Exam 16: Time-Series Forecasting

Exam 1: Defining and Collecting Data202 Questions

Exam 2: Organizing and Visualizing256 Questions

Exam 3: Numerical Descriptive Measures217 Questions

Exam 4: Basic Probability167 Questions

Exam 5: Discrete Probability Distributions165 Questions

Exam 6: The Normal Distribution and Other Continuous Distributions170 Questions

Exam 7: Sampling Distributions165 Questions

Exam 8: Confidence Interval Estimation219 Questions

Exam 9: Fundamentals of Hypothesis Testing: One-Sample Tests194 Questions

Exam 10: Two-Sample Tests240 Questions

Exam 11: Analysis of Variance170 Questions

Exam 12: Chi-Square and Nonparametric188 Questions

Exam 13: Simple Linear Regression243 Questions

Exam 14: Introduction to Multiple394 Questions

Exam 15: Multiple Regression146 Questions

Exam 16: Time-Series Forecasting235 Questions

Exam 17: Getting Ready to Analyze Data386 Questions

Exam 18: Statistical Applications in Quality Management159 Questions

Exam 19: Decision Making126 Questions

Exam 20: Probability and Combinatorics421 Questions

Select questions type

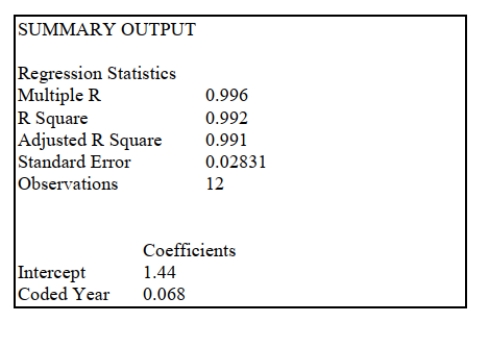

SCENARIO 16-7

The executive vice-president of a drug manufacturing firm believes that the demand for the firm's

most popular drug has been evidencing an exponential trend since 1999. She uses Microsoft

Excel to obtain the partial output below. The dependent variable is the log base 10 of the demand

for the drug, while the independent variable is years, where 1999 is coded as 0, 2000 is coded as

1, etc.  -Referring to Scenario 16-7, the fitted exponential trend equation to predict Y is __________.

-Referring to Scenario 16-7, the fitted exponential trend equation to predict Y is __________.

(Short Answer)

4.8/5  (40)

(40)

SCENARIO 16-15-B

You are the CEO of a diary company. The total milk production (in gallons) from your company

over the past 30 years are presented below and also contained in the Excel file SCENARIO 16-

15-B.XLSX. Year 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Milk 150201 193718 212520 214553 237507 248069 241824 234627 252049 252029 Prod 263449 260689 247900 260059 268197 249477 246216 265236 256364 241705 245932 243529 241551 247697 248454 241974 235823 243517 238490 248606 You want to predict your company's future total milk production using the linear trend, quadratic

trend, exponential trend, first-order autoregressive, second-order autoregressive and third-order

autoregressive model.

-Referring to Scenario 16-15-B, you can reject the null hypothesis for testing

the appropriateness of the first-order autoregressive model at the 5% level of significance.

(True/False)

4.9/5 (37)

SCENARIO 16-13

Given below is the monthly time series data for U.S. retail sales of building materials over a

specific year. Month Retail Sales 1 6,594 2 6,610 3 8,174 4 9,513 5 10,595 6 10,415 7 9,949 8 9,810 9 9,637 10 9,732 11 9,214 12 9,201 The results of the linear trend, quadratic trend, exponential trend, first-order autoregressive,

second-order autoregressive and third-order autoregressive model are presented below in which

the coded month for the 1st month is 0:

Coefficients Standard Error t Stat P-value Intercept 7950.7564 617.6342 12.8729 0.0000 Coded Month 212.6503 95.1145 2.2357 0.0494

Coefficients Standard Error t Stat P-value Intercept 3.8912 0.0315 123.3674 0.0000 Coded Month 0.0116 0.0049 2.3957 0.0376

Coefficients Standard Error t Stat P-value Intercept 3132.0951 1287.2899 2.4331 0.0378 YLag1 0.6823 0.1398 4.8812 0.0009

-Referring to Scenario 16-13, you can conclude that the quadratic term in the

quadratic-trend model is statistically significant at the 5% level of significance.

Coefficients Standard Error t Stat P-value Intercept 3.8912 0.0315 123.3674 0.0000 Coded Month 0.0116 0.0049 2.3957 0.0376

Coefficients Standard Error t Stat P-value Intercept 3132.0951 1287.2899 2.4331 0.0378 YLag1 0.6823 0.1398 4.8812 0.0009

-Referring to Scenario 16-13, you can conclude that the quadratic term in the

quadratic-trend model is statistically significant at the 5% level of significance.

