Exam 13: Differential Analysis: the Key to Decision Making

Exam 1: Managerial Accounting and Cost Concepts346 Questions

Exam 2: Job-Order Costing: Calculating Unit Product Costs408 Questions

Exam 3: Job-Order Costing: Cost Flows and External Reporting314 Questions

Exam 4: Process Costing365 Questions

Exam 5: Cost-Volume-Profit Relationships396 Questions

Exam 6: Variable Costing and Segment Reporting: Tools for Management392 Questions

Exam 7: Activity-Based Costing: a Tool to Aid Decision Making382 Questions

Exam 8: Master Budgeting284 Questions

Exam 9: Flexible Budgets and Performance Analysis491 Questions

Exam 10: Standard Costs and Variances469 Questions

Exam 11: Responsibility Accounting Systems335 Questions

Exam 12: Strategic Performance Measurement153 Questions

Exam 13: Differential Analysis: the Key to Decision Making432 Questions

Exam 14: Capital Budgeting Decisions405 Questions

Exam 15: Statement of Cash Flows221 Questions

Exam 16: Financial Statement Analysis327 Questions

Select questions type

The constraint at Dreyfus Incorporated is an expensive milling machine. The three products listed below use this constrained resource.

Required:a. Rank the products in order of their current profitability from the most profitable to the least profitable. In other words, rank the products in the order in which they should be emphasized.b. Assume that sufficient constraint time is available to satisfy demand for all but the least profitable product. Up to how much should the company be willing to pay to acquire more of the constrained resource?

Required:a. Rank the products in order of their current profitability from the most profitable to the least profitable. In other words, rank the products in the order in which they should be emphasized.b. Assume that sufficient constraint time is available to satisfy demand for all but the least profitable product. Up to how much should the company be willing to pay to acquire more of the constrained resource?

(Essay)

4.9/5  (39)

(39)

The Carter Corporation makes products A and B in a joint process from a single input, R. During a typical production run, 50,000 units of R yield 20,000 units of A and 30,000 units of B at the split-off point. Joint production costs total $90,000 per production run. The unit selling price for A is $4.00 and for B is $3.80 at the split-off point. However, B can be processed further at a total cost of $60,000 and then sold for $7.00 per unit.In a decision between selling B at the split-off point or processing B further, which of the following items is not relevant:

(Multiple Choice)

4.9/5 (43)

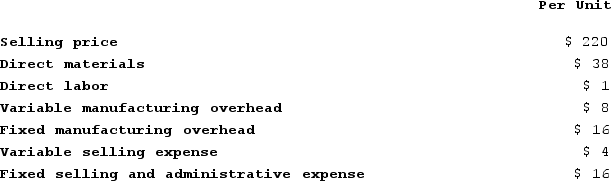

Younes Incorporated manufactures industrial components. One of its products, which is used in the construction of industrial air conditioners, is known as P06. Data concerning this product are given below:  The above per unit data are based on annual production of 4,000 units of the component. Assume that direct labor is a variable cost.The company has received a special, one-time-only order for 400 units of component P06. There would be no variable selling expense on this special order and the total fixed manufacturing overhead and fixed selling and administrative expenses of the company would not be affected by the order. Assuming that Younes has excess capacity and can fill the order without cutting back on the production of any product, what is the minimum price per unit below which the company should not accept the special order?

The above per unit data are based on annual production of 4,000 units of the component. Assume that direct labor is a variable cost.The company has received a special, one-time-only order for 400 units of component P06. There would be no variable selling expense on this special order and the total fixed manufacturing overhead and fixed selling and administrative expenses of the company would not be affected by the order. Assuming that Younes has excess capacity and can fill the order without cutting back on the production of any product, what is the minimum price per unit below which the company should not accept the special order?

(Multiple Choice)

4.9/5 (34)

Two alternatives, code-named X and Y, are under consideration at Guyer Corporation. Costs associated with the alternatives are listed below.  What is the financial advantage (disadvantage) of Alternative Y over Alternative X?

What is the financial advantage (disadvantage) of Alternative Y over Alternative X?

