Exam 12: Alternative Minimum Tax

Exam 1: An Introduction to Taxation and Understanding the Federal Tax Law195 Questions

Exam 2: Working With the Tax Law86 Questions

Exam 3: Tax Formula and Tax Determination;an Overview of Property Transactions188 Questions

Exam 4: Gross Income: Concepts and Inclusions124 Questions

Exam 5: Gross Income: Exclusions114 Questions

Exam 6: Deductions and Losses: in General142 Questions

Exam 7: Deductions and Losses: Certain Business Expenses and Losses120 Questions

Exam 8: Depreciation, cost Recovery, amortization, and Depletion115 Questions

Exam 9: Deductions: Employee and Self-Employed-Related Expenses177 Questions

Exam 10: Deductions and Losses: Certain Itemized Deductions104 Questions

Exam 11: Investor Losses110 Questions

Exam 12: Alternative Minimum Tax119 Questions

Exam 13: Tax Credits and Payment Procedures124 Questions

Exam 14: Property Transactions: Determination of Gain or Loss and Basis Considerations142 Questions

Exam 15: Property Transactions: Nontaxable Exchanges120 Questions

Exam 16: Property Transactions: Capital Gains and Losses72 Questions

Exam 17: Property Transactions: 1231 and Recapture Provisions70 Questions

Exam 18: Accounting Periods and Methods108 Questions

Exam 19: Deferred Compensation102 Questions

Exam 20: Corporations and Partnerships207 Questions

Select questions type

The AMT adjustment for research and experimental expenditures can be avoided if the taxpayer capitalizes the expenditures and amortizes them over a 10-year period.

(True/False)

4.7/5  (36)

(36)

In May 2012,Swallow,Inc. ,issues options to Karrie,a corporate officer,to purchase 100 shares of Swallow stock under an ISO plan.At the date the stock options are issued,the fair market value of the stock is $1,000 per share and the option price is $1,200 per share.The stock becomes freely transferable in 2013.Karrie exercises the options in November 2012 when the stock is selling for $1,500 per share.She sells the stock in December 2014 for $1,800 per share.

a.Determine the amount of the AMT adjustment for 2012.

b.Determine the amount of the AMT adjustment for 2013.

c.Determine Karrie's recognized gain for regular income tax purposes and for

AMT purposes in 2014 on the sale of the stock.

d.Determine the amount of the AMT adjustment for 2014.

(Essay)

4.9/5 (35)

Prior to the effect of tax credits,Eunice's regular income tax liability is $325,000 and her tentative AMT is $312,000.Eunice has general business credits available of $20,000.Calculate Eunice's tax liability after tax credits.

(Multiple Choice)

4.8/5 (38)

Eula owns a mineral property that had a basis of $23,000 at the beginning of the year.Cost depletion is $19,000.The property qualifies for a 15% depletion rate.Gross income from the property was $200,000 and net income before the percentage depletion deduction was $50,000.What is Eula's tax preference for excess depletion?

(Multiple Choice)

4.9/5 (38)

Marvin,the vice president of Lavender,Inc. ,exercises stock options for 100 shares of stock in March 2014.The stock options are incentive stock options (ISOs).Their exercise price is $20 and the fair market value on the date of exercise is $28.The options were granted in March 2010 and all restrictions on the free transferability had lapsed by the exercise date.

(Multiple Choice)

4.9/5 (41)

If the taxpayer elects to capitalize intangible drilling costs and to amortize them over a 3-year period for regular income tax purposes,there is no adjustment or preference for AMT purposes.

