Exam 10: Credit Risk: Individual Loans

Exam 1: Why Are Financial Institutions Special90 Questions

Exam 2: Deposit-Taking Institutions43 Questions

Exam 3: Finance Companies71 Questions

Exam 4: Securities, Brokerage, and Investment Banking91 Questions

Exam 5: Mutual Funds, Hedge Funds, and Pension Funds61 Questions

Exam 6: Insurance Companies80 Questions

Exam 7: Risks of Financial Institutions110 Questions

Exam 8: Interest Rate Risk I110 Questions

Exam 9: Interest Rate Risk II116 Questions

Exam 10: Credit Risk: Individual Loans112 Questions

Exam 11: Credit Risk: Loan Portfolio and Concentration Risk51 Questions

Exam 12: Liquidity Risk85 Questions

Exam 13: Foreign Exchange Risk87 Questions

Exam 14: Sovereign Risk89 Questions

Exam 15: Market Risk95 Questions

Exam 16: Off-Balance-Sheet Risk101 Questions

Exam 17: Technology and Other Operational Risks107 Questions

Exam 18: Liability and Liquidity Management38 Questions

Exam 19: Deposit Insurance and Other Liability Guarantees54 Questions

Exam 20: Capital Adequacy102 Questions

Exam 21: Product and Geographic Expansion114 Questions

Exam 22: Futures and Forwards234 Questions

Exam 23: Options, Caps, Floors, and Collars113 Questions

Exam 24: Swaps95 Questions

Exam 25: Loan Sales83 Questions

Exam 26: Securitization Index98 Questions

Select questions type

Which of the following observations is true of a spot loan?

(Multiple Choice)

4.8/5  (35)

(35)

Recessionary phases in the business cycle typically cause greater hardship on companies that borrow large amounts.

(True/False)

4.9/5 (29)

Which of the following statements does not reflect a borrower-specific factor often used in qualitative default risk models?

(Multiple Choice)

5.0/5 (46)

If the spot interest rate on a prime-rated one-month CD is 6 percent today and the market rate on a two-month maturity prime-rated CD is 7 percent today, the implied forward rate on a one-month CD to be delivered one month from today is

(Multiple Choice)

4.8/5 (36)

The primary difficulty in arranging a syndicated loan is having all of the various lending and borrowing parties reach agreement on terms, rates, and collateral.

(True/False)

4.7/5 (26)

Usury ceilings are maximum rates imposed by legislation that FIs can charge on consumer and mortgage debt.

(True/False)

4.9/5 (32)

What is the most important factor determining bankruptcy, according to the Altman Z-score model?

(Multiple Choice)

5.0/5 (27)

The mortality rate is the past default experience of all loans, regardless of quality.

(True/False)

4.8/5 (27)

Because a compensating balance is the proportion of a loan that must be kept on deposit at the lending institution, the actual return to the lender on the usable portion of these loans is higher.

(True/False)

4.8/5 (35)

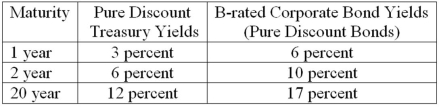

The following represents two yield curves.  What spread is expected between the one-year maturity B-rated bond and the one-year Treasury bond in one year?

What spread is expected between the one-year maturity B-rated bond and the one-year Treasury bond in one year?

(Multiple Choice)

4.7/5 (30)

Which of the following is NOT a valid conceptual or application problem of the mortality rate approach to estimate default risk?

(Multiple Choice)

4.8/5 (38)

What does the Moody's Analytics model use as equivalent to holding a call option on the assets of the firm?

(Multiple Choice)

4.9/5 (35)

Which of the following is not a qualitative factor in credit risk analysis?

(Multiple Choice)

4.8/5 (37)

The following is information on current spot and forward term structures (assume the corporate debt pays interest annually):  Using the term structure of default probabilities, the implied default probability for BBB corporate debt during the current year is

Using the term structure of default probabilities, the implied default probability for BBB corporate debt during the current year is

(Multiple Choice)

4.8/5 (30)

Generally, at the retail level, an FI controls credit risks solely by using a range of interest rates or prices and not by credit rationing.

(True/False)

4.8/5 (37)

The duration of a soon to be approved loan of $10 million is four years. The 99th percentile increase in risk premium for bonds belonging to the same risk category of the loan has been estimated to be 5.5 percent. If the minimum RAROC acceptable to the bank is 8 percent, what should be its expected percentage fee income in order for it to approve the loan?

(Multiple Choice)

4.9/5 (36)

The probability that a borrower would default in any specific time period is a marginal default probability.

(True/False)

4.9/5 (33)

The following is information on current spot and forward term structures (assume the corporate debt pays interest annually):  Calculate the value of x (the implied forward rate on one-year maturity Treasuries to be delivered in one year).

Calculate the value of x (the implied forward rate on one-year maturity Treasuries to be delivered in one year).

(Multiple Choice)

4.8/5 (31)

LIBOR, the London Interbank Offered Rate, is the rate for short-term interbank dollar loans in the domestic money-center bank market.

(True/False)

4.9/5 (35)

Credit risk applies only to bond investment and loan portfolios of FIs and banks.

(True/False)

4.7/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)