(True/False)

4.7/5 (32)

SCENARIO 16-15-B

You are the CEO of a diary company. The total milk production (in gallons) from your company

over the past 30 years are presented below and also contained in the Excel file SCENARIO 16-

15-B.XLSX. Year 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Milk 150201 193718 212520 214553 237507 248069 241824 234627 252049 252029 Prod 263449 260689 247900 260059 268197 249477 246216 265236 256364 241705 245932 243529 241551 247697 248454 241974 235823 243517 238490 248606 You want to predict your company's future total milk production using the linear trend, quadratic

trend, exponential trend, first-order autoregressive, second-order autoregressive and third-order

autoregressive model.

-Referring to Scenario 16-15-B, what is the exponentially smoothed forecast for 2016 using

a smoothing coefficient of W = 0.5?

(Short Answer)

4.8/5 (34)

SCENARIO 16-12

A local store developed a multiplicative time-series model to forecast its revenues in future

quarters, using quarterly data on its revenues during the 5-year period from 2009 to 2013. The

following is the resulting regression equation:

where is the estimated number of contracts in a quarter

is the coded quarterly value with in the first quarter of 2008 .

is a dummy variable equal to 1 in the first quarter of a year and 0 otherwise.

is a dummy variable equal to 1 in the second quarter of a year and 0 otherwise.

is a dummy variable equal to 1 in the third quarter of a year and 0 otherwise.

-Referring to Scenario 16-12, using the regression equation, what is the forecast for the

revenues in the fourth quarter of 2015?

(Short Answer)

4.9/5 (35)

SCENARIO 16-15-A

You are the CEO of a diary company. The total milk production (in gallons) from your company

over the past 30 years are presented below and also contained in the Excel file SCENARIO 16-

15-A.XLSX. Year 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Milk 150201 172719 171357 157121 155727 152974 153443 158548 162614 164210 Prod 159127 153866 165992 177843 167477 163821 161700 170348 174105 185103 184670 173385 159695 173641 165706 171164 168706 150684 179314 163802 You want to predict your company's future total milk production using the linear trend, quadratic

trend, exponential trend, first-order autoregressive, second-order autoregressive and third-order

autoregressive model.

-Referring to Scenario 16-15-A, what is your forecast for 2016 using the first-order

autoregressive model?

(Short Answer)

4.9/5 (31)

SCENARIO 16-13

Given below is the monthly time series data for U.S. retail sales of building materials over a

specific year. Month Retail Sales 1 6,594 2 6,610 3 8,174 4 9,513 5 10,595 6 10,415 7 9,949 8 9,810 9 9,637 10 9,732 11 9,214 12 9,201 The results of the linear trend, quadratic trend, exponential trend, first-order autoregressive,

second-order autoregressive and third-order autoregressive model are presented below in which

the coded month for the 1st month is 0:

Coefficients Standard Error t Stat P-value Intercept 7950.7564 617.6342 12.8729 0.0000 Coded Month 212.6503 95.1145 2.2357 0.0494

Coefficients Standard Error t Stat P-value Intercept 3.8912 0.0315 123.3674 0.0000 Coded Month 0.0116 0.0049 2.3957 0.0376

Coefficients Standard Error t Stat P-value Intercept 3132.0951 1287.2899 2.4331 0.0378 YLag1 0.6823 0.1398 4.8812 0.0009

-Referring to Scenario 16-13, the best model based on the residual plots is the

quadratic-trend regression model.

(True/False)

4.8/5 (29)

SCENARIO 16-10

Business closures in a city in the western U.S. from 2007 to 2012 were: 2007 10 2008 11 2009 13 2010 19 2011 24 2012 35 Microsoft Excel was used to fit both first-order and second-order autoregressive models, resulting

in the following partial outputs: SUMMARY OUTPUT - Order Model Coefficients Intercept -5.77 X Variable 1 0.80 X Variable 2 1.14 SUMMARY OUTPUT - Order Model Coefficients Intercept -4.16 X Variable 1 1.59

-Referring to Scenario 16-10, the fitted values for the second-order autoregressive model are

________, ________, ________, and ________.

(Short Answer)

4.8/5 (35)

SCENARIO 16-13

Given below is the monthly time series data for U.S. retail sales of building materials over a

specific year. Month Retail Sales 1 6,594 2 6,610 3 8,174 4 9,513 5 10,595 6 10,415 7 9,949 8 9,810 9 9,637 10 9,732 11 9,214 12 9,201 The results of the linear trend, quadratic trend, exponential trend, first-order autoregressive,

second-order autoregressive and third-order autoregressive model are presented below in which

the coded month for the 1st month is 0:

