Exam 7: Efficiency, Exchange, and the Invisible Hand in Action

Exam 1: Thinking Like an Economist143 Questions

Exam 2: Comparative Advantage157 Questions

Exam 3: Supply and Demand120 Questions

Exam 4: Elasticity148 Questions

Exam 5: Demand134 Questions

Exam 6: Perfectly Competitive Supply152 Questions

Exam 7: Efficiency, Exchange, and the Invisible Hand in Action151 Questions

Exam 8: Monopoly, Oligopoly, and Monopolistic Competition141 Questions

Exam 9: Games and Strategic Behavior144 Questions

Exam 10: Externalities and Property Rights130 Questions

Exam 11: The Economics of Information123 Questions

Exam 12: Labor Markets, Poverty, and Income Distribution127 Questions

Exam 13: The Environment, Health, and Safety125 Questions

Exam 14: Public Goods and Tax Policy136 Questions

Select questions type

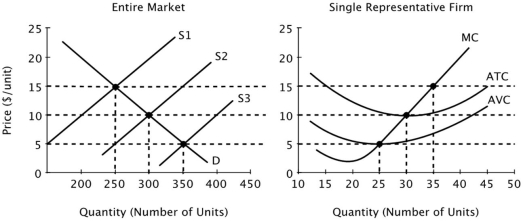

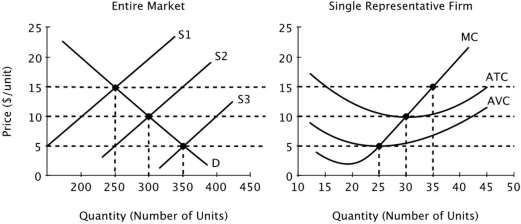

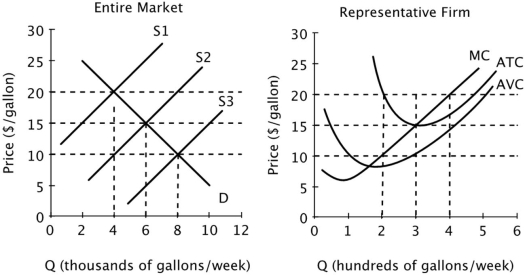

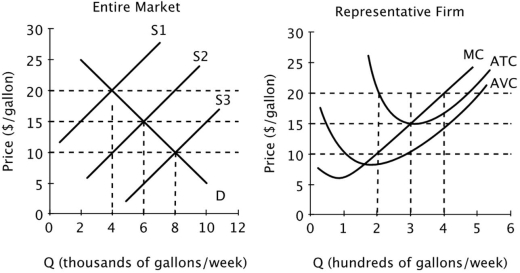

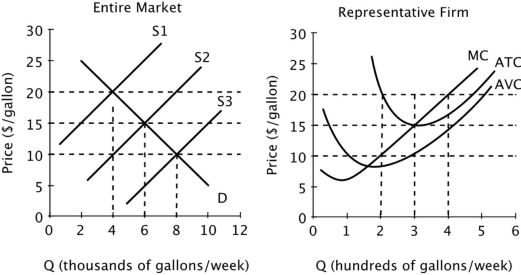

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  If the market supply curve is given by S1, then in the long run firms will:

If the market supply curve is given by S1, then in the long run firms will:

(Multiple Choice)

4.8/5  (27)

(27)

Pat used to work as an aerobics instructor at the local gym earning $35,000 a year. Pat quit that job and started working as a personal trainer. Pat makes $50,000 in total annual revenue. Pat's only out-of-pocket costs are $12,000 per year for rent and utilities, $1,000 per year for advertising and $3,000 per year for equipment. For Pat to earn normal profit, Pat's accounting profit would have to be ______.

