Exam 17: Standard Costing and Variance Analysis 1

Exam 1: Introduction to Management Accounting49 Questions

Exam 2: An Introduction to Cost Terms and Concepts64 Questions

Exam 3: Cost Assignment29 Questions

Exam 4: Accounting Entries for a Job Costing System15 Questions

Exam 5: Process Costing29 Questions

Exam 6: Joint and By-Product Costing61 Questions

Exam 7: Income Effects of Alternative Cost Accumulation Systems45 Questions

Exam 8: Cost-Volume-Profit Analysis60 Questions

Exam 9: Measuring Relevant Costs and Revenues for Decision-Making81 Questions

Exam 10: Activity-Based Costing40 Questions

Exam 11: Pricing Decisions and Profitability Analysis59 Questions

Exam 12: Decision-Making Under Conditions of Risk and Uncertainty29 Questions

Exam 13: Capital Investment Decisions: Appraisal Methods77 Questions

Exam 14: Capital Investment Decisions: the Impact of Capital Rationing, Taxation, Inflation and Risk25 Questions

Exam 15: The Budgeting Process86 Questions

Exam 16: Management Control Systems64 Questions

Exam 17: Standard Costing and Variance Analysis 181 Questions

Exam 18: Standard Costing and Variance Analysis 2: Further Aspects12 Questions

Exam 19: Divisional Financial Performance Measures51 Questions

Exam 20: Transfer Pricing in Divisionalized Companies50 Questions

Exam 21: Cost Management95 Questions

Exam 22: Strategic Management Accounting32 Questions

Exam 23: Cost Estimation and Cost Behaviour63 Questions

Exam 24: Quantitative Models for the Planning and Control of Stocks42 Questions

Exam 25: The Application of Linear Programming to Management Accounting30 Questions

Select questions type

Using more highly skilled direct labourers might affect which of the following variances?

(Multiple Choice)

4.7/5  (32)

(32)

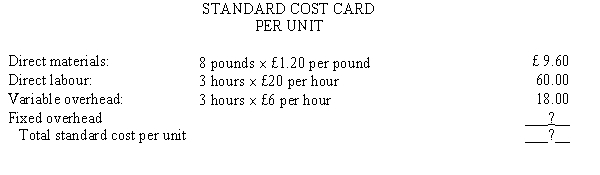

Figure 17-4

Shannon Ltd.'s standard cost card contained the following information:

Direct labour: 1.25 hours * £8.00 per hour = £10.00

Shannon planned to make 12,000 units. Shannon actually made 10,000 units using 13,000 hours.

-Refer to Figure 17-4. Shannon's labour efficiency variance was

(Multiple Choice)

4.8/5 (40)

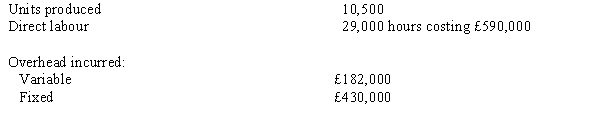

Figure 17-2

Rax Company has developed the following standards for one of its products:  The following activities occurred during the month of October:

The following activities occurred during the month of October:  The company records materials price variances at the time of purchase.

-Refer to Figure 17-2. Rax's variable standard cost per unit would be

The company records materials price variances at the time of purchase.

-Refer to Figure 17-2. Rax's variable standard cost per unit would be

(Multiple Choice)

4.9/5 (32)

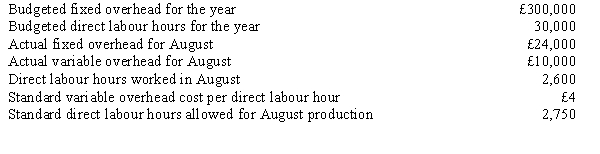

Figure 17-8

The following information was extracted from the accounting records of Noelle Company:  Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:

Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:  -Franklin Company expected sales were 2,000 units at £100 per unit. During 2011, it had actual sales of 1,800 units at £110 per unit. Budgeted variable costs were £60 per unit. What is Franklin's sales price variance?

-Franklin Company expected sales were 2,000 units at £100 per unit. During 2011, it had actual sales of 1,800 units at £110 per unit. Budgeted variable costs were £60 per unit. What is Franklin's sales price variance?

(Multiple Choice)

4.8/5 (36)

Figure 17-6  -Refer to Figure 17-6. The variable overhead spending variance would be

-Refer to Figure 17-6. The variable overhead spending variance would be

(Multiple Choice)

4.8/5 (36)

Figure 17-5

Ebola Company has developed the following standards for one of its products:  The following activities occurred during the month of October:

The following activities occurred during the month of October:  The company records materials price variances at the time of purchase.

-Refer to Figure 17-5. Ebola's labour efficiency variance would be

The company records materials price variances at the time of purchase.

-Refer to Figure 17-5. Ebola's labour efficiency variance would be

(Multiple Choice)

4.7/5 (42)

Figure 17-5

Ebola Company has developed the following standards for one of its products: The following activities occurred during the month of October: The company records materials price variances at the time of purchase.

-Refer to Figure 17-5. Ebola's materials price variance would be

(Multiple Choice)

4.9/5 (35)

Figure 17-7

Orient Company has developed the following standards for one of its products:  The following activities occurred during the month of November:

The following activities occurred during the month of November:  The company records materials price variances at the time of purchase.

-Refer to Figure 17-7. Orient's materials price variance would be

The company records materials price variances at the time of purchase.

-Refer to Figure 17-7. Orient's materials price variance would be

(Multiple Choice)

4.9/5 (39)

Figure 17-8

The following information was extracted from the accounting records of Noelle Company: Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:

-A sales volume variance will be favourable when:

(Multiple Choice)

4.8/5 (35)

Figure 17-8

The following information was extracted from the accounting records of Noelle Company: Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:

-Refer to Figure 17-8. Noelle's fixed overhead volume variance would be

(Multiple Choice)

4.8/5 (36)

Figure 17-7

Orient Company has developed the following standards for one of its products: The following activities occurred during the month of November: The company records materials price variances at the time of purchase.

-Refer to Figure 17-7. Orient's variable overhead efficiency variance would be

(Multiple Choice)

4.7/5 (35)

To determine the unit standard cost for a particular input, a company must decide how much

(Multiple Choice)

4.8/5 (33)

Fortensky Construction planned to produce 275,000 units using 34,375 machine hours. Actual output was 290,000 units using 37,425 machine hours. Fortensky's volume variance

(Multiple Choice)

4.8/5 (35)

During May, 6,000 pounds of raw materials were purchased at a cost of £2.60 per pound. If there was a favourable materials price variance of £900 for December, the standard cost per pound must be

(Multiple Choice)

4.9/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)