Coefficients Standard Error t Stat P-value Intercept 7950.7564 617.6342 12.8729 0.0000 Coded Month 212.6503 95.1145 2.2357 0.0494

Coefficients Standard Error t Stat P-value Intercept 3.8912 0.0315 123.3674 0.0000 Coded Month 0.0116 0.0049 2.3957 0.0376

Coefficients Standard Error t Stat P-value Intercept 3132.0951 1287.2899 2.4331 0.0378 YLag1 0.6823 0.1398 4.8812 0.0009

-Referring to Scenario 16-13, what is your forecast for the month using the second-

order autoregressive model?

(Short Answer)

4.7/5 (33)

SCENARIO 16-15-A

You are the CEO of a diary company. The total milk production (in gallons) from your company

over the past 30 years are presented below and also contained in the Excel file SCENARIO 16-

15-A.XLSX. Year 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Milk 150201 172719 171357 157121 155727 152974 153443 158548 162614 164210 Prod 159127 153866 165992 177843 167477 163821 161700 170348 174105 185103 184670 173385 159695 173641 165706 171164 168706 150684 179314 163802 You want to predict your company's future total milk production using the linear trend, quadratic

trend, exponential trend, first-order autoregressive, second-order autoregressive and third-order

autoregressive model.

-Referring to Scenario 16-15-A, if a five-year moving average is used to smooth this series,

what would be the moving average for 1988?

(Short Answer)

4.8/5 (39)

SCENARIO 16-4

The number of cases of merlot wine sold by a Paso Robles winery in an 8-year period follows. Year Cases of Wine 2005 270 2006 356 2007 398 2008 456 2009 358 2010 500 2011 410 2012 376

-Referring to Scenario 16-4, a centered 3-year moving average is to be constructed for the

wine sales. The moving average for 2006 is __________.

(Short Answer)

4.9/5 (42)

SCENARIO 16-13

Given below is the monthly time series data for U.S. retail sales of building materials over a

specific year. Month Retail Sales 1 6,594 2 6,610 3 8,174 4 9,513 5 10,595 6 10,415 7 9,949 8 9,810 9 9,637 10 9,732 11 9,214 12 9,201 The results of the linear trend, quadratic trend, exponential trend, first-order autoregressive,

second-order autoregressive and third-order autoregressive model are presented below in which

the coded month for the 1st month is 0:

Coefficients Standard Error t Stat P-value Intercept 7950.7564 617.6342 12.8729 0.0000 Coded Month 212.6503 95.1145 2.2357 0.0494

Coefficients Standard Error t Stat P-value Intercept 3.8912 0.0315 123.3674 0.0000 Coded Month 0.0116 0.0049 2.3957 0.0376

Coefficients Standard Error t Stat P-value Intercept 3132.0951 1287.2899 2.4331 0.0378 YLag1 0.6823 0.1398 4.8812 0.0009

-Referring to Scenario 16-13, the best model based on the residual plots is the

second-order autoregressive model.

(True/False)

4.7/5 (38)

SCENARIO 16-13

Given below is the monthly time series data for U.S. retail sales of building materials over a

specific year. Month Retail Sales 1 6,594 2 6,610 3 8,174 4 9,513 5 10,595 6 10,415 7 9,949 8 9,810 9 9,637 10 9,732 11 9,214 12 9,201 The results of the linear trend, quadratic trend, exponential trend, first-order autoregressive,

second-order autoregressive and third-order autoregressive model are presented below in which

the coded month for the 1st month is 0:

Coefficients Standard Error t Stat P-value Intercept 7950.7564 617.6342 12.8729 0.0000 Coded Month 212.6503 95.1145 2.2357 0.0494

Coefficients Standard Error t Stat P-value Intercept 3.8912 0.0315 123.3674 0.0000 Coded Month 0.0116 0.0049 2.3957 0.0376

Coefficients Standard Error t Stat P-value Intercept 3132.0951 1287.2899 2.4331 0.0378 YLag1 0.6823 0.1398 4.8812 0.0009

-Referring to Scenario 16-13, what is the exponentially smoothed value for the second

month using a smoothing coefficient of W = 0.5?

