Exam 17: Standard Costing and Variance Analysis 1

Exam 1: Introduction to Management Accounting49 Questions

Exam 2: An Introduction to Cost Terms and Concepts64 Questions

Exam 3: Cost Assignment29 Questions

Exam 4: Accounting Entries for a Job Costing System15 Questions

Exam 5: Process Costing29 Questions

Exam 6: Joint and By-Product Costing61 Questions

Exam 7: Income Effects of Alternative Cost Accumulation Systems45 Questions

Exam 8: Cost-Volume-Profit Analysis60 Questions

Exam 9: Measuring Relevant Costs and Revenues for Decision-Making81 Questions

Exam 10: Activity-Based Costing40 Questions

Exam 11: Pricing Decisions and Profitability Analysis59 Questions

Exam 12: Decision-Making Under Conditions of Risk and Uncertainty29 Questions

Exam 13: Capital Investment Decisions: Appraisal Methods77 Questions

Exam 14: Capital Investment Decisions: the Impact of Capital Rationing, Taxation, Inflation and Risk25 Questions

Exam 15: The Budgeting Process86 Questions

Exam 16: Management Control Systems64 Questions

Exam 17: Standard Costing and Variance Analysis 181 Questions

Exam 18: Standard Costing and Variance Analysis 2: Further Aspects12 Questions

Exam 19: Divisional Financial Performance Measures51 Questions

Exam 20: Transfer Pricing in Divisionalized Companies50 Questions

Exam 21: Cost Management95 Questions

Exam 22: Strategic Management Accounting32 Questions

Exam 23: Cost Estimation and Cost Behaviour63 Questions

Exam 24: Quantitative Models for the Planning and Control of Stocks42 Questions

Exam 25: The Application of Linear Programming to Management Accounting30 Questions

Select questions type

Figure 17-3

Tuvok Ltd. has developed the following standards for one of its products:  -During October, 14,000 direct labour hours were worked at a standard cost of £40 per hour. If the labour rate variance for October was £70,000 favourable, the actual cost per labour hour must be

-During October, 14,000 direct labour hours were worked at a standard cost of £40 per hour. If the labour rate variance for October was £70,000 favourable, the actual cost per labour hour must be

(Multiple Choice)

4.8/5  (45)

(45)

Who is responsible for unfavourable labour efficiency variances caused by poor quality materials?

(Multiple Choice)

4.9/5 (43)

Figure 17-6  -Refer to Figure 17-6. The variable overhead efficiency variance would be

-Refer to Figure 17-6. The variable overhead efficiency variance would be

(Multiple Choice)

4.9/5 (38)

Figure 17-7

Orient Company has developed the following standards for one of its products:  The following activities occurred during the month of November:

The following activities occurred during the month of November:  The company records materials price variances at the time of purchase.

-Refer to Figure 17-7. Orient's labour efficiency variance would be

The company records materials price variances at the time of purchase.

-Refer to Figure 17-7. Orient's labour efficiency variance would be

(Multiple Choice)

4.8/5 (35)

Figure 17-2

Rax Company has developed the following standards for one of its products:  The following activities occurred during the month of October:

The following activities occurred during the month of October:  The company records materials price variances at the time of purchase.

-Refer to Figure 17-2. Rax's materials price variance would be

The company records materials price variances at the time of purchase.

-Refer to Figure 17-2. Rax's materials price variance would be

(Multiple Choice)

4.8/5 (37)

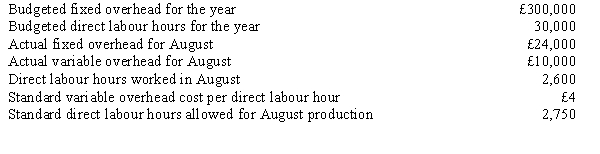

Figure 17-8

The following information was extracted from the accounting records of Noelle Company:  Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:

Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:  -Refer to Figure 17-8. Noelle's fixed overhead spending variance would be

-Refer to Figure 17-8. Noelle's fixed overhead spending variance would be

(Multiple Choice)

4.8/5 (42)

Which of the following is information that would be included in the standard cost card (sheet)?