(Multiple Choice)

4.8/5 (29)

Morice Industries Incorporated has developed a new injection mold, model IA-05, that is designed to offer superior performance to a comparable injection mold sold by Morice's main competitor. The competing injection mold sells for $54,000 and needs to be replaced after 1,000 hours of use. It also requires $7,000 of preventive maintenance during its useful life. Model IA-05's performance capabilities are similar to the competing product with two important exceptions-it needs to be replaced only after 2,000 hours of use and it requires $8,000 of preventive maintenance during its useful life.From a value-based pricing standpoint what range of possible prices should Morice consider when setting a price for model IA-05?

(Multiple Choice)

4.8/5 (36)

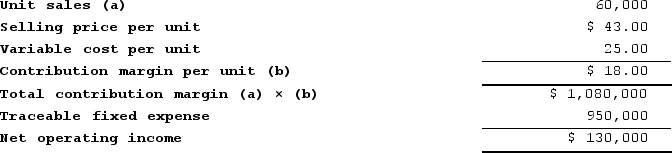

Buzby Corporation manufactures numerous products, one of which is called Epsilon39. The company has provided the following data about this product:

Required:a. Management is considering decreasing the price of Epsilon39 by 5%, from $43.00 to $40.85. The company's marketing managers estimate that this price reduction would increase unit sales by 10%, from 60,000 units to 66,000 units. Assuming that the total traceable fixed expense does not change, what net operating income will Epsilon39 earn at a price of $40.85 if this sales forecast is correct?b. Assuming that the total traceable fixed expense does not change, how many units of Epsilon39 would Buzby need to sell at a price of $40.85 to earn the same net operating income that it currently earns at a price of $43.00? (Round your answer up to the nearest whole number.)

Required:a. Management is considering decreasing the price of Epsilon39 by 5%, from $43.00 to $40.85. The company's marketing managers estimate that this price reduction would increase unit sales by 10%, from 60,000 units to 66,000 units. Assuming that the total traceable fixed expense does not change, what net operating income will Epsilon39 earn at a price of $40.85 if this sales forecast is correct?b. Assuming that the total traceable fixed expense does not change, how many units of Epsilon39 would Buzby need to sell at a price of $40.85 to earn the same net operating income that it currently earns at a price of $43.00? (Round your answer up to the nearest whole number.)

(Essay)

4.9/5 (34)

Boney Corporation processes sugar beets that it purchases from farmers. Sugar beets are processed in batches. A batch of sugar beets costs $53 to buy from farmers and $18 to crush in the company's plant. Two intermediate products, beet fiber and beet juice, emerge from the crushing process. The beet fiber can be sold as is for $25 or processed further for $18 to make the end product industrial fiber that is sold for $39. The beet juice can be sold as is for $32 or processed further for $28 to make the end product refined sugar that is sold for $79.What is the financial advantage (disadvantage) for the company from processing the intermediate product beet juice into refined sugar rather than selling it as is?

(Multiple Choice)

4.8/5 (37)

Wenner Corporation would like to use target costing for a new product it is considering introducing. At a selling price of $44 per unit, management projects sales of 10,000 units. The new product would require an investment of $900,000. The desired return on investment is 10%.The desired profit according to the target costing calculations is:

(Multiple Choice)

4.8/5 (35)

Tavis Robotics Corporation has developed a new robot-model FI-73-that has been designed to outperform a competitor's best-selling robot. The competitor's product has a useful life of 10,000 hours of service, has operating costs that average $4.60 per hour, and sells for $109,000. In contrast, model FI-73 has a useful life of 30,000 hours of service and its operating cost is $2.60 per hour. Tavis has not yet established a selling price for model FI-73.From a value-based pricing standpoint what is the differentiation value offered by FI-73 relative to the competitor's offering for each 30,000 hours of service?

(Multiple Choice)

4.8/5 (36)

Cabebe Corporation manufactures numerous products, one of which is called Omicron55. The company has provided the following data about this product:

Required:

a. Management is considering decreasing the price of Omicron55 by 4%, from $54.00 to $51.84. The company's marketing managers estimate that this price reduction would increase unit sales by 10%, from 140,000 units to 154,000 units. Assuming that the total traceable fixed expense does not change, what net operating income will Omicron55 earn at a price of $51.84 if this sales forecast is correct?

b. Assuming that the total traceable fixed expense does not change, if Cabebe decreases the price of Omicron55 to $51.84, what percentage change in unit sales would provide the same net operating income that it currently earns at a price of $54.00? (Round your answer to the nearest one-tenth of a percent.)