(Multiple Choice)

4.8/5 (28)

Suppose the production of cotton causes substantial environmental damage because the pesticides used by cotton farmers often make their way into nearby rivers and streams, and are very harmful to fish and other wildlife. Economists would consider the environmental damage that results from the production of cotton to be a(n):

(Multiple Choice)

4.8/5 (29)

Suppose the production of cotton causes substantial environmental damage because the pesticides used by cotton farmers often make their way into nearby rivers and streams, and are very harmful to fish and other wildlife. If cotton farmers do not have to pay for the environmental damage caused by the pesticides used to grow cotton, then the market equilibrium price will be ______ and the market equilibrium quantity will be ______.

(Multiple Choice)

4.9/5 (36)

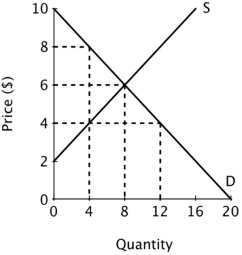

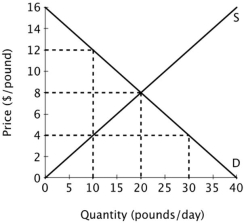

Refer to the figure below.  If a price ceiling were imposed at $4, consumer surplus would be:

If a price ceiling were imposed at $4, consumer surplus would be:

(Multiple Choice)

4.8/5 (37)

E-commerce and an internet presence are important to many firms, requiring employees with specialized skills that are in short supply. The invisible hand solves the employment problem by:

(Multiple Choice)

4.9/5 (33)

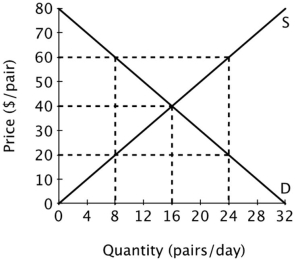

The figure below shows the supply and demand curves for jeans in Smallville.  At a price of $60 per pair, there will be an excess ______ of ______ pairs of jeans per day.

At a price of $60 per pair, there will be an excess ______ of ______ pairs of jeans per day.

(Multiple Choice)

4.8/5 (31)

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  The firm depicted in the graph on the right faces a demand curve that is:

The firm depicted in the graph on the right faces a demand curve that is:

(Multiple Choice)

4.8/5 (28)

Refer to the table below. An output level of 15 units, this firm's accounting profit is ______, and its economic profit is ______. Quantity Total Revenue Explicit Costs Implicit Costs 10 50 36 5 15 75 63 6 20 100 93 7 25 125 125 8 30 150 161 9

(Multiple Choice)

4.9/5 (30)

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  If the market supply curve is given by S3, then what will happen to the market supply curve in the long run?

If the market supply curve is given by S3, then what will happen to the market supply curve in the long run?

(Multiple Choice)

4.8/5 (33)

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  If S3 is the market supply curve, then in the short run, the profit-maximizing level of output for a single firm in this market is ______ gallons per week.

If S3 is the market supply curve, then in the short run, the profit-maximizing level of output for a single firm in this market is ______ gallons per week.

(Multiple Choice)

4.7/5 (36)

The figure below shows the supply and demand curves for oranges in Smallville.  When this market is in equilibrium, total economic surplus is ______ per day.

When this market is in equilibrium, total economic surplus is ______ per day.

(Multiple Choice)

4.7/5 (34)

If you were to start your own business, your implicit costs would include the:

(Multiple Choice)

4.8/5 (29)

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  In the long run, the equilibrium price will be _____ per gallon, and each firm's profit-maximizing quantity will be ______ gallons per week.

In the long run, the equilibrium price will be _____ per gallon, and each firm's profit-maximizing quantity will be ______ gallons per week.

(Multiple Choice)

5.0/5 (36)

Refer to the table below. At what output level or levels are this firm's owners doing as well as or better than they could do with the next best use of their resources? Quantity Total Revenue Explicit Costs Implicit Costs 10 50 36 5 15 75 63 6 20 100 93 7 25 125 125 8 30 150 161 9

(Multiple Choice)

4.8/5 (35)

The statement, "If a deal is too good to be true, then it probably is not true," is most closely related to which core economic principle?

(Multiple Choice)

4.8/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)