4.8/5 (32)

The market risk premium of an individual security is dependent upon the market rate of return.

(True/False)

4.8/5 (28)

What is the standard deviation of a portfolio which is invested 20% in stock A, 30% in stock B and 50% in stock C?

(Multiple Choice)

4.8/5 (30)

According to the CAPM, the expected return on a risky asset depends on three components. Describe each component, and explain its role in determining expected return.

(Essay)

4.7/5 (28)

The reward for bearing risk in the financial markets is called:

(Multiple Choice)

4.9/5 (39)

The Capital Asset Pricing Model (CAPM) assumes that a risk-free asset generally has a positive rate of return.

(True/False)

4.8/5 (34)

The expected return on Justus, Inc. stock is 15.63% while the expected return on the market is 12.4%. The beta of Justus's stock is 1.48. What is the risk-free rate of return?

(Multiple Choice)

4.9/5 (34)

You have a $1,000 portfolio which is invested in stocks A and B plus a risk-free asset. $400 is invested in stock A. Stock A has a beta of 1.3 and stock B has a beta of.7. How much needs to be invested in stock B if you want a portfolio beta of.90?

(Multiple Choice)

4.7/5 (27)

Asset A has an expected return of 15%. The expected market return is 14% and the risk-free rate is 4%. What is asset A's beta?

(Multiple Choice)

4.9/5 (34)

The ____________ return is that portion of total return attributable to information surprises.

(Multiple Choice)

4.7/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)