Exam 28: Accounting for Group Structures

Exam 1: An Overview of the Australian External Reporting Environment50 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financ62 Questions

Exam 3: Theories of Financial Accounting61 Questions

Exam 4: An Overview of Accounting for Assets62 Questions

Exam 5: Depreciation of Property, plant and Equipment62 Questions

Exam 6: Revaluation and Impairment Testing of Non-Current Assets59 Questions

Exam 7: Inventory61 Questions

Exam 8: Accounting for Intangibles61 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets61 Questions

Exam 10: An Overview of Accounting for Liabilities58 Questions

Exam 11: Accounting for Lease78 Questions

Exam 12: Set-Off and Extinguishment of Debt47 Questions

Exam 13: Accounting for Employee Benefits67 Questions

Exam 14: Share Capital and Reserves66 Questions

Exam 15: Accounting for Financial Instruments72 Questions

Exam 16: Revenue Recognition Issues64 Questions

Exam 17: The Statement of Comprehensive Income and Statement of Changes in E62 Questions

Exam 18: Accounting for Share-Based Payments62 Questions

Exam 19: Accounting for Income Taxes56 Questions

Exam 20: Cash-Flow Statements60 Questions

Exam 21: Accounting for the Extractive Industries60 Questions

Exam 22: Accounting for General Insurance Contracts58 Questions

Exam 23: Accounting for Superannuation Plans62 Questions

Exam 24: Events Occurring After Balance Sheet Date62 Questions

Exam 25: Segment Reporting61 Questions

Exam 26: Related-Party Disclosures59 Questions

Exam 27: Earnings Per Share43 Questions

Exam 28: Accounting for Group Structures69 Questions

Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact46 Questions

Exam 30: Further Consolidation Issues II: Accounting for Minority Interests34 Questions

Exam 31: Further Consolidation Issues III: Accounting for Indirect Ownershi38 Questions

Exam 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg39 Questions

Exam 33: Accounting for Equity Investments67 Questions

Exam 33: Accounting for Equity Investments59 Questions

Exam 35: Accounting for Foreign Currency Transactions58 Questions

Exam 36: Translation of the Accounts of Foreign Operations41 Questions

Exam 37: Accounting for Corporate Social Responsibility59 Questions

Select questions type

AASB 127 notes that in preparing consolidated financial statements,an entity combines the financial statements of the parent and the subsidiaries line by line by adding together,in proportion to the degree of ownership,like items of assets,liabilities,income and expenses; but not equity balances:

(True/False)

4.9/5  (31)

(31)

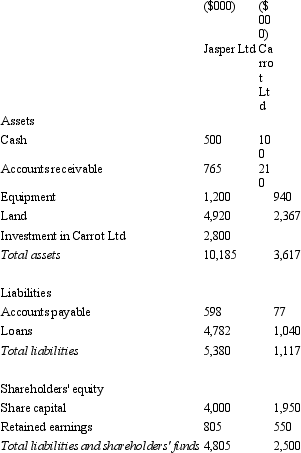

Jasper Ltd acquires all the issued capital of Carrot Ltd for a cash payment of $2,800,000 on 30 June 2004.The balance sheet of both entities at purchase date is:  Assuming the assets of Carrot Ltd are recorded at fair value,what is the consolidated balance sheet at the date of purchase?

Assuming the assets of Carrot Ltd are recorded at fair value,what is the consolidated balance sheet at the date of purchase?

(Multiple Choice)

4.9/5 (39)

When an acquirer makes a bargain purchase in a business combination,the excess that remains is recognised in profit or loss of the acquirer on acquisition date.

(True/False)

4.9/5 (34)

On 1 July 2012,Goliath Ltd acquires all shares in David Ltd for $800 000.The fair value of net assets acquired is $920 000 comprised of $600,000 in share capital and $320 000 in retained earnings.What is the appropriate elimination entry for this investment that is in accordance with AASB 3 "Business Combinations" and AASB 127 "Consolidated and Separate Financial Statements"?

(Multiple Choice)

4.9/5 (29)

Sullivan (1985)argued that the preparation of group accounts can proceed to the fulfilment of the true and fair notion only when partitioning is fully enforced.

(True/False)

4.9/5 (29)

Which of the following statements accurately describes important aspects of consolidation after the date of acquisition?

(Multiple Choice)

4.8/5 (38)

In what situation does an excess on acquisition arise and how does AASB 3 require it to be treated?

(Multiple Choice)

4.9/5 (46)

One important aim of releasing AAS 24 in 1991 and amendments made to The Corporations Law in the same year was to:

(Multiple Choice)

4.8/5 (33)

Under AASB 127 parent companies may choose whether to present one set of consolidated accounts or to provide two or more sub-sets of the consolidated accounts to cover the whole group:

(True/False)

5.0/5 (31)

The purpose of providing consolidated statements is to show the results and financial position of a group as if it were operating with a single source of finance:

(True/False)

4.9/5 (38)

Which of the following statements accurately describes the elimination entry to eliminate pre-acquisition shareholders' funds?

(Multiple Choice)

4.9/5 (41)

On consolidation,the investment in subsidiary,shown in the investor's books,shall be eliminated in full against which of the following?

(Multiple Choice)

4.7/5 (42)

Which of the following statements is an accurate description of the difference between a legal entity and an economic entity?

(Multiple Choice)

4.9/5 (37)

A former loophole (now closed)that existed under the former s.9 of the Corporations Law:

(Multiple Choice)

4.9/5 (37)

AASB 127 identifies a number of factors that may indicate the existence of control.These include:

(Multiple Choice)

4.8/5 (30)

In a situation where the net assets acquired in the controlled entity are not recorded at fair value,approaches that may be taken to account for this include:

(Multiple Choice)

4.8/5 (29)

The consolidation process does not involve any adjustments to the financial statements of the individual entities making up the group:

(True/False)

4.9/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)