Exam 7: Efficiency, Exchange, and the Invisible Hand in Action

Exam 1: Thinking Like an Economist143 Questions

Exam 2: Comparative Advantage157 Questions

Exam 3: Supply and Demand120 Questions

Exam 4: Elasticity148 Questions

Exam 5: Demand134 Questions

Exam 6: Perfectly Competitive Supply152 Questions

Exam 7: Efficiency, Exchange, and the Invisible Hand in Action151 Questions

Exam 8: Monopoly, Oligopoly, and Monopolistic Competition141 Questions

Exam 9: Games and Strategic Behavior144 Questions

Exam 10: Externalities and Property Rights130 Questions

Exam 11: The Economics of Information123 Questions

Exam 12: Labor Markets, Poverty, and Income Distribution127 Questions

Exam 13: The Environment, Health, and Safety125 Questions

Exam 14: Public Goods and Tax Policy136 Questions

Select questions type

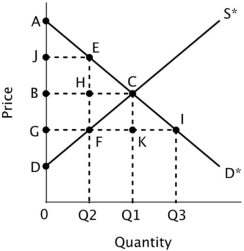

Refer to the figure below.  If a price ceiling were imposed at point G, then producer surplus would be represented by the area ______.

If a price ceiling were imposed at point G, then producer surplus would be represented by the area ______.

(Multiple Choice)

4.8/5  (34)

(34)

The cumulative difference between the price producers actually receive for a good and the lowest price for which they would have been willing to sell it is called:

(Multiple Choice)

4.9/5 (36)

The phrase "smart for one, but dumb for all" refers to the idea that the individual pursuit of self-interest:

(Multiple Choice)

4.8/5 (28)

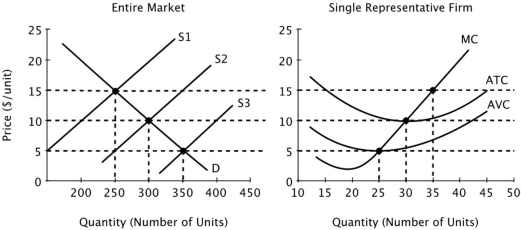

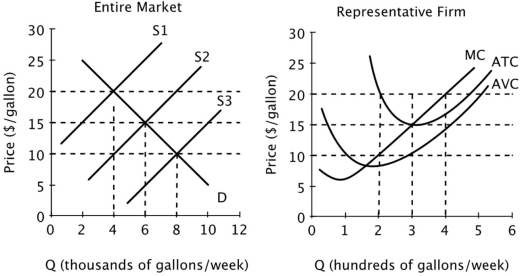

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  The long-run equilibrium price in this industry is:

The long-run equilibrium price in this industry is:

(Multiple Choice)

4.9/5 (27)

If an individual producer is willing to produce one unit of a good for $2.50 but is able to sell it for $7.50, then his or her producer surplus from the sale of that unit would be:

(Multiple Choice)

4.9/5 (35)

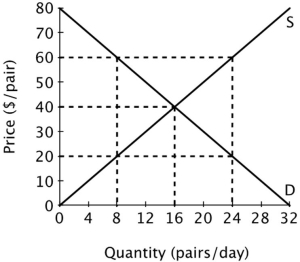

The figure below shows the supply and demand curves for jeans in Smallville.  Suppose jeans initially sell for $60 per pair. If the price of jeans falls to $40 per pair, then total economic surplus will increase by ______ per day.

Suppose jeans initially sell for $60 per pair. If the price of jeans falls to $40 per pair, then total economic surplus will increase by ______ per day.

(Multiple Choice)

4.8/5 (32)

Ingrid has been waiting for the show "Mamma Mia!" to come to town. When it finally does come, tickets cost $60. Ingrid's reservation price is $75. But when Ingrid tries to buy a ticket, they are sold out. Suppose Steven was able to purchase a ticket at the box office for $60. Steven's reservation price for the ticket is $65. If Steven attends "Mamma Mia!" and Ingrid does not, then this situation is:

(Multiple Choice)

4.7/5 (40)

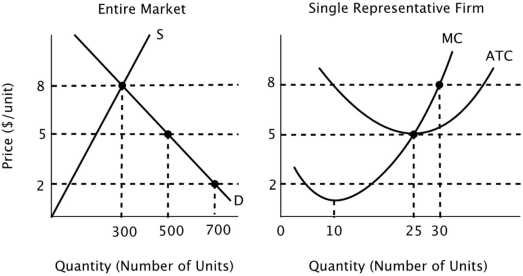

The figure below depicts the short-run market equilibrium in a perfectly competitive market and the cost curves for a representative firm in that market. Assume that all firms in this market have identical cost curves.  A starting assumption about this industry was that all of the firms in the market had identical cost curves. This assumption is:

A starting assumption about this industry was that all of the firms in the market had identical cost curves. This assumption is:

(Multiple Choice)

4.8/5 (37)

Which of the following is a characteristic of economic rent?

(Multiple Choice)

4.8/5 (27)

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  If S3 is the market supply curve, then each firm in this market will earn a economic loss of ______ per week.

If S3 is the market supply curve, then each firm in this market will earn a economic loss of ______ per week.

(Multiple Choice)

4.8/5 (23)

Factors of production are the most likely to earn economic rent when they:

(Multiple Choice)

4.8/5 (37)

Consider a perfectly competitive industry in a long-run equilibrium. If a single firm in that industry discovers a significant cost-saving production technology, then:

(Multiple Choice)

4.8/5 (33)

Suppose your economics professor has an extra copy of textbook that he or she would like to give to a student in the class. Which of the following schemes is the most likely to result in an efficient outcome?

(Multiple Choice)

4.8/5 (31)

If resources are misallocated in a perfectly competitive market, then in the long run profit opportunities will:

(Multiple Choice)

4.7/5 (28)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)