Exam 6: Efficient Diversification

Exam 1: Investments: Background and Issues79 Questions

Exam 2: Asset Classes and Financial Instruments85 Questions

Exam 3: Securities Markets94 Questions

Exam 4: Mutual Funds and Other Investment Companies90 Questions

Exam 5: Risk, Return, and the Historical Record89 Questions

Exam 6: Efficient Diversification89 Questions

Exam 7: Capital Asset Pricing and Arbitrage Pricing Theory89 Questions

Exam 8: The Efficient Market Hypothesis92 Questions

Exam 9: Behavioral Finance and Technical Analysis89 Questions

Exam 10: Bond Prices and Yields96 Questions

Exam 11: Managing Bond Portfolios90 Questions

Exam 12: Macroeconomic and Industry Analysis93 Questions

Exam 13: Equity Valuation94 Questions

Exam 14: Financial Statement Analysis88 Questions

Exam 15: Options Markets91 Questions

Exam 16: Option Valuation90 Questions

Exam 17: Futures Markets and Risk Management92 Questions

Exam 18: Evaluating Investment Performance78 Questions

Exam 19: International Diversification50 Questions

Exam 20: Hedge Funds65 Questions

Exam 21: Taxes, Inflation, and Investment Strategy74 Questions

Exam 22: Investors and the Investment Process86 Questions

Select questions type

The expected rate of return of a portfolio of risky securities is ________.

(Multiple Choice)

4.7/5  (39)

(39)

What is the standard deviation of a portfolio of two stocks given the following data: Stock A has a standard deviation of 30%. Stock B has a standard deviation of 18%. The portfolio contains 60% of stock A, and the correlation coefficient between the two stocks is -1.

(Multiple Choice)

4.9/5 (34)

Stock A has a beta of 1.2, and stock B has a beta of 1. The returns of stock A are ________ sensitive to changes in the market than are the returns of stock B.

(Multiple Choice)

4.8/5 (24)

The ________ reward-to-variability ratio is found on the ________ capital market line.

(Multiple Choice)

4.9/5 (30)

An investor can design a risky portfolio based on two stocks, A and B. Stock A has an expected return of 18% and a standard deviation of return of 20%. Stock B has an expected return of 14% and a standard deviation of return of 5%. The correlation coefficient between the returns of A and B is .50. The risk-free rate of return is 10%. The standard deviation of return on the optimal risky portfolio is ________.

(Multiple Choice)

4.9/5 (43)

What is the most likely correlation coefficient between a stock-index mutual fund and the S&P 500?

(Multiple Choice)

4.8/5 (38)

An investor can design a risky portfolio based on two stocks, A and B. The standard deviation of return on stock A is 20%, while the standard deviation on stock B is 15%. The correlation coefficient between the returns on A and B is 0%. The rate of return for stocks A and B is 20% and 10% respectively. The expected return on the minimum-variance portfolio is approximately ________.

(Multiple Choice)

4.9/5 (33)

A stock has a correlation with the market of .45. The standard deviation of the market is 21%, and the standard deviation of the stock is 35%. What is the stock's beta?

(Multiple Choice)

4.9/5 (40)

Decreasing the number of stocks in a portfolio from 50 to 10 would likely ________.

(Multiple Choice)

4.9/5 (32)

Which of the following is a correct expression concerning the formula for the standard deviation of returns of a two-asset portfolio where the correlation coefficient is positive?

(Multiple Choice)

4.8/5 (26)

Some diversification benefits can be achieved by combining securities in a portfolio as long as the correlation between the securities is ________.

(Multiple Choice)

4.8/5 (24)

The values of beta coefficients of securities are ________.

(Multiple Choice)

4.8/5 (35)

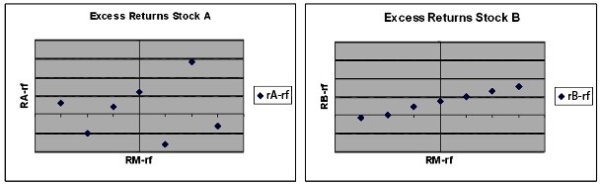

The figures below show plots of monthly excess returns for two stocks plotted against excess returns for a market index.  Which stock is likely to further reduce risk for an investor currently holding her portfolio in a well-diversified portfolio of common stock?

Which stock is likely to further reduce risk for an investor currently holding her portfolio in a well-diversified portfolio of common stock?

(Multiple Choice)

4.8/5 (35)

An investor can design a risky portfolio based on two stocks, A and B. The standard deviation of return on stock A is 20%, while the standard deviation on stock B is 15%. The correlation coefficient between the returns on A and B is 0%. The rate of return for stocks A and B is 20% and 10% respectively. The standard deviation of return on the minimum-variance portfolio is ________.

(Multiple Choice)

4.9/5 (31)

According to Tobin's separation property, portfolio choice can be separated into two independent tasks consisting of ________ and ________.

(Multiple Choice)

4.8/5 (32)

The standard deviation of return on investment A is 10%, while the standard deviation of return on investment B is 5%. If the covariance of returns on A and B is .0030, the correlation coefficient between the returns on A and B is ________.

(Multiple Choice)

4.9/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)