Exam 7: Efficiency, Exchange, and the Invisible Hand in Action

Exam 1: Thinking Like an Economist143 Questions

Exam 2: Comparative Advantage157 Questions

Exam 3: Supply and Demand120 Questions

Exam 4: Elasticity148 Questions

Exam 5: Demand134 Questions

Exam 6: Perfectly Competitive Supply152 Questions

Exam 7: Efficiency, Exchange, and the Invisible Hand in Action151 Questions

Exam 8: Monopoly, Oligopoly, and Monopolistic Competition141 Questions

Exam 9: Games and Strategic Behavior144 Questions

Exam 10: Externalities and Property Rights130 Questions

Exam 11: The Economics of Information123 Questions

Exam 12: Labor Markets, Poverty, and Income Distribution127 Questions

Exam 13: The Environment, Health, and Safety125 Questions

Exam 14: Public Goods and Tax Policy136 Questions

Select questions type

Adam Smith's theory of the invisible hand posits that the most efficient allocation of resources is often achieved by:

Free

(Multiple Choice)

4.8/5  (30)

(30)

Correct Answer: Verified

Verified

D

Which of the following is NOT an example of an explicit cost?

Free

(Multiple Choice)

4.8/5 (43)

Correct Answer:Verified

B

A price ceiling that is set below the equilibrium price will cause:

Free

(Multiple Choice)

4.7/5 (36)

Correct Answer:Verified

A

Which of the following statements best expresses why economic efficiency should be society's first goal?

(Multiple Choice)

4.8/5 (33)

Duke is a highly skilled negotiator who could work for many law firms. The law firm that hires Duke is able to collect twice as much revenue per hour of Duke's time than it can for any other negotiator in town. The increased revenue will:

(Multiple Choice)

4.9/5 (34)

Suppose farmers in a given market can either grow soy beans or corn on their land. In addition, suppose an increase in the demand for corn causes the price of corn to increase. As a result of the increase in the price of corn, farmers who were already growing corn will earn an:

(Multiple Choice)

4.9/5 (38)

Suppose you own a small business. Last month, your total revenue was $6,000. In addition, you paid: $1,000 in monthly rent for office space.

$200 in monthly rent for equipment.

$3,000 to your workers in wages for the month.

$1,000 for the supplies you used that month.

If you correctly determine that your economic profit last month was negative $200, then it must be true that:

(Multiple Choice)

4.9/5 (38)

Refer to the table below. An output level of 25 units, this firm's accounting profit is ______, and its economic profit is ______. Quantity Total Revenue Explicit Costs Implicit Costs 10 50 36 5 15 75 63 6 20 100 93 7 25 125 125 8 30 150 161 9

(Multiple Choice)

4.9/5 (38)

Which of the following statements about explicit costs is true?

(Multiple Choice)

4.8/5 (28)

Which of the following is NOT necessarily true in a market equilibrium?

(Multiple Choice)

4.8/5 (30)

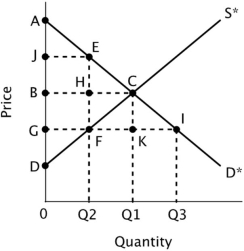

Refer to the figure below.  If a price ceiling were imposed at point G, the loss in total economic surplus would be represented by the area ______.

If a price ceiling were imposed at point G, the loss in total economic surplus would be represented by the area ______.

(Multiple Choice)

4.9/5 (35)

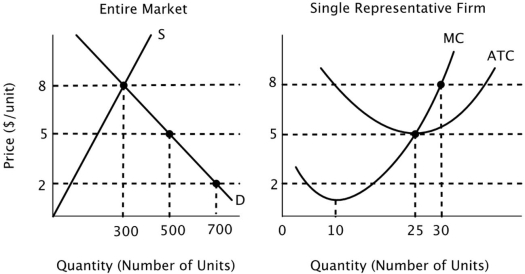

The figure below depicts the short-run market equilibrium in a perfectly competitive market and the cost curves for a representative firm in that market. Assume that all firms in this market have identical cost curves.  Given that the current equilibrium price is $8, what will happen to the number of firms in this market in the long run?

Given that the current equilibrium price is $8, what will happen to the number of firms in this market in the long run?

(Multiple Choice)

4.9/5 (32)

The role that prices play in distributing scarce goods and services to those consumers who value them the most highly is known as the ______ function of price.

(Multiple Choice)

4.8/5 (39)

If all firms in a perfectly competitive industry are earning a normal profit, then:

(Multiple Choice)

4.9/5 (39)

In perfectly competitive markets, an implication of entry and exit in response to economic profit and loss is that:

(Multiple Choice)

4.8/5 (33)

The role that prices play in directing resources away from overcrowded markets and towards markets that are underserved is known as the ______ function of price.

(Multiple Choice)

4.8/5 (41)

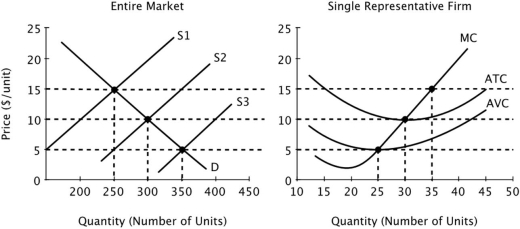

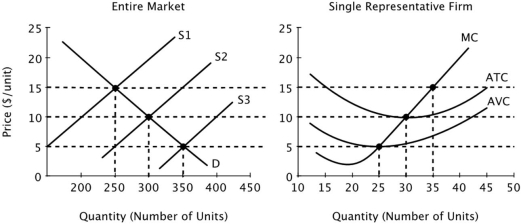

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  In the long run, there will be ______ firms in this market.

In the long run, there will be ______ firms in this market.

(Multiple Choice)

4.7/5 (37)

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  If the market supply curve is given by S3, then in the long run firms will:

If the market supply curve is given by S3, then in the long run firms will:

(Multiple Choice)

4.8/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)