Exam 6: Efficient Diversification

Exam 1: Investments: Background and Issues79 Questions

Exam 2: Asset Classes and Financial Instruments85 Questions

Exam 3: Securities Markets94 Questions

Exam 4: Mutual Funds and Other Investment Companies90 Questions

Exam 5: Risk, Return, and the Historical Record89 Questions

Exam 6: Efficient Diversification89 Questions

Exam 7: Capital Asset Pricing and Arbitrage Pricing Theory89 Questions

Exam 8: The Efficient Market Hypothesis92 Questions

Exam 9: Behavioral Finance and Technical Analysis89 Questions

Exam 10: Bond Prices and Yields96 Questions

Exam 11: Managing Bond Portfolios90 Questions

Exam 12: Macroeconomic and Industry Analysis93 Questions

Exam 13: Equity Valuation94 Questions

Exam 14: Financial Statement Analysis88 Questions

Exam 15: Options Markets91 Questions

Exam 16: Option Valuation90 Questions

Exam 17: Futures Markets and Risk Management92 Questions

Exam 18: Evaluating Investment Performance78 Questions

Exam 19: International Diversification50 Questions

Exam 20: Hedge Funds65 Questions

Exam 21: Taxes, Inflation, and Investment Strategy74 Questions

Exam 22: Investors and the Investment Process86 Questions

Select questions type

Which of the following provides the best example of a systematic-risk event?

(Multiple Choice)

4.9/5  (38)

(38)

A portfolio of stocks fluctuates when the Treasury yields change. Since this risk cannot be eliminated through diversification, it is called ________.

(Multiple Choice)

5.0/5 (34)

The expected return of a portfolio is 8.9%, and the risk-free rate is 3.5%. If the portfolio standard deviation is 12%, what is the reward-to-variability ratio of the portfolio?

(Multiple Choice)

4.9/5 (34)

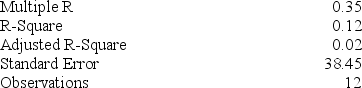

You run a regression for a stock's return on a market index and find the following Excel output:

________ % of the variance is explained by this regression.

________ % of the variance is explained by this regression.

(Multiple Choice)

4.8/5 (36)

A project has a 50% chance of doubling your investment in 1 year and a 50% chance of losing half your money. What is the expected return on this investment project?

(Multiple Choice)

4.8/5 (35)

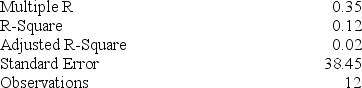

You run a regression for a stock's return on a market index and find the following Excel output:

The stock is ________ riskier than the typical stock.

The stock is ________ riskier than the typical stock.

(Multiple Choice)

5.0/5 (36)

The part of a stock's return that is systematic is a function of which of the following variables?

I. Volatility in excess returns of the stock market

II. The sensitivity of the stock's returns to changes in the stock market

III. The variance in the stock's returns that is unrelated to the overall stock market

(Multiple Choice)

4.8/5 (40)

Based on the outcomes in the following table, choose which of the statements below is (are) correct?

I. The covariance of security A and security B is zero.

II. The correlation coefficient between securities A and C is negative.

III. The correlation coefficient between securities B and C is positive.

I. The covariance of security A and security B is zero.

II. The correlation coefficient between securities A and C is negative.

III. The correlation coefficient between securities B and C is positive.

(Multiple Choice)

4.9/5 (27)

Investing in two assets with a correlation coefficient of 1 will reduce which kind of risk?

(Multiple Choice)

4.8/5 (34)

To construct a riskless portfolio using two risky stocks, one would need to find two stocks with a correlation coefficient of ________.

(Multiple Choice)

4.9/5 (29)

The portfolio with the lowest standard deviation for any risk premium is called the_______.

(Multiple Choice)

4.8/5 (43)

Approximately how many securities does it take to diversify almost all of the unique risk from a portfolio?

(Multiple Choice)

4.8/5 (34)

The optimal risky portfolio can be identified by finding:

I. The minimum-variance point on the efficient frontier

II. The maximum-return point on the efficient frontier and the minimum-variance point on the efficient frontier

III. The tangency point of the capital market line and the efficient frontier

IV. The line with the steepest slope that connects the risk-free rate to the efficient frontier

(Multiple Choice)

4.7/5 (36)

An investor can design a risky portfolio based on two stocks, A and B. Stock A has an expected return of 21% and a standard deviation of return of 39%. Stock B has an expected return of 14% and a standard deviation of return of 20%. The correlation coefficient between the returns of A and B is .4. The risk-free rate of return is 5%. The standard deviation of returns on the optimal risky portfolio is ________.

(Multiple Choice)

4.9/5 (28)

Which of the following correlation coefficients will produce the most diversification benefits?

(Multiple Choice)

4.8/5 (35)

You find that the annual Sharpe ratio for stock A returns is equal to 1.8. For a 3-year holding period, the Sharpe ratio would equal ________.

(Multiple Choice)

4.9/5 (23)

If an investor does not diversify his portfolio and instead puts all of his money in one stock, the appropriate measure of security risk for that investor is the ________.

(Multiple Choice)

4.8/5 (38)

Suppose that a stock portfolio and a bond portfolio have a zero correlation. This means that ________.

(Multiple Choice)

4.9/5 (33)

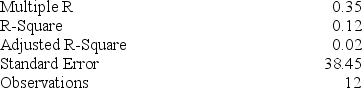

You run a regression for a stock's return on a market index and find the following Excel output:

The characteristic line for this stock is Rstock = ________ + ________ Rmarket.

The characteristic line for this stock is Rstock = ________ + ________ Rmarket.

(Multiple Choice)

4.7/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)