Exam 12: Alternative Minimum Tax

Exam 1: An Introduction to Taxation and Understanding the Federal Tax Law195 Questions

Exam 2: Working With the Tax Law86 Questions

Exam 3: Tax Formula and Tax Determination;an Overview of Property Transactions188 Questions

Exam 4: Gross Income: Concepts and Inclusions124 Questions

Exam 5: Gross Income: Exclusions114 Questions

Exam 6: Deductions and Losses: in General142 Questions

Exam 7: Deductions and Losses: Certain Business Expenses and Losses120 Questions

Exam 8: Depreciation, cost Recovery, amortization, and Depletion115 Questions

Exam 9: Deductions: Employee and Self-Employed-Related Expenses177 Questions

Exam 10: Deductions and Losses: Certain Itemized Deductions104 Questions

Exam 11: Investor Losses110 Questions

Exam 12: Alternative Minimum Tax119 Questions

Exam 13: Tax Credits and Payment Procedures124 Questions

Exam 14: Property Transactions: Determination of Gain or Loss and Basis Considerations142 Questions

Exam 15: Property Transactions: Nontaxable Exchanges120 Questions

Exam 16: Property Transactions: Capital Gains and Losses72 Questions

Exam 17: Property Transactions: 1231 and Recapture Provisions70 Questions

Exam 18: Accounting Periods and Methods108 Questions

Exam 19: Deferred Compensation102 Questions

Exam 20: Corporations and Partnerships207 Questions

Select questions type

Identify an AMT adjustment that applies for the individual taxpayer that does not apply for the corporate taxpayer and identify an AMT adjustment that applies for the corporate taxpayer that does not apply for the individual taxpayer.

(Essay)

4.8/5  (36)

(36)

Keosha acquires 10-year personal property to use in her business in 2014 and takes the maximum cost recovery deduction for regular income tax purposes.As a result of this,Keosha will have a positive AMT adjustment in 2014.

(True/False)

4.9/5 (31)

Nell has a personal casualty loss deduction of $14,500 for regular income tax purposes.The deduction would have been $26,600,but it had to be reduced by $100 and by $12,000 (10% × $120,000 AGI).For AMT purposes,the casualty loss deduction also is $14,500.

(True/False)

4.8/5 (30)

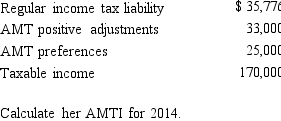

Beula,who is a head of household and age 40,provides you with the following information from her financial records for 2014.

(Multiple Choice)

4.8/5 (39)

When qualified residence interest exceeds qualified housing interest,the positive adjustment required in calculating AMT is a timing adjustment.That is,in the future,there will be an offsetting negative adjustment.Comment on the validity of this statement.

(Essay)

4.9/5 (40)

Vinny's AGI is $250,000.He contributed $200,000 in cash to the Boy Scouts,a public charity.What is Vinny's charitable contribution deduction for AMT purposes?

(Multiple Choice)

4.9/5 (36)

For the ACE adjustment,discuss the relationship between ACE and unadjusted AMTI.

(Essay)

4.8/5 (35)

The deduction for charitable contributions in calculating the regular income tax can differ from that in calculating the AMT because the percentage limitations (20%,30%,and 50%)may be applied to a different base amount.

(True/False)

4.9/5 (36)

What effect do deductible gambling losses for regular income tax purposes have in calculating AMTI?

(Essay)

5.0/5 (32)

Paul incurred circulation expenditures of $180,000 in 2014 and deducted that amount for regular income tax purposes.Paul has a $60,000 negative AMT adjustment for 2015,2016,and for 2017.

(True/False)

4.9/5 (37)

Tad and Audria,who are married filing a joint return,have AMTI of $256,000 for 2014.Calculate their AMT exemption.

(Essay)

4.7/5 (33)

Dale owns and operates Dale's Emporium as a sole proprietorship.On January 30,1998,Dale's Emporium acquired a warehouse for $100,000.For regular income tax purposes in 2014,depreciation was deducted under MACRS using a rate of 2.564%.Determine the AMT adjustment for depreciation and indicate whether it is positive or negative.

(Multiple Choice)

4.8/5 (36)

Andrea,who is single,has a personal exemption deduction in calculating her 2014 taxable income.She has no dependency deductions.What is the amount of the AMT adjustment in calculating AMTI?

(Essay)

4.8/5 (36)

Are the AMT rates for the individual taxpayer the same as those for a corporate taxpayer?

(Essay)

4.8/5 (35)

Is it possible that no AMT adjustment is necessary for medical expenses in calculating AMTI for a taxpayer who is at least age 65 even though the floor limitation is different (7.5% of AGI for regular income tax compared to 10% for AMT purposes)?

(Essay)

4.9/5 (40)

In 2014,Linda incurs circulation expenses of $240,000 which she deducts in calculating taxable income.

a.Calculate Linda's AMT adjustment for circulation expenses for 2014,2015,2016,and 2017.

b.Advise Linda on how she could reduce or eliminate the AMT adjustment in 2014.

(Essay)

5.0/5 (36)

Danica owned a car that she used exclusively for business.The car was purchased in 2010 and sold in 2014 for a recognized gain of $9,000.However,the sale resulted in no AMT.Why?

(Essay)

4.8/5 (44)

66. Wallace owns a construction company that builds both commercial and residential buildings. He contracts to build a residential building for $800,000 for which he is eligible to use the completed contract method of accounting. In the current year for regular income tax purposes, Wallace does not recognize any income on the contract. Under the percentage of completion method, the income recognized under the contract would have been $60,000. Wallace’s AMT adjustment is:

(Multiple Choice)

4.8/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)