Exam 15: Estimation of Dynamic Causal Effects

The distributed lag model assumptions include all of the following with the exception of a. there is no perfect multicollinearity.

b. is strictly exogenous.

c. .

d. The random variables and have a stationary distribution.

B

In the distributed lag model, the coefficient on the contemporaneous value of the regressor is called the

D

It has been argued that Canada's aggregate output growth and unemployment rates are

very sensitive to United States economic fluctuations, while the opposite is not true.

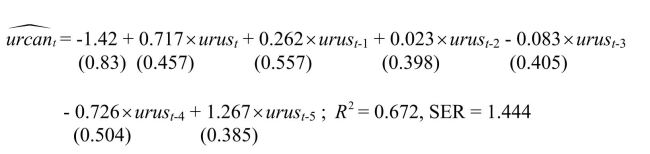

(a)A researcher uses a distributed lag model to estimate dynamic causal effects of U.S.

economic activity on Canada.The results (HAC standard errors in parenthesis)for the

sample period 1961:I-1995:IV are:  where urcan is the Canadian unemployment rate, and urus is the United States

unemployment rate.

Calculate the long-run cumulative dynamic multiplier.

where urcan is the Canadian unemployment rate, and urus is the United States

unemployment rate.

Calculate the long-run cumulative dynamic multiplier.

Autocorrelation in the error term is the result of omitted variables which are

serially correlated.Canadian unemployment rates depend on Canadian labor

market conditions and most likely on Canadian aggregate demand variables in

the short run.Prime candidates for slowly changing omitted variables would be

demographics, indicators of unemployment insurance generosity, changes in the

terms of trade, monetary policy indicators such as the real interest rate, etc.

Some of these variables are highly likely to be correlated with U.S.

unemployment rates since demographics are similar between the two countries

and Canadian monetary policy often follows moves made by the Federal

Reserve.A case could be made that the U.S.unemployment rate is exogenous

as a result of the relative size of the two economies.However, due to the size of

the trade between the two countries, this is not as easy to support as if the

dependent variable were the unemployment rate in Costa Rica, say.

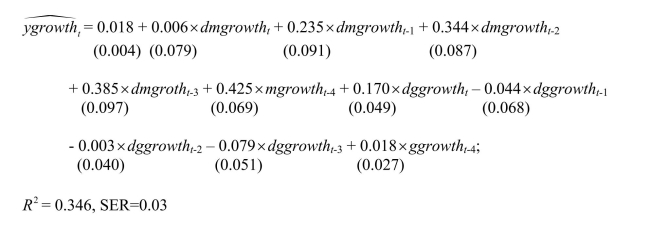

A model that attracted quite a bit of interest in macroeconomics in the 1970s was the St.

Louis model.The underlying idea was to calculate fiscal and monetary impact and long

run cumulative dynamic multipliers, by relating output (growth)to government

expenditure (growth)and money supply (growth).The assumption was that both

government expenditures and the money supply were exogenous.Estimation of a St.

Louis type model using quarterly data from 1960:I-1995:IV results in the following

output (HAC standard errors in parenthesis):  where ygrowth is quarterly growth of real GDP, mgrowth is quarterly growth of real money supply (M2), and ggrowth is quarterly growth of real government expenditures. "d" in front of ggrowth and mgrowth indicates a change in the variable. (a)Assuming that money and government expenditures are exogenous, what do the

coefficients represent? Calculate the h-period cumulative dynamic multipliers from these.

How can you test for the statistical significance of the cumulative dynamic multipliers

and the long-run cumulative dynamic multiplier?

where ygrowth is quarterly growth of real GDP, mgrowth is quarterly growth of real money supply (M2), and ggrowth is quarterly growth of real government expenditures. "d" in front of ggrowth and mgrowth indicates a change in the variable. (a)Assuming that money and government expenditures are exogenous, what do the

coefficients represent? Calculate the h-period cumulative dynamic multipliers from these.

How can you test for the statistical significance of the cumulative dynamic multipliers

and the long-run cumulative dynamic multiplier?

The impact effect is the a. zero period dynamic multiplier.

b. period dynamic multiplier, .

c. cumulative dynamic multiplier.

d. long-run cumulative dynamic multiplier.

Your textbook mentions heteroskedasticity- and autocorrelation- consistent standard

errors.Explain why you should use this option in your regression package when

estimating the distributed lag regression model.What are the properties of the OLS

estimator in the presence of heteroskedasticity and autocorrelation in the error terms?

Explain why it is likely to find autocorrelation in time series data.If the errors are

autocorrelated, then why not simply adjust for autocorrelation by using some non-linear

estimation method such as Cochrane-Orcutt?

To convey information about the dynamic multipliers more effectively, you should

A distributed lag regression a. is also called .

b. can also be used with cross-sectional data.

c. gives estimates of dynamic causal effects.

d. is sometimes referred to as ADL.

Heteroskedasticity- and autocorrelation-consistent standard errors

A seasonal binary (or indicator or dummy)variable, in the case of monthly data,

Your textbook presents as an example of a distributed lag regression the effect of the

weather on the price of orange juice.The authors mention U.S.income and Australian

exports, oil prices and inflation, monetary policy and inflation, and the Phillips curve as

other candidates for distributed lag regression.Briefly discuss whether or not the

exogeneity assumption is likely to hold in each of these cases.Explain why it is so hard

to come up with good examples of distributed lag regressions in economics.

In your intermediate macroeconomics course, government expenditures and the money

supply were treated as exogenous, in the sense that the variables could be changed to

conduct economic policy to influence target variables, but that these variables would not

react to changes in the economy as a result of some fixed rule.The St.Louis Model,

proposed by two researchers at the Federal Reserve in St.Louis, used this idea to test

whether monetary policy or fiscal policy was more effective in influencing output

behavior.Although there were various versions of this model, the basic specification was

of the following type: Assuming that money supply and government expenditures are exogenous, how would

you estimate dynamic causal effects? Why do you think this type of model is no longer

used by most to calculate fiscal and monetary multipliers?

One of the central predictions of neo-classical macroeconomic growth theory is that an

increase in the growth rate of the population causes at first a decline the growth rate of

real output per capita, but that subsequently the growth rate returns to its natural level,

itself determined by the rate of technological innovation.The intuition is that, if the

growth rate of the workforce increases, then more has to be saved to provide the new

workers with physical capital.However, accumulating capital takes time, so that output

per capita falls in the short run.

Under the assumption that population growth is exogenous, a number of regressions of

the growth rate of output per capita on current and lagged population growth were

performed, as reported below.(A constant was included in the regressions but is not

reported.HAC standard errors are in brackets.BIC is listed at the bottom of the table). Regression of Growth Rate of Real Per-Capita GDP on Lags of Population Growth, United States, 1825-2000.

Lag number Dynamic multipliers Dynamic multipliers Dynamic multipliers (1) Dynamic multipliers Dynamic multipliers 0 -0.9 -1.1 -1.3 -0.2 -2.0 (1.3) (1.3) (1.7) (1.7) (1.5) 1 3.5 3.2 1.8 0.8 - 2 (1.6) (1.6) (1.6) (1.5) - 3 -1.3 -3.0 -2.2 - - 4 (1.7) 1.6) (1.4) - - BIC -234.4 -236.1 -238.5 -240.0 -241.8 (a)Which of these models is favored by the information criterion?

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)