Exam 33: Aggregate Demand and Aggregate Supply

Exam 1: Ten Principles of Economics220 Questions

Exam 2: Thinking Like an Economist284 Questions

Exam 3: Interdependence and the Gains From Trade192 Questions

Exam 4: The Market Forces of Supply and Demand277 Questions

Exam 5: Elasticity and Its Application222 Questions

Exam 6: Supply, Demand, and Government Policies321 Questions

Exam 7: Consumers, Producers, and the Efficiency of Markets218 Questions

Exam 8: Applications: The Costs of Taxation203 Questions

Exam 9: Application: International Trade214 Questions

Exam 10: Externalities204 Questions

Exam 11: Public Goods and Common Resources182 Questions

Exam 12: The Design of the Tax System225 Questions

Exam 13: The Costs of Production261 Questions

Exam 14: Firms in Competitive Markets243 Questions

Exam 15: Monopoly231 Questions

Exam 16: Monopolistic Competition246 Questions

Exam 17: Oligopoly204 Questions

Exam 18: The Markets for the Factors of Production232 Questions

Exam 19: Earnings and Discrimination230 Questions

Exam 20: Income Inequality and Poverty194 Questions

Exam 21: The Theory of Consumer Choice209 Questions

Exam 22: Frontiers in Microeconomics185 Questions

Exam 23: Measuring a Nations Income231 Questions

Exam 24: Measuring the Cost of Living214 Questions

Exam 25: Production and Growth187 Questions

Exam 26: Saving, Investment, and the Financial System225 Questions

Exam 27: Tools of Finance198 Questions

Exam 28: Unemployment and Its Natural Rate361 Questions

Exam 29: The Monetary System210 Questions

Exam 30: Money Growth and Inflation201 Questions

Exam 31: Open-Economy Macroeconomics: Basic Concepts194 Questions

Exam 32: A Macroeconomic Theory of the Open Economy188 Questions

Exam 33: Aggregate Demand and Aggregate Supply189 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand207 Questions

Exam 35: The Short-Run Tradeoff Between Inflation and Unemployment223 Questions

Exam 36: Six Debates Over Macroeconomic Policy154 Questions

Select questions type

Suppose a country offers a new investment tax credit. Which curve(s) in the aggregate demand and aggregate supply model would be affected, and which way would it (they) shift?

(Essay)

4.9/5  (29)

(29)

People had been expecting the price level to be 120 but it turns out to be 122. In response Robinson Tire Company increases the number of workers it employs. What could explain this?

(Multiple Choice)

4.9/5 (37)

Scenario 33-2

Imagine that in the current year the economy is in long-run equilibrium. Then stock prices rise more than expected and stay high for some time.

-Refer to Scenario 33-2. In the long run, the change in price expectations created by the rise in stock prices

(Multiple Choice)

4.9/5 (32)

Policymakers who control monetary and fiscal policy and want to offset the effects on output of an economic contraction caused by a shift in aggregate supply could use policy to shift

(Multiple Choice)

4.9/5 (39)

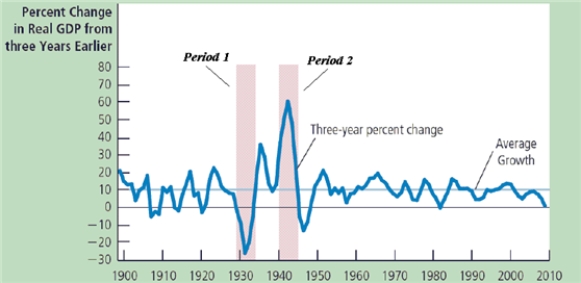

Figure 33-8

-Refer to Figure 33-8. Explain how the aggregate demand and aggregate supply model changed during periods 1 and 2.

-Refer to Figure 33-8. Explain how the aggregate demand and aggregate supply model changed during periods 1 and 2.

(Essay)

4.9/5 (29)

Use sticky-wage theory to explain why an increase in the expected price level shifts the aggregate supply curve.

(Essay)

4.7/5 (26)

If U.S. speculators gained greater confidence in foreign economies so that they wanted to move more of their wealth into foreign countries, the dollar would

(Multiple Choice)

4.9/5 (30)

Scenario 33-2

Imagine that in the current year the economy is in long-run equilibrium. Then stock prices rise more than expected and stay high for some time.

-Refer to Scenario 33-2. In the short run what happens to the price level and real GDP?