(True/False)

4.7/5 (42)

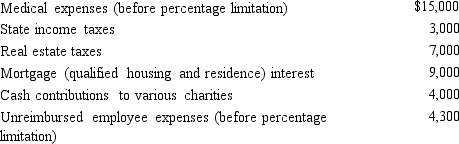

Darin's,who is age 30,has itemized deductions in calculating 2014 taxable income as follows:

Medical expenses [\ 15,000-10\%(\ 100,000)] \ 5,000 Mortgage interest on personal residence 7,000 State income taxes 4,000 Real property taxes 4,500 Personal property taxes 2,500 Casualty loss [\ 14,000-(10\%\times\ 100,000)] 4,000 Charitable contributions 3,500 Gambling losses (\ 3,200 limited to gambling income of \ 1,000) 1,000 Miscellaneous itemized deductions [\ 2.500-2\%(\ 100,000)] 500 Itemized deductions \3 2,000

a.Calculate Darin's itemized deductions for AMT purposes using the direct method.

b.Calculate Darin's itemized deductions for AMT purposes using the indirect method.

(Essay)

4.9/5 (43)

The AMT calculated using the indirect method will produce a different amount than the AMT calculated using the direct method.

(True/False)

4.8/5 (31)

Joel placed real property in service in 2014 that cost $900,000 and used MACRS for regular income tax purposes.He is required to make a positive adjustment for AMT purposes in 2014 for the excess of depreciation calculated for regular income tax purposes over the depreciation calculated for AMT purposes.

(True/False)

4.9/5 (42)

The AMT adjustment for mining exploration and development costs can be avoided if the taxpayer elects to write off the expenditures in the year incurred for regular income tax purposes,rather than writing off the expenditures over a 10-year period for regular income tax purposes.

(True/False)

4.8/5 (38)

Durell owns a construction company that builds residential housing.The company is eligible to use the completed contract method for regular income tax purposes.What can Durell do to minimize his AMT?

(Essay)

4.9/5 (39)

How can an AMT adjustment be avoided for a taxpayer who incurs circulation expenditures in the current tax year?

(Essay)

4.8/5 (38)

Kay had percentage depletion of $119,000 for the current year for regular income tax purposes.Cost depletion was $60,000.Her basis in the property was $90,000 at the beginning of the current year.Kay must treat the percentage depletion deducted in excess of cost depletion,or $59,000,as a tax preference in computing AMTI.

(True/False)

4.7/5 (34)

The amount of the deduction for medical expenses under the regular income tax may be different than for AMT purposes if the taxpayer is at least age 65.

(True/False)

4.8/5 (47)

In determining the amount of the AMT adjustments,discuss the difference in the treatment of a building placed in service after 1986 and before January 1,1999 and a building placed in service after December 31,1998.

(Essay)

4.8/5 (37)

Mitch,who is single and age 66 and has no dependents,had AGI of $100,000 in 2014.His potential itemized deductions were as follows:  What is the amount of Mitch's AMT adjustment for itemized deductions for 2014?

What is the amount of Mitch's AMT adjustment for itemized deductions for 2014?

(Multiple Choice)

4.9/5 (41)

Certain adjustments apply in calculating the corporate AMT that do not apply in calculating the noncorporate AMT and certain adjustments apply in calculating the noncorporate AMT that do not apply in calculating the corporate AMT.

(True/False)

4.9/5 (41)

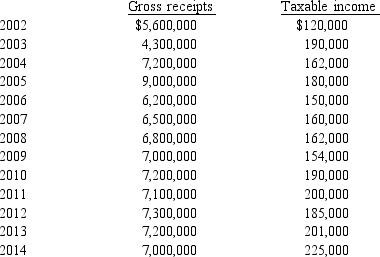

Sage,Inc. ,has the following gross receipts and taxable income:

Is Sage,Inc. ,subject to the AMT in 2014?

Is Sage,Inc. ,subject to the AMT in 2014?

(Essay)

4.9/5 (39)

Income from some long-term contracts can be reported using the completed contract method for regular income tax purposes,but the percentage of completion method is required for AMT purposes for all long-term contracts.

(True/False)

4.9/5 (45)

Melinda is in the 35% marginal tax bracket.She has a net capital gain of $150,000 on the sale of land which is eligible for the alternative tax on net capital gain in calculating the regular income tax.Discuss the tax rate that applies to the $150,000 net capital gain in calculating the tentative AMT for Melinda.

(Essay)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)