Required:

a. Management is considering decreasing the price of Omicron55 by 4%, from $54.00 to $51.84. The company's marketing managers estimate that this price reduction would increase unit sales by 10%, from 140,000 units to 154,000 units. Assuming that the total traceable fixed expense does not change, what net operating income will Omicron55 earn at a price of $51.84 if this sales forecast is correct?

b. Assuming that the total traceable fixed expense does not change, if Cabebe decreases the price of Omicron55 to $51.84, what percentage change in unit sales would provide the same net operating income that it currently earns at a price of $54.00? (Round your answer to the nearest one-tenth of a percent.)

(Essay)

4.8/5 (30)

Saulsberry Corporation manufactures numerous products, one of which is called Beta70. The company has provided the following data about this product:

Required:a. What net operating income is the company earning now on its sales of Beta70?

b. Management is considering increasing the price of Beta70 by 10%, from $60.00 to $66.00. The company's marketing managers estimate that this price hike would decrease unit sales by 15%, from 90,000 units to 76,500 units. Assuming that the total traceable fixed expense does not change, what net operating income will Beta70 earn at a price of $66.00 if this sales forecast is correct?

c. Assuming that the total traceable fixed expense does not change, how many units of Beta70 would Saulsberry need to sell at a price of $66.00 to earn the same net operating income that it currently earns at a price of $60.00? (Round your answer up to the nearest whole number.)

Required:a. What net operating income is the company earning now on its sales of Beta70?

b. Management is considering increasing the price of Beta70 by 10%, from $60.00 to $66.00. The company's marketing managers estimate that this price hike would decrease unit sales by 15%, from 90,000 units to 76,500 units. Assuming that the total traceable fixed expense does not change, what net operating income will Beta70 earn at a price of $66.00 if this sales forecast is correct?

c. Assuming that the total traceable fixed expense does not change, how many units of Beta70 would Saulsberry need to sell at a price of $66.00 to earn the same net operating income that it currently earns at a price of $60.00? (Round your answer up to the nearest whole number.)

(Essay)

4.9/5 (29)

Melbourne Corporation has traditionally made a subcomponent of its major product. Annual production of 30,000 subcomponents results in the following costs:  Melbourne has received an offer from an outside supplier who is willing to provide the 30,000 units of the subcomponent each year at a price of $28 per unit. Melbourne knows that the facilities now being used to manufacture the subcomponent could be rented to another company for $80,000 per year if the subcomponent were purchased from the outside supplier. There would be no effect of this decision on the total fixed manufacturing overhead of the company. Assume that direct labor is a variable cost.If Melbourne decides to purchase the subcomponent from the outside supplier, the annual financial advantage (disadvantage) would be:

Melbourne has received an offer from an outside supplier who is willing to provide the 30,000 units of the subcomponent each year at a price of $28 per unit. Melbourne knows that the facilities now being used to manufacture the subcomponent could be rented to another company for $80,000 per year if the subcomponent were purchased from the outside supplier. There would be no effect of this decision on the total fixed manufacturing overhead of the company. Assume that direct labor is a variable cost.If Melbourne decides to purchase the subcomponent from the outside supplier, the annual financial advantage (disadvantage) would be:

(Multiple Choice)

4.9/5 (32)

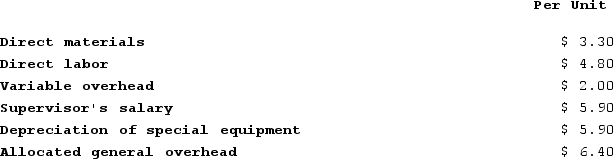

Mcfarlain Corporation is presently making part U98 that is used in one of its products. A total of 14,000 units of this part are produced and used every year. The company's Accounting Department reports the following costs of producing the part at this level of activity:  An outside supplier has offered to produce and sell the part to the company for $26.70 each. If this offer is accepted, the supervisor's salary and all of the variable costs, including direct labor, can be avoided. The special equipment used to make the part was purchased many years ago and has no salvage value or other use. The allocated general overhead represents fixed costs of the entire company, none of which would be avoided if the part were purchased instead of produced internally.In addition to the facts given above, assume that the space used to produce part U98 could be used to make more of one of the company's other products, generating an additional segment margin of $44,200 per year for that product. What would be the financial advantage (disadvantage) of buying part U98 from the outside supplier and using the freed space to make more of the other product?