(Multiple Choice)

4.8/5 (42)

The aggregate-demand curve shows the quantity of domestic goods and services that households, firms, the government, and customers abroad want to buy at each price level.

(True/False)

4.9/5 (31)

According to the misperceptions theory of short-run aggregate supply, if a firm thought that inflation was going to be 5 percent and actual inflation was 6 percent, then the firm would believe that the relative price of what it produce had

(Multiple Choice)

4.9/5 (28)

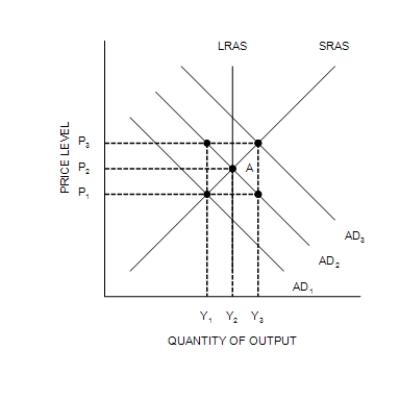

Figure 33-6

-Refer to Figure 33-6. Suppose the economy starts at A. If changes occur that move the economy to a new short-run equilibrium of P1 and Y1 , then it must be the case that

-Refer to Figure 33-6. Suppose the economy starts at A. If changes occur that move the economy to a new short-run equilibrium of P1 and Y1 , then it must be the case that

(Multiple Choice)

4.8/5 (39)

Name two macroeconomic variables that decline when an economy goes into recession, and name one macroeconomic variable that rises.

(Essay)

4.8/5 (35)

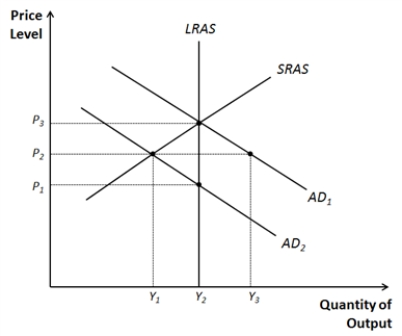

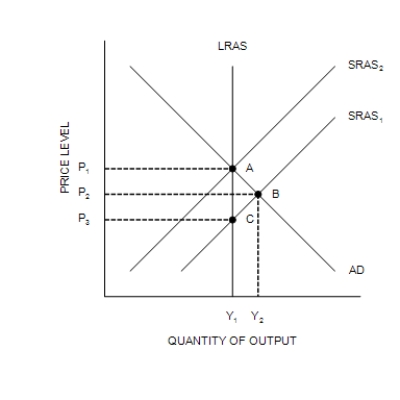

Figure 33-13

-Refer to Figure 33-13. Suppose the economy starts at P3 and Y2. Explain how government purchases would need to change to move the economy to P2 and Y1. What about taxes?

-Refer to Figure 33-13. Suppose the economy starts at P3 and Y2. Explain how government purchases would need to change to move the economy to P2 and Y1. What about taxes?

(Essay)

4.9/5 (36)

Suppose technology advances within a nation. Which curves in the aggregate demand and aggregate supply model would be affected, and which way would they shift?

(Essay)

4.7/5 (34)

Suppose the economy is in long-run equilibrium. If there is a sharp increase in the minimum wage as well as an increase in taxes, then in the short run, real GDP will

(Multiple Choice)

4.9/5 (29)

Figure 33-4  -Refer to Figure 33-4. The short-run equilibrium is defined by the given AD and SRAS curves. Which of the long-run aggregate-supply curves is consistent with the economy being in an expansion?

-Refer to Figure 33-4. The short-run equilibrium is defined by the given AD and SRAS curves. Which of the long-run aggregate-supply curves is consistent with the economy being in an expansion?

(Multiple Choice)

4.8/5 (34)

Classical economist David Hume observed that as the money supply expanded after gold discoveries it took some time for prices to rise and in the meantime the economy enjoyed higher employment and production. This is inconsistent with monetary neutrality because monetary neutrality would mean that

(Multiple Choice)

4.7/5 (32)

Policymakers who influence aggregate demand can potentially mitigate the severity of economic fluctuations.

(True/False)

4.7/5 (31)

Figure 33-3  -Refer to Figure 33-3. In Figure 33-3, Point B represents a

-Refer to Figure 33-3. In Figure 33-3, Point B represents a

(Multiple Choice)

4.9/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)