Exam 28: Accounting for Group Structures

Exam 1: An Overview of the Australian External Reporting Environment50 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financ62 Questions

Exam 3: Theories of Financial Accounting61 Questions

Exam 4: An Overview of Accounting for Assets62 Questions

Exam 5: Depreciation of Property, plant and Equipment62 Questions

Exam 6: Revaluation and Impairment Testing of Non-Current Assets59 Questions

Exam 7: Inventory61 Questions

Exam 8: Accounting for Intangibles61 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets61 Questions

Exam 10: An Overview of Accounting for Liabilities58 Questions

Exam 11: Accounting for Lease78 Questions

Exam 12: Set-Off and Extinguishment of Debt47 Questions

Exam 13: Accounting for Employee Benefits67 Questions

Exam 14: Share Capital and Reserves66 Questions

Exam 15: Accounting for Financial Instruments72 Questions

Exam 16: Revenue Recognition Issues64 Questions

Exam 17: The Statement of Comprehensive Income and Statement of Changes in E62 Questions

Exam 18: Accounting for Share-Based Payments62 Questions

Exam 19: Accounting for Income Taxes56 Questions

Exam 20: Cash-Flow Statements60 Questions

Exam 21: Accounting for the Extractive Industries60 Questions

Exam 22: Accounting for General Insurance Contracts58 Questions

Exam 23: Accounting for Superannuation Plans62 Questions

Exam 24: Events Occurring After Balance Sheet Date62 Questions

Exam 25: Segment Reporting61 Questions

Exam 26: Related-Party Disclosures59 Questions

Exam 27: Earnings Per Share43 Questions

Exam 28: Accounting for Group Structures69 Questions

Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact46 Questions

Exam 30: Further Consolidation Issues II: Accounting for Minority Interests34 Questions

Exam 31: Further Consolidation Issues III: Accounting for Indirect Ownershi38 Questions

Exam 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg39 Questions

Exam 33: Accounting for Equity Investments67 Questions

Exam 33: Accounting for Equity Investments59 Questions

Exam 35: Accounting for Foreign Currency Transactions58 Questions

Exam 36: Translation of the Accounts of Foreign Operations41 Questions

Exam 37: Accounting for Corporate Social Responsibility59 Questions

Select questions type

Minority interests (minority interests)are defined as the equity in the parent company that is not provided by the group shareholders:

(True/False)

4.9/5  (35)

(35)

The lack of a direct link between levels of ownership and control (i.e.,the degree of ownership does not,of itself,determine if an entity has control of another):

(Multiple Choice)

4.9/5 (35)

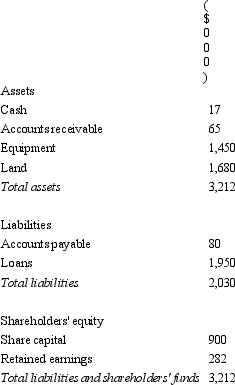

Fresco Ltd acquires all the issued capital of Indoor Ltd for a cash payment of $1,000,000 on 30 June 2005.The balance sheet of Indoor Ltd at purchase date is:  Assuming the assets of Indoor Ltd are at fair value,what is the entry to eliminate the investment in Fresco Ltd?

Assuming the assets of Indoor Ltd are at fair value,what is the entry to eliminate the investment in Fresco Ltd?

(Multiple Choice)

4.8/5 (34)

Gingimup Ltd purchased all the equity of Kindawansa Ltd on 30 June 2005.At that time the carrying value of the net assets of Kindawansa was $1,200,000.This amount was made up in equity as follows: share capital $1,000,000; retained earnings $200,000.Kindawansa has held some valuable land for a long time (purchased at $ 1,200,000),but has not revalued it.Its fair value at 30 June 2005 was $2,800,000 (all other non-current assets are recorded at fair value).Gingimup Ltd paid cash consideration of $3,000,000 for Kindawansa Ltd.Assuming that the land has not been revalued in the controlled entity's books,what are the elimination entries required to reflect the purchase of Kindawansa Ltd?

(Multiple Choice)

4.8/5 (42)

In the situation in which a subsidiary is only controlled temporarily,AASB 127 requires:

(Multiple Choice)

4.8/5 (37)

Richer Ltd is owed a material amount by Poorer Partnership.Poorer is heavily in debt to Richer Ltd,but due to an unexpected economic downturn is unable to make repayments according to schedule.The board of Richer Ltd believes that Poorer has a good chance of trading out of its current economic difficulties as its management and product are sound and the current problems stem from external factors that are expected to pass within the next 12 to 18 months.Richer Ltd enters into an arrangement with Poorer to manage its finances until the economic situation reverses.At this stage it is not perceived as necessary for Richer Ltd to be otherwise involved in the running of Poorer.Given the situation described,what is Richer Ltd most likely to be required to do to account for Poorer under AASB 127?

(Multiple Choice)

4.8/5 (32)

In the situation in which a subsidiary revalues its non-current assets to fair value in its books as part of being acquired by a parent entity,the accounting treatment is:

(Multiple Choice)

4.8/5 (30)

The partition effect in relation to a group of companies arose when:

(Multiple Choice)

4.7/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)