Exam 7: Consumer Choice and Elasticity

Exam 1: Economics: Foundations and Models160 Questions

Exam 2: Trade-Offs, comparative Advantage, and the Market System191 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply241 Questions

Exam 4: Market Efficiency and Market Failure226 Questions

Exam 5: The Economics of Healthcare169 Questions

Exam 6: Firms,the Stock Market,and Corporate Governance255 Questions

Exam 7: Consumer Choice and Elasticity270 Questions

Exam 8: Technology, production, and Costs277 Questions

Exam 9: Firms in Perfectly Competitive Markets351 Questions

Exam 10: Monopoly and Antitrust253 Questions

Exam 11: Monopolistic Competition and Oligopoly304 Questions

Exam 12: GDP: Measuring Total Production and Income200 Questions

Exam 13: Unemployment and Inflation207 Questions

Exam 14: Economic Growth, the Financial System and Business Cycles172 Questions

Exam 15: Aggregate Demand and Aggregate Supply Analysis120 Questions

Exam 16: Money, banks, and the Federal Reserve System139 Questions

Exam 17: Monetary Policy180 Questions

Exam 18: Fiscal Policy131 Questions

Exam 19: Comparative Advantage, international Trade, and Exchange Rates247 Questions

Select questions type

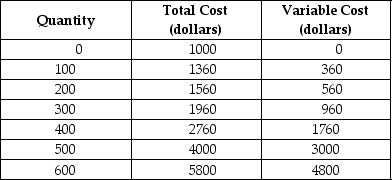

Table 7-1

Table 7-1 shows the short-run cost data of a perfectly competitive firm that produces plastic camera cases. Assume that output can only be increased in batches of 100 units.

-Refer to Table 7-1.The firm will not produce in the short run if the output price falls below

Table 7-1 shows the short-run cost data of a perfectly competitive firm that produces plastic camera cases. Assume that output can only be increased in batches of 100 units.

-Refer to Table 7-1.The firm will not produce in the short run if the output price falls below

Free

(Multiple Choice)

4.8/5  (48)

(48)

Correct Answer: Verified

Verified

D

Which of the following statements is true?

Free

(Multiple Choice)

4.9/5 (39)

Correct Answer:Verified

D

Perfectly competitive firms produce up to the point where the price of the good equals the marginal cost of producing the last unit.This condition is referred to as

Free

(Multiple Choice)

4.7/5 (40)

Correct Answer:Verified

C

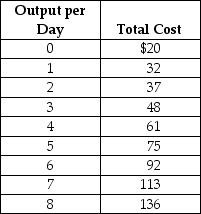

Suppose Veronica sells teapots in the perfectly competitive teapot market.Her output per day and her costs are as follows:

Suppose the current equilibrium price in the teapot market is $10.To maximise profit,how many teapots will Veronica produce,what price will she charge,and how much profit (or loss)will she make? Draw a graph to illustrate your answer.Your graph should include Veronica's demand,ATC,AVC,MC,and MR curves,the price she is charging,the quantity she is producing,and the area representing her profit (or loss).

Suppose the current equilibrium price in the teapot market is $10.To maximise profit,how many teapots will Veronica produce,what price will she charge,and how much profit (or loss)will she make? Draw a graph to illustrate your answer.Your graph should include Veronica's demand,ATC,AVC,MC,and MR curves,the price she is charging,the quantity she is producing,and the area representing her profit (or loss).

(Essay)

4.7/5 (37)

If the market price is $40 in a perfectly competitive market,the marginal revenue from selling the fifth unit is

(Multiple Choice)

4.8/5 (38)

Use a graph to show the demand,AVC,ATC,MC,and MR curves of a firm that should temporarily shut down in the short run.Identify the shutdown point on the graph.

(Essay)

4.8/5 (38)

Using two graphs,illustrate how a positive technological change in the market for notebook computers could eliminate short-run economic profit for a firm in that market.On the first graph,use a supply and demand graph to illustrate the positive technological change.On the second graph,use demand,ATC,MC and MR curves to illustrate the elimination of economic profit resulting from the positive technological change.Explain what is taking place in each graph.

(Essay)

4.8/5 (40)

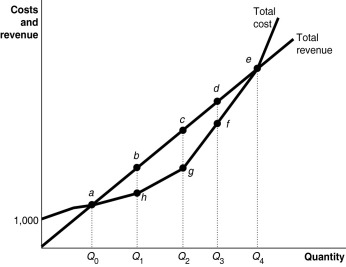

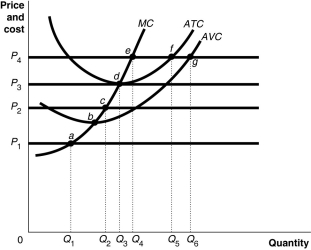

Figure 7-2  -Refer to Figure 7-2.Suppose the firm is currently producing Q2 units.What happens if it expands output to Q3 units?

