Exam 6: Consolidated Financial Statements: on Date of Business Combination

Exam 1: Ethical Issues in Advanced Accounting33 Questions

Exam 2: Partnerships: Organization and Operation39 Questions

Exam 3: Partnership Liquidation and Incorporation; Joint Ventures40 Questions

Exam 4: Accounting for Branches; Combined Financial Statements39 Questions

Exam 5: Business Combinations25 Questions

Exam 6: Consolidated Financial Statements: on Date of Business Combination39 Questions

Exam 7: Consolidated Financial Statements: Subsequent to Date of Business Combination39 Questions

Exam 8: Consolidated Financial Statements: Intercompany Transactions49 Questions

Exam 9: Consolidated Financial Statements: Income Taxes, Cash Flows, and Installment Acquisitions31 Questions

Exam 10: Consolidated Financial Statements: Special Problems29 Questions

Exam 11: International Accounting Standards; Accounting for Foreign Currency Transactions24 Questions

Exam 12: Translation of Foreign Currency Financial Statements20 Questions

Exam 13: Components; Interim Reports; Reporting for the Sec40 Questions

Exam 14: Bankruptcy: Liquidation and Reorganization30 Questions

Exam 15: Estates and Trusts39 Questions

Exam 16: Nonprofit Organizations35 Questions

Exam 17: Governmental Entities: General Fund34 Questions

Exam 18: Governmental Entities: Other Governmental Funds and Account Groups31 Questions

Exam 19: Governmental Entities: Proprietary Funds, Fiduciary Funds, and Comprehensive Annual Financial Report29 Questions

Select questions type

Before the computation of goodwill, the debits in the date-of-business-combination working paper elimination for the consolidated balance sheet of Promo Corporation and its 80%-owned subsidiary subtotaled $640,000, compared with a $540,000 credit to Investment in Sindow Company Common Stock-Promo. The working paper elimination should be completed with:

(Multiple Choice)

4.9/5  (40)

(40)

In a business combination resulting in a parent company-subsidiary relationship, the parent company's Investment in Subsidiary Common Stock ledger account balance is:

(Multiple Choice)

4.9/5 (40)

Minority interest in net assets of subsidiary is displayed in the consolidated balance sheet as:

(Multiple Choice)

4.7/5 (41)

On April 30, 2006, Press Corporation paid $168,000 cash for 80% of the outstanding common stock of Sow Company. Legal, accounting, and finder's fees paid by Press relative to the business combination totaled $24,000. The current fair value of Sow's identifiable net assets was $220,000 on April 30, 2006; the carrying amount was $200,000.

Prepare a working paper to compute the minority interest and goodwill in the April 30, 2006 consolidated balance sheet of Press Corporation and subsidiary under each of the following independent assumptions:

a. Sow's identifiable net assets are recognized at current fair value; minority interest is based on current fair value of identifiable net assets.

b. Sow's identifiable net assets are recognized at current fair value only to the extent of Press Corporation's interest; balance of net assets and minority interest are reflected at carrying amounts in Sow's accounting records.

c. Current fair value, through inference, is assigned to total net assets of Sow, including goodwill.

(Essay)

4.7/5 (28)

A debit to Goodwill-Subsidiary in a working paper elimination (in journal entry format) for a parent company and its wholly owned subsidiary indicates that the current fair values of the subsidiary's identifiable net assets exceeded their carrying amounts on the date of the business combination.

(True/False)

4.8/5 (41)

A controlling financial interest traditionally has been defined as the investor corporation's ownership of more than 50% of the investee corporation's outstanding common stock.

(True/False)

5.0/5 (36)

Because minority stockholders exercise no ownership control over the operations of either the parent company or the subsidiary, minority stockholders in substance might be considered a special class of creditors of the consolidated entity.

