Exam 7: Efficiency, Exchange, and the Invisible Hand in Action

Exam 1: Thinking Like an Economist143 Questions

Exam 2: Comparative Advantage157 Questions

Exam 3: Supply and Demand120 Questions

Exam 4: Elasticity148 Questions

Exam 5: Demand134 Questions

Exam 6: Perfectly Competitive Supply152 Questions

Exam 7: Efficiency, Exchange, and the Invisible Hand in Action151 Questions

Exam 8: Monopoly, Oligopoly, and Monopolistic Competition141 Questions

Exam 9: Games and Strategic Behavior144 Questions

Exam 10: Externalities and Property Rights130 Questions

Exam 11: The Economics of Information123 Questions

Exam 12: Labor Markets, Poverty, and Income Distribution127 Questions

Exam 13: The Environment, Health, and Safety125 Questions

Exam 14: Public Goods and Tax Policy136 Questions

Select questions type

Suppose the market for coffee is in equilibrium at a price of $5 per pound. This means that:

(Multiple Choice)

4.9/5  (33)

(33)

Mary Jane is willing to babysit for $6 an hour. Her neighbor has asked her to babysit for $8 an hour. Assuming Mary Jane accepts the offer:

(Multiple Choice)

4.9/5 (30)

Generally, ______ motivates firms to enter an industry, while ______ motivates firms to exit an industry.

(Multiple Choice)

4.7/5 (37)

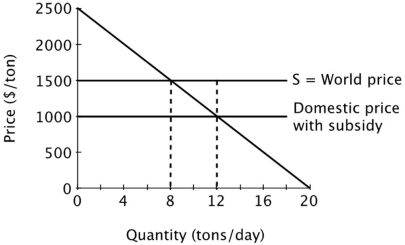

Suppose a small island nation imports sugar for its population at the world price of $1,500 per ton. The domestic market for sugar is shown below.  With no subsidy, the equilibrium price of sugar is ______ per ton, and the equilibrium quantity is ______ tons per day.

With no subsidy, the equilibrium price of sugar is ______ per ton, and the equilibrium quantity is ______ tons per day.

(Multiple Choice)

4.9/5 (32)

In a perfectly competitive market, if supply and demand fully reflect all of the costs and benefits associated with production and consumption, then total economic surplus is maximized when:

(Multiple Choice)

4.9/5 (36)

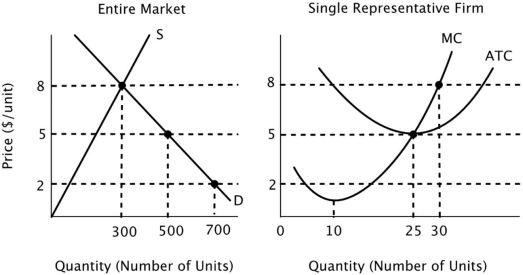

The figure below depicts the short-run market equilibrium in a perfectly competitive market and the cost curves for a representative firm in that market. Assume that all firms in this market have identical cost curves.  In the long run equilibrium in this market:

In the long run equilibrium in this market:

(Multiple Choice)

4.9/5 (40)

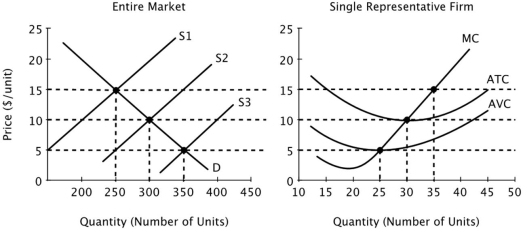

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  In the short run, firms in this market will shut down if the market price is:

In the short run, firms in this market will shut down if the market price is:

(Multiple Choice)

4.9/5 (34)

Entry into a perfectly competitive industry to occurs whenever:

(Multiple Choice)

4.9/5 (40)

Superstar professional athletes can sustain their economic rents because:

(Multiple Choice)

4.9/5 (40)

The supplier of a factor of production has a reservation price of $100. The purchaser of the factor of production has a reservation price of $200. If the factor of production is unique, then:

(Multiple Choice)

4.9/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)