-Refer to Figure 7-2.Suppose the firm is currently producing Q2 units.What happens if it expands output to Q3 units?

(Multiple Choice)

4.9/5 (39)

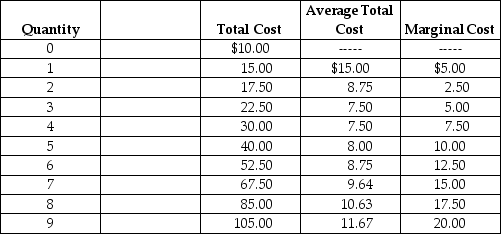

Table 7-2

Arnie sells basketballs in a perfectly competitive market. Table 7-2 summarises Arnie's output per day (Q), total cost (TC), average total cost (ATC) and marginal cost (MC).

-Refer to Table 7-2.What price (P)will Arnie charge and how much profit will he earn if the market price of basketballs is $12.50?

Arnie sells basketballs in a perfectly competitive market. Table 7-2 summarises Arnie's output per day (Q), total cost (TC), average total cost (ATC) and marginal cost (MC).

-Refer to Table 7-2.What price (P)will Arnie charge and how much profit will he earn if the market price of basketballs is $12.50?

(Multiple Choice)

4.9/5 (36)

Figure 7-14  -Refer to Figure 7-14.Which panel best represents the perfectly competitive organic produce market in which some firms are experiencing short-run losses,and consumers are displaying an increased preference for organic produce?

-Refer to Figure 7-14.Which panel best represents the perfectly competitive organic produce market in which some firms are experiencing short-run losses,and consumers are displaying an increased preference for organic produce?

(Multiple Choice)

4.7/5 (38)

Figure 7-7  Figure 7-7 shows cost and demand curves facing a profit-maximising, perfectly competitive firm.

-Refer to Figure 7-7.Identify the firm's short-run supply curve.

Figure 7-7 shows cost and demand curves facing a profit-maximising, perfectly competitive firm.

-Refer to Figure 7-7.Identify the firm's short-run supply curve.

(Multiple Choice)

4.7/5 (41)

In a decreasing-cost industry,the entry of new firms lowers average cost at each level of output.

(True/False)

4.7/5 (41)

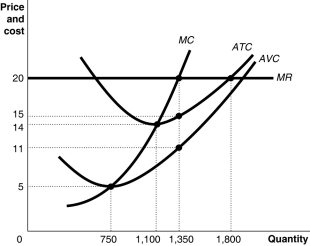

Figure 7-5  Figure 7-5 shows cost and demand curves facing a typical firm in a constant-cost, perfectly competitive industry.

-Refer to Figure 7-5.If the market price is $20,what is the amount of the firm's profit?

Figure 7-5 shows cost and demand curves facing a typical firm in a constant-cost, perfectly competitive industry.

-Refer to Figure 7-5.If the market price is $20,what is the amount of the firm's profit?

(Multiple Choice)

4.9/5 (36)

Figure 7-13  -Refer to Figure 7-13.Assume that the medical screening industry is perfectly competitive and that some firms are incurring short-run losses.Suppose the medical screening industry runs an effective advertising campaign which convinces a large number of people that yearly CT scans are critical for good health.Which of the diagrams in the figure best describes what happens in the industry?

-Refer to Figure 7-13.Assume that the medical screening industry is perfectly competitive and that some firms are incurring short-run losses.Suppose the medical screening industry runs an effective advertising campaign which convinces a large number of people that yearly CT scans are critical for good health.Which of the diagrams in the figure best describes what happens in the industry?

(Multiple Choice)

4.8/5 (36)

A perfectly competitive firm has to charge the same price as every other firm in the market.Therefore,the firm

(Multiple Choice)

4.7/5 (39)

Figure 7-14

-Refer to Figure 7-14.Which panel best represents the perfectly competitive organic produce market in which some firms are earning short-run economic profits,and the Surgeon General announces that switching from non-organic produce to organic produce will add 5 years to the average life span of consumers?

(Multiple Choice)

4.8/5 (38)

Why are individual buyers and sellers in perfect competition called price takers?

(Essay)

5.0/5 (35)

A perfectly competitive firm will maximise its profit at the rate of output where the vertical distance between its total revenue and total cost is the largest.This is the same rate of output where

(Multiple Choice)

4.7/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)