Exam 11: Cash Flow Estimation and Risk Analysis

Exam 1: An Overview of Financial Management and the Financial Environment38 Questions

Exam 2: Financial Statements, Cash Flow, and Taxes3 Questions

Exam 3: Analysis of Financial Statements104 Questions

Exam 4: Time Value of Money139 Questions

Exam 5: Bonds, Bond Valuation, and Interest Rates100 Questions

Exam 6: Risks and Rates of Return132 Questions

Exam 7: Stocks and Their Valuation48 Questions

Exam 8: Financial Options and Applications in Corporate Finance22 Questions

Exam 9: The Cost of Capital87 Questions

Exam 10: The Basics of Capital Budgeting98 Questions

Exam 11: Cash Flow Estimation and Risk Analysis66 Questions

Exam 12: Financial Planning and Forecasting Financial Statements46 Questions

Exam 13: Corporate Valuation, Value-Based Management, and Corporate Governance24 Questions

Exam 14: Distributions to Shareholders: Dividends and Repurchases26 Questions

Exam 15: Capital Structure Decisions70 Questions

Exam 16: Working Capital Management129 Questions

Exam 17: Multinational Financial Management39 Questions

Exam 18: Lease Financing20 Questions

Exam 19: Hybrid Financing: Preferred Stock, Warrants, and Convertibles27 Questions

Exam 20: Initial Public Offerings, Investment Banking, and Financial Restructuring22 Questions

Exam 21: Mergers, Lbos, Divestitures, and Holding Companies41 Questions

Exam 22: Bankruptcy, Reorganization, and Liquidation8 Questions

Exam 23: Derivatives and Risk Management14 Questions

Exam 24: Portfolio Theory, Asset Pricing Models, and Behavioral Finance25 Questions

Exam 25: Real Options15 Questions

Exam 26: Analysis of Capital Structure Theory27 Questions

Exam 27: Providing and Obtaining Credit31 Questions

Exam 28: Advanced Issues in Cash Management and Inventory Control20 Questions

Exam 29: Pension Plan Management9 Questions

Exam 30: Financial Management in Not-For-Profit Businesses10 Questions

Select questions type

Thomson Media is considering some new equipment whose data are shown below. The equipment has a 3-year tax life and would be fully depreciated by the straight-line method over 3 years, but it would have a positive pre-tax salvage value at the end of Year 3, when the project would be closed down. Also, some new working capital would be required, but it would be recovered at the end of the project's life. Revenues and other operating costs are expected to be constant over the project's 3-year life. What is the project's NPV?

(Multiple Choice)

4.9/5  (32)

(32)

Your company, CSUS Inc., is considering a new project whose data are Shown below. The required equipment has a 3-year tax life, and the accelerated rates for such property are 33%, 45%, 15%, and 7% for Years

1 through 4. Revenues and other operating costs are expected to be constant over the project's 10-year expected operating life. What is the project's Year 4 cash flow?

(Multiple Choice)

4.8/5 (20)

A firm that bases its capital budgeting decisions on either NPV or IRR will be more likely to accept a given project if it uses accelerated depreciation than if it uses straight-line depreciation, other things being equal.

(True/False)

4.9/5 (38)

Estimating project cash flows is generally the most important, but also the most difficult, step in the capital budgeting process. Methodology, such as the use of NPV versus IRR, is important, but less so than obtaining a reasonably accurate estimate of projects' cash flows.

(True/False)

4.9/5 (27)

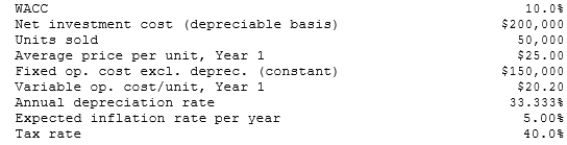

Poulsen Industries is analyzing an average-risk project, and the following data have been developed. Unit sales will be constant, but the sales price should increase with inflation. Fixed costs will also be constant, but variable costs should rise with inflation. The project should last for 3 years, it will be depreciated on a straight- line basis, and there will be no salvage value. This is just one of many projects for the firm, so any losses can be used to offset gains on other firm projects. The marketing manager does not think it is necessary to adjust for inflation since both the sales price and the variable costs will rise at the same rate, but the CFO thinks an adjustment is required. What is the difference in the expected NPV if the inflation adjustment is made vs. if it is not made?

(Multiple Choice)

4.8/5 (28)

The change in net working capital associated with new projects is always positive, because new projects mean that more working capital will be required. This situation is especially true for replacement projects.

(True/False)

4.7/5 (27)

Opportunity costs include those cash inflows that could be generated from assets the firm already owns if those assets are not used for the project being evaluated.

(True/False)

4.7/5 (37)

We can identify the cash costs and cash inflows to a company that will result from a project. These could be called "direct inflows and outflows," and the net difference is the direct net cash flow. If there are other costs and benefits that do not flow from or to the firm, but to other parties, these are called externalities, and they need not be considered as a part of the capital budgeting analysis.

(True/False)

4.8/5 (43)

Which one of the following would NOT result in incremental cash flows and thus should NOT be included in the capital budgeting analysis for a new product?

(Multiple Choice)

4.9/5 (43)

The primary advantage to using accelerated rather than straight-line depreciation is that with accelerated depreciation the present value of the tax savings provided by depreciation will be higher, other things held constant.

(True/False)

4.9/5 (33)

Sensitivity analysis measures a project's stand-alone risk by showing how much the project's NPV (or IRR) is affected by a small change in one of the input variables, say sales. Other things held constant, with the size of the independent variable graphed on the horizontal axis and the NPV on the vertical axis, the steeper the graph of the relationship line, the more risky the project, other things held constant.

(True/False)

4.9/5 (32)

If an investment project would make use of land which the firm currently owns, the project should be charged with the opportunity cost of the land.

(True/False)

4.8/5 (48)

Because of improvements in forecasting techniques, estimating the cash flows associated with a project has become the easiest step in the capital budgeting process.

(True/False)

4.8/5 (40)

If debt is to be used to finance a project, then when cash flows for a project are estimated, interest payments should be included in the analysis.

(True/False)

4.9/5 (36)

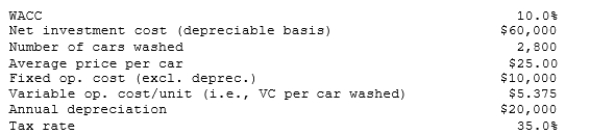

Your company, RMU Inc., is considering a new project whose data are shown below. What is the project's Year 1 cash flow?

(Multiple Choice)

4.8/5 (33)

Currently, Powell Products has a beta of 1.0, and its sales and profits are positively correlated with the overall economy. The company estimates that a proposed new project would have a higher standard deviation and coefficient of variation than an average company project. Also, the new project's sales would be countercyclical in the sense that they would be high when the overall economy is down and low when the overall economy is strong. On the basis of this information, which of the following statements is CORRECT?

(Multiple Choice)

4.8/5 (36)

The primary advantage to using accelerated rather than straight-line depreciation is that with accelerated depreciation the total amount of depreciation that can be taken, assuming the asset is used for its full tax life, is greater.

(True/False)

5.0/5 (25)

TexMex Food Company is considering a new salsa whose data are shown below. The equipment to be used would be depreciated by the straight- line method over its 3-year life and would have a zero salvage value, and no new working capital would be required. Revenues and other operating costs are expected to be constant over the project's 3-year life. However, this project would compete with other TexMex products and would reduce their pre-tax annual cash flows. What is the project's NPV? (Hint: Cash flows are constant in Years 1-3.)

(Multiple Choice)

4.7/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)