An outside supplier has offered to produce and sell the part to the company for $26.70 each. If this offer is accepted, the supervisor's salary and all of the variable costs, including direct labor, can be avoided. The special equipment used to make the part was purchased many years ago and has no salvage value or other use. The allocated general overhead represents fixed costs of the entire company, none of which would be avoided if the part were purchased instead of produced internally.In addition to the facts given above, assume that the space used to produce part U98 could be used to make more of one of the company's other products, generating an additional segment margin of $44,200 per year for that product. What would be the financial advantage (disadvantage) of buying part U98 from the outside supplier and using the freed space to make more of the other product?

(Multiple Choice)

4.8/5 (39)

The SP Corporation makes 40,000 motors to be used in the production of its sewing machines. The average cost per motor at this level of activity is:  An outside supplier recently began producing a comparable motor that could be used in the sewing machine. The price offered to SP Corporation for this motor is $18. If SP Corporation decides not to make the motors, there would be no other use for the production facilities and none of the fixed manufacturing overhead cost could be avoided. Direct labor is a variable cost in this company. The annual financial advantage (disadvantage) for the company as a result of making the motors rather than buying them from the outside supplier would be:

An outside supplier recently began producing a comparable motor that could be used in the sewing machine. The price offered to SP Corporation for this motor is $18. If SP Corporation decides not to make the motors, there would be no other use for the production facilities and none of the fixed manufacturing overhead cost could be avoided. Direct labor is a variable cost in this company. The annual financial advantage (disadvantage) for the company as a result of making the motors rather than buying them from the outside supplier would be:

(Multiple Choice)

4.7/5 (40)

It is profitable to continue processing joint products after the split-off point if their total revenues exceed the joint costs.

(True/False)

4.8/5 (28)

Banfield Corporation makes three products that use compound W, the current constrained resource. Data concerning those products appear below:  Rank the products in order of their current profitability from most profitable to least profitable. In other words, rank the products in the order in which they should be emphasized. (Round your intermediate calculations to 2 decimal places.)

Rank the products in order of their current profitability from most profitable to least profitable. In other words, rank the products in the order in which they should be emphasized. (Round your intermediate calculations to 2 decimal places.)

(Multiple Choice)

4.8/5 (36)

. A cost that will be incurred regardless of which alternative is selected is not relevant when choosing between the alternatives.

(True/False)

4.8/5 (34)

Wenner Corporation would like to use target costing for a new product it is considering introducing. At a selling price of $44 per unit, management projects sales of 10,000 units. The new product would require an investment of $900,000. The desired return on investment is 10%.The target cost per unit is closest to:

(Multiple Choice)

5.0/5 (27)

Lusk Corporation produces and sells 16,100 units of Product X each month. The selling price of Product X is $31 per unit, and variable expenses are $25 per unit. A study has been made concerning whether Product X should be discontinued. The study shows that $71,000 of the $111,000 in monthly fixed expenses charged to Product X would not be avoidable even if the product was discontinued. If Product X is discontinued, the monthly financial advantage (disadvantage) for the company of eliminating this product should be:

(Multiple Choice)

4.8/5 (39)

Blauvelt Electronics Corporation has developed a new instrument-model GZ-29-that has been designed to outperform a competitor's best-selling instrument. Model GZ-29 has a useful life of 30,000 hours of service and its operating cost is $3.20 per hour.In contrast, the competitor's product has a useful life of 10,000 hours of service and has operating costs that average $5.60 per hour. The competitor's instrument sells for $149,000. Blauvelt has not yet established a selling price for model GZ-29.From a value-based pricing standpoint what is the differentiation value offered by GZ-29 relative to the competitor's offering for each 30,000 hours of service?

(Multiple Choice)

4.9/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)