(Multiple Choice)

4.7/5 (40)

Figure 17-8

The following information was extracted from the accounting records of Noelle Company: Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:

-Taylor Company's budgeted sales were 10,000 units at £200 per unit. Actual sales were 9,200 units at £210 per unit. Taylor's sales price variance is

(Multiple Choice)

5.0/5 (45)

For planning and control purposes, fixed overhead is NOT included in the standard cost per unit because:

(Multiple Choice)

4.8/5 (35)

Figure 17-2

Rax Company has developed the following standards for one of its products: The following activities occurred during the month of October: The company records materials price variances at the time of purchase.

-Refer to Figure 17-2. Rax's labour efficiency variance would be

(Multiple Choice)

4.8/5 (44)

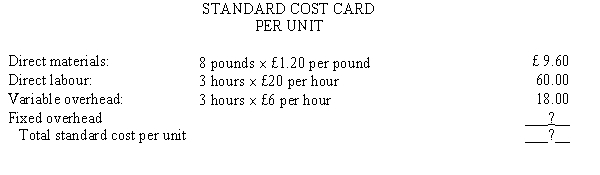

Figure 17-4

Shannon Ltd.'s standard cost card contained the following information:

Direct labour: 1.25 hours * £8.00 per hour = £10.00

Shannon planned to make 12,000 units. Shannon actually made 10,000 units using 13,000 hours.

-Refer to Figure 17-4. Shannon's standard hours allowed for production was

(Multiple Choice)

4.8/5 (34)

Figure 17-3

Tuvok Ltd. has developed the following standards for one of its products:

-Refer to Figure 17-3. Tuvok's materials usage variance is

(Multiple Choice)

4.8/5 (33)

Figure 17-7

Orient Company has developed the following standards for one of its products: The following activities occurred during the month of November: The company records materials price variances at the time of purchase.

-Refer to Figure 17-7. Orient's labour rate variance would be

(Multiple Choice)

4.9/5 (31)

If actual fixed overhead was £120,000 and there was a £2,600 favourable spending variance and a £2,000 unfavourable volume variance, budgeted fixed overhead must have been

(Multiple Choice)

4.7/5 (33)

If a company was concerned with controlling expenditures on overhead items, which variance would be useful?

(Multiple Choice)

4.9/5 (28)

Figure 17-2

Rax Company has developed the following standards for one of its products: The following activities occurred during the month of October: The company records materials price variances at the time of purchase.

-Refer to Figure 17-2. Rax's materials usage variance would be

(Multiple Choice)

4.8/5 (31)

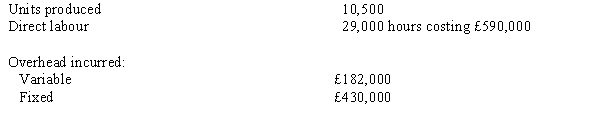

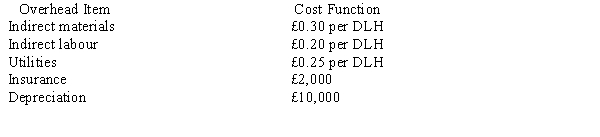

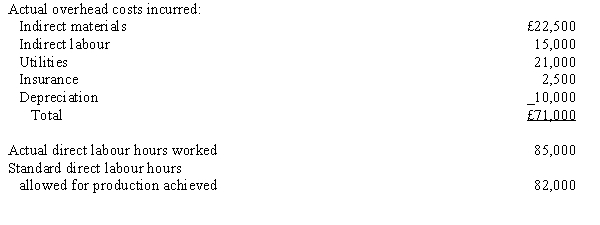

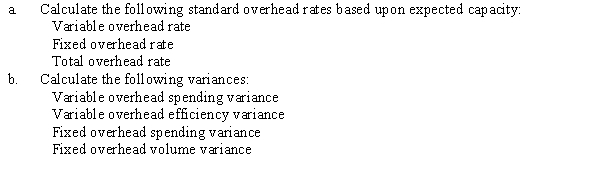

Mills Company uses standard costing for direct materials and direct labour. Management would like to use standard costing for variable and fixed overhead.

The following monthly cost functions were developed for overhead items:  The cost functions are considered reliable within a relevant range of 70,000 to 100,000 direct labour hours. The company expects to operate at 80,000 direct labour hours per month.

Information for the month of September is as follows:

The cost functions are considered reliable within a relevant range of 70,000 to 100,000 direct labour hours. The company expects to operate at 80,000 direct labour hours per month.

Information for the month of September is as follows:  Required:

Required:

(Essay)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)