Exam 6: Efficient Diversification

Exam 1: Investments: Background and Issues79 Questions

Exam 2: Asset Classes and Financial Instruments85 Questions

Exam 3: Securities Markets94 Questions

Exam 4: Mutual Funds and Other Investment Companies90 Questions

Exam 5: Risk, Return, and the Historical Record89 Questions

Exam 6: Efficient Diversification89 Questions

Exam 7: Capital Asset Pricing and Arbitrage Pricing Theory89 Questions

Exam 8: The Efficient Market Hypothesis92 Questions

Exam 9: Behavioral Finance and Technical Analysis89 Questions

Exam 10: Bond Prices and Yields96 Questions

Exam 11: Managing Bond Portfolios90 Questions

Exam 12: Macroeconomic and Industry Analysis93 Questions

Exam 13: Equity Valuation94 Questions

Exam 14: Financial Statement Analysis88 Questions

Exam 15: Options Markets91 Questions

Exam 16: Option Valuation90 Questions

Exam 17: Futures Markets and Risk Management92 Questions

Exam 18: Evaluating Investment Performance78 Questions

Exam 19: International Diversification50 Questions

Exam 20: Hedge Funds65 Questions

Exam 21: Taxes, Inflation, and Investment Strategy74 Questions

Exam 22: Investors and the Investment Process86 Questions

Select questions type

A portfolio is composed of two stocks, A and B. Stock A has a standard deviation of return of 24%, while stock B has a standard deviation of return of 18%. Stock A comprises 60% of the portfolio, while stock B comprises 40% of the portfolio. If the variance of return on the portfolio is .0380, the correlation coefficient between the returns on A and B is ________.

(Multiple Choice)

4.9/5  (25)

(25)

Asset A has an expected return of 20% and a standard deviation of 25%. The risk-free rate is 10%. What is the reward-to-variability ratio?

(Multiple Choice)

4.8/5 (26)

An investor can design a risky portfolio based on two stocks, A and B. The standard deviation of return on stock A is 24%, while the standard deviation on stock B is 14%. The correlation coefficient between the returns on A and B is .35. The expected return on stock A is 25%, while on stock B it is 11%. The proportion of the minimum-variance portfolio that would be invested in stock B is approximately ________.

(Multiple Choice)

4.8/5 (38)

Which one of the following stock return statistics fluctuates the most over time?

(Multiple Choice)

4.9/5 (41)

Harry Markowitz is best known for his Nobel Prize-winning work on ________.

(Multiple Choice)

4.7/5 (32)

Which risk can be partially or fully diversified away as additional securities are added to a portfolio?

I. Total risk

II. Systematic risk

III. Firm-specific risk

(Multiple Choice)

4.8/5 (31)

A security's beta coefficient will be negative if ________.

(Multiple Choice)

4.8/5 (35)

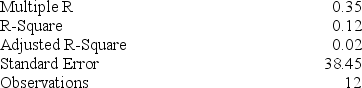

You run a regression for a stock's return on a market index and find the following Excel output:

This stock has greater systematic risk than a stock with a beta of ________.

This stock has greater systematic risk than a stock with a beta of ________.

(Multiple Choice)

4.9/5 (37)

Many current and retired Enron Corp. employees had their 401k retirement accounts wiped out when Enron collapsed because ________.

(Multiple Choice)

4.9/5 (35)

The plot of a security's excess return relative to the market's excess return is called the ________.

(Multiple Choice)

4.8/5 (34)

An investor can design a risky portfolio based on two stocks, A and B. Stock A has an expected return of 18% and a standard deviation of return of 20%. Stock B has an expected return of 14% and a standard deviation of return of 5%. The correlation coefficient between the returns of A and B is .50. The risk-free rate of return is 10%. The expected return on the optimal risky portfolio is ________.

(Multiple Choice)

4.8/5 (34)

If you want to know the portfolio standard deviation for a three-stock portfolio, you will have to ________.

(Multiple Choice)

4.9/5 (34)

You are constructing a scatter plot of excess returns for stock A versus the market index. If the correlation coefficient between stock A and the index is -1, you will find that the points of the scatter diagram ________ and the line of best fit has a ________.

(Multiple Choice)

4.7/5 (40)

Which of the following correlation coefficients will produce the least diversification benefit?

(Multiple Choice)

4.8/5 (33)

You put half of your money in a stock portfolio that has an expected return of 14% and a standard deviation of 24%. You put the rest of your money in a risky bond portfolio that has an expected return of 6% and a standard deviation of 12%. The stock and bond portfolios have a correlation of .55. The standard deviation of the resulting portfolio will be ________.

(Multiple Choice)

4.9/5 (35)

You are recalculating the risk of ACE stock in relation to the market index, and you find that the ratio of the systematic variance to the total variance has risen. You must also find that the ________.

(Multiple Choice)

4.8/5 (31)

As you lengthen the time horizon of your investment period and decide to invest for multiple years, you will find that:

I. The average risk per year may be smaller over longer investment horizons.

II. The overall risk of your investment will compound over time.

III. Your overall risk on the investment will fall.

(Multiple Choice)

4.9/5 (37)

The ________ is the covariance divided by the product of the standard deviations of the returns on each fund.

(Multiple Choice)

4.7/5 (50)

What is the standard deviation of a portfolio of two stocks given the following data: Stock A has a standard deviation of 18%. Stock B has a standard deviation of 14%. The portfolio contains 40% of stock A, and the correlation coefficient between the two stocks is -.23.

(Multiple Choice)

4.7/5 (25)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)