(Short Answer)

5.0/5 (38)

SCENARIO 16-15-B

You are the CEO of a diary company. The total milk production (in gallons) from your company

over the past 30 years are presented below and also contained in the Excel file SCENARIO 16-

15-B.XLSX. Year 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Milk 150201 193718 212520 214553 237507 248069 241824 234627 252049 252029 Prod 263449 260689 247900 260059 268197 249477 246216 265236 256364 241705 245932 243529 241551 247697 248454 241974 235823 243517 238490 248606 You want to predict your company's future total milk production using the linear trend, quadratic

trend, exponential trend, first-order autoregressive, second-order autoregressive and third-order

autoregressive model.

-Referring to Scenario 16-15-B, what is your forecast for 2016 using the linear-trend model?

(Short Answer)

4.7/5 (33)

SCENARIO 16-12

A local store developed a multiplicative time-series model to forecast its revenues in future

quarters, using quarterly data on its revenues during the 5-year period from 2009 to 2013. The

following is the resulting regression equation:

where is the estimated number of contracts in a quarter

is the coded quarterly value with in the first quarter of 2008 .

is a dummy variable equal to 1 in the first quarter of a year and 0 otherwise.

is a dummy variable equal to 1 in the second quarter of a year and 0 otherwise.

is a dummy variable equal to 1 in the third quarter of a year and 0 otherwise.

-Referring to Scenario 16-12, the estimated quarterly compound growth rate in revenues is around:

(Multiple Choice)

4.9/5 (38)

SCENARIO 16-13

Given below is the monthly time series data for U.S. retail sales of building materials over a

specific year. Month Retail Sales 1 6,594 2 6,610 3 8,174 4 9,513 5 10,595 6 10,415 7 9,949 8 9,810 9 9,637 10 9,732 11 9,214 12 9,201 The results of the linear trend, quadratic trend, exponential trend, first-order autoregressive,

second-order autoregressive and third-order autoregressive model are presented below in which

the coded month for the 1st month is 0:

Coefficients Standard Error t Stat P-value Intercept 7950.7564 617.6342 12.8729 0.0000 Coded Month 212.6503 95.1145 2.2357 0.0494

Coefficients Standard Error t Stat P-value Intercept 3.8912 0.0315 123.3674 0.0000 Coded Month 0.0116 0.0049 2.3957 0.0376

Coefficients Standard Error t Stat P-value Intercept 3132.0951 1287.2899 2.4331 0.0378 YLag1 0.6823 0.1398 4.8812 0.0009

-Referring to Scenario 16-13, what is the exponentially smoothed forecast for the month

using a smoothing coefficient of W = 0.25 if the exponentially smooth value for the and month are 9,477.7776 and 9,411.8332, respectively?

(Short Answer)

4.9/5 (37)

SCENARIO 16-5

The number of passengers arriving at San Francisco on the Amtrak cross-country express on 6

successive Mondays were: 60, 72, 96, 84, 36, and 48.

-Referring to Scenario 16-5, the number of arrivals will be exponentially smoothed with a

smoothing constant of 0.1. The smoothed value for the second Monday will be __________.

(Short Answer)

4.8/5 (39)

SCENARIO 16-14

A contractor developed a multiplicative time-series model to forecast the number of contracts in

future quarters, using quarterly data on number of contracts during the 3-year period from 2011 to

-The following is the resulting regression equation:

where is the estimated number of contracts in a quarter

is the coded quarterly value with in the first quarter of 2011 .

is a dummy variable equal to 1 in the first quarter of a year and 0 otherwise.

is a dummy variable equal to 1 in the second quarter of a year and 0 otherwise.

is a dummy variable equal to 1 in the third quarter of a year and 0 otherwise.

(Short Answer)

4.9/5 (37)

SCENARIO 16-14

A contractor developed a multiplicative time-series model to forecast the number of contracts in

future quarters, using quarterly data on number of contracts during the 3-year period from 2011 to

-Referring to Scenario 16-14, in testing the coefficient of X in the regression equation (0.117) the results were a t-statistic of 9.08 and an associated p-value of 0.0000. Which of the

Following is the best interpretation of this result?

(Multiple Choice)

4.9/5 (43)

SCENARIO 16-15-A

You are the CEO of a diary company. The total milk production (in gallons) from your company

over the past 30 years are presented below and also contained in the Excel file SCENARIO 16-

15-A.XLSX. Year 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Milk 150201 172719 171357 157121 155727 152974 153443 158548 162614 164210 Prod 159127 153866 165992 177843 167477 163821 161700 170348 174105 185103 184670 173385 159695 173641 165706 171164 168706 150684 179314 163802 You want to predict your company's future total milk production using the linear trend, quadratic

trend, exponential trend, first-order autoregressive, second-order autoregressive and third-order

autoregressive model.

-Referring to Scenario 16-15-A, you can conclude that the third-order

autoregressive model is appropriate at the 5% level of significance.

(True/False)

4.8/5 (27)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)