(True/False)

4.8/5 (47)

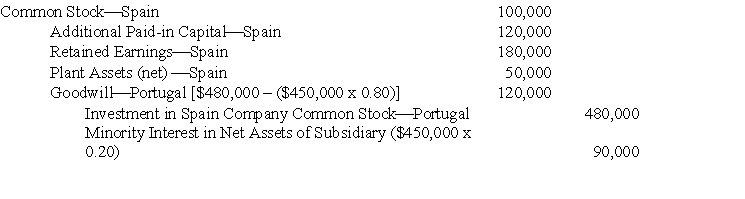

On October 31, 2006, Portugal Corporation acquired 80% of the outstanding common stock of Spain Company in a business combination. Total cost of the investment, including direct out-of-pocket costs, was $480,000. The working paper elimination (in journal entry format, explanation omitted) for Portugal Corporation and Subsidiary on October 31, 2006, was as follows:  If goodwill had been computed based on the implied current fair value of the subsidiary's total net assets, the debit to Goodwill-Portugal in the foregoing working paper elimination would have been:

If goodwill had been computed based on the implied current fair value of the subsidiary's total net assets, the debit to Goodwill-Portugal in the foregoing working paper elimination would have been:

(Multiple Choice)

4.8/5 (39)

On the date of a business combination resulting in a parent-subsidiary relationship, the differences between current fair values and carrying amounts of the subsidiary's identifiable net assets are:

(Multiple Choice)

4.9/5 (31)

Consolidated financial statements are prepared when a parent-subsidiary relationship exists, in recognition of the accounting principle or concept of:

(Multiple Choice)

4.8/5 (35)

In a proposed Statement, "Consolidated Financial Statements: Purpose and Policy," the FASB would replace objectively determined legal form by subjectively determined economic substance as a basis for consolidated financial statements. Majority ownership of an investee's outstanding common stock would no longer be a prerequisite for consolidation.

a. Present arguments in support of the FASB's proposal.

b. Present arguments in opposition to the FASB's proposal.

(Essay)

5.0/5 (39)

How is the minority interest in net assets of subsidiary displayed in a consolidated balance sheet under the economic unit concept of consolidated financial statements?

(Multiple Choice)

4.7/5 (39)

On December 31, 2006, the balance sheet of Sint Company included stockholders' equity of $2,000,000. On that date, Plane Corporation acquired for cash a controlling interest in the common stock of Sint. The December 31, 2006, current fair values of Sint's identifiable net assets totaled $2,400,000, and goodwill computed as the difference between Plane's cost and its share of the current fair value of Sint's identifiable net assets was $180,000.

Prepare a working paper to compute the total cost of Plane's investment in Sint if Plane owns:

a. 100% of Sint's common stock

b. 90% of Sint's common stock

c. 80% of Sint's common stock

(Essay)

4.8/5 (45)

On November 30, 2006, Pegler Corporation paid $500,000 cash and issued 100,000 shares of $1 par common stock with a current fair value of $10 a share for all 50,000 outstanding shares of $5 par common stock (carrying amount $20 a share) of Stadler Company, which became a subsidiary of Pegler. Also on November 30, 2006, Pegler paid $50,000 for finder's, accounting, and legal fees related to the business combination and $80,000 for costs associated with the SEC registration statement for the common stock issued in the combination. The net result of Pegler's journal entries to record the combination is to:

(Multiple Choice)

4.8/5 (39)

Finance-related subsidiaries may be excluded from consolidation at the election of the parent company's management.

(True/False)

4.8/5 (39)

On March 1, 2006, Pride Corporation paid $400,000 for all the outstanding common stock of Supra Company in a business combination, for which out-of-pocket costs may be disregarded. The carrying amounts of Supra's identifiable assets and liabilities on March 1, 2006, follow:  On March 1, 2006, the inventories of Supra had a current fair value of $95,000, and the plant assets (net) had a current fair value of $280,000.

The amount recognized as goodwill as a result of the business combination is:

On March 1, 2006, the inventories of Supra had a current fair value of $95,000, and the plant assets (net) had a current fair value of $280,000.

The amount recognized as goodwill as a result of the business combination is:

(Multiple Choice)

4.8/5 (34)

All out-of-pocket costs of a business combination reduce additional paid-in capital of the combinor.

(True/False)

4.7/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)