Exam 10: Credit Risk: Individual Loans

Exam 1: Why Are Financial Institutions Special90 Questions

Exam 2: Deposit-Taking Institutions43 Questions

Exam 3: Finance Companies71 Questions

Exam 4: Securities, Brokerage, and Investment Banking91 Questions

Exam 5: Mutual Funds, Hedge Funds, and Pension Funds61 Questions

Exam 6: Insurance Companies80 Questions

Exam 7: Risks of Financial Institutions110 Questions

Exam 8: Interest Rate Risk I110 Questions

Exam 9: Interest Rate Risk II116 Questions

Exam 10: Credit Risk: Individual Loans112 Questions

Exam 11: Credit Risk: Loan Portfolio and Concentration Risk51 Questions

Exam 12: Liquidity Risk85 Questions

Exam 13: Foreign Exchange Risk87 Questions

Exam 14: Sovereign Risk89 Questions

Exam 15: Market Risk95 Questions

Exam 16: Off-Balance-Sheet Risk101 Questions

Exam 17: Technology and Other Operational Risks107 Questions

Exam 18: Liability and Liquidity Management38 Questions

Exam 19: Deposit Insurance and Other Liability Guarantees54 Questions

Exam 20: Capital Adequacy102 Questions

Exam 21: Product and Geographic Expansion114 Questions

Exam 22: Futures and Forwards234 Questions

Exam 23: Options, Caps, Floors, and Collars113 Questions

Exam 24: Swaps95 Questions

Exam 25: Loan Sales83 Questions

Exam 26: Securitization Index98 Questions

Select questions type

Suppose that debt-equity ratio (D/E) and the sales-asset ratio (S/A) were two factors influencing the past default behavior of borrowers. Based on past default (repayment) experience, the linear probability model is estimated as: PDi = 0.5(D/Ei) + 0.1(S/Ai). If a prospective borrower has a debt-equity ratio of 0.4 and sales-asset ratio of 1.8, the expected probability of default is

(Multiple Choice)

4.8/5  (37)

(37)

The amount of leverage of a borrower and the probability of default are positively related, but only after some minimum level of debt.

(True/False)

4.8/5 (39)

Commercial loans have been decreasing in importance in bank loan portfolios.

(True/False)

4.8/5 (40)

A loan commitment is an agreement involving the amount of loan available and the amount of time during which the loan can be initiated.

(True/False)

4.8/5 (32)

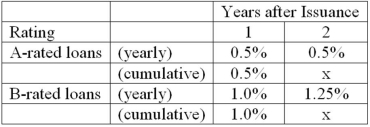

The following information on the mortality rate of loans as estimated by an FI:  What is the cumulative mortality rate of the A-rated and B-rated loans for year 2?

What is the cumulative mortality rate of the A-rated and B-rated loans for year 2?

(Multiple Choice)

4.9/5 (34)

Which of the following factors may affect the promised return an FI receives on a loan?

(Multiple Choice)

5.0/5 (40)

Use the following information and the option valuation model for the next two problems. Onyx Corporation has a $200,000 loan that will mature in one year. The risk free interest rate is 6 percent. The standard deviation in the rate of change in the underlying asset's value is 12 percent, and the leverage ratio for Onyx is 0.8 (80 percent). The value for N(h1) is 0.02743, and the value for N(h2) is 0.96406. What is the current market value of the loan?

(Multiple Choice)

4.8/5 (32)

Using a modified discriminant function similar to Altman's, Burger Bank estimates the following coefficients for its portfolio of loans: Z = 1.4X1 + 1.09X2 + 1.5X3

Where X1 = debt to asset ratio; X2 = net income and X3 = dividend payout ratio.

Using Z = 1.682 as the cut-off rate, what should be the debt to asset ratio of the firm in order for the bank to approve the loan?

(Multiple Choice)

4.8/5 (42)

Which of the following refers to the term "mortality rate"?

(Multiple Choice)

4.8/5 (29)

Willingness to post collateral may be a signal of more rather than less credit risk on the part of the borrower.

(True/False)

4.9/5 (32)

Suppose that the financial ratios of a potential borrowing firm took the following values: X1 = 0.30

X2 = 0

X3 = -0.30

X4 = 0.15

X5 = 2.1

Altman's discriminant function takes the form:

Z = 1.2 X1 + 1.4 X2 + 3.3 X3 + 0.6 X4 + 1.0 X5

The Z score for the firm would be

(Multiple Choice)

4.9/5 (37)

Residential mortgages are the smallest component of bank real estate loan portfolios.

(True/False)

4.8/5 (27)

The cumulative default probability of a borrower in a given time period is one minus the product of the marginal default probabilities for all time periods up to that time period.

(True/False)

4.9/5 (31)

Use the following information and the option valuation model for the next two problems. Onyx Corporation has a $200,000 loan that will mature in one year. The risk free interest rate is 6 percent. The standard deviation in the rate of change in the underlying asset's value is 12 percent, and the leverage ratio for Onyx is 0.8 (80 percent). The value for N(h1) is 0.02743, and the value for N(h2) is 0.96406. What is the required yield on this risky loan?

(Multiple Choice)

4.8/5 (32)

In making credit decisions, which of the following items is considered a market-specific factor?

(Multiple Choice)

4.9/5 (25)

At some point, further increases in interest rates on specific loans may decrease expected loan returns because of increased probability of default by the borrower.

(True/False)

4.7/5 (30)

From the perspective of an FI, which of the following is an advantage of a floating-rate loan?

(Multiple Choice)

4.9/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)