Exam 7: Consumer Choice and Elasticity

Exam 1: Economics: Foundations and Models160 Questions

Exam 2: Trade-Offs, comparative Advantage, and the Market System191 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply241 Questions

Exam 4: Market Efficiency and Market Failure226 Questions

Exam 5: The Economics of Healthcare169 Questions

Exam 6: Firms,the Stock Market,and Corporate Governance255 Questions

Exam 7: Consumer Choice and Elasticity270 Questions

Exam 8: Technology, production, and Costs277 Questions

Exam 9: Firms in Perfectly Competitive Markets351 Questions

Exam 10: Monopoly and Antitrust253 Questions

Exam 11: Monopolistic Competition and Oligopoly304 Questions

Exam 12: GDP: Measuring Total Production and Income200 Questions

Exam 13: Unemployment and Inflation207 Questions

Exam 14: Economic Growth, the Financial System and Business Cycles172 Questions

Exam 15: Aggregate Demand and Aggregate Supply Analysis120 Questions

Exam 16: Money, banks, and the Federal Reserve System139 Questions

Exam 17: Monetary Policy180 Questions

Exam 18: Fiscal Policy131 Questions

Exam 19: Comparative Advantage, international Trade, and Exchange Rates247 Questions

Select questions type

Figure 7-12  -Refer to Figure 7-12.Consider a typical firm in a perfectly competitive industry which is incurring short-run losses.Which of the diagrams in the figure shows the effect on the industry as it transitions to a long-run equilibrium?

-Refer to Figure 7-12.Consider a typical firm in a perfectly competitive industry which is incurring short-run losses.Which of the diagrams in the figure shows the effect on the industry as it transitions to a long-run equilibrium?

(Multiple Choice)

4.8/5  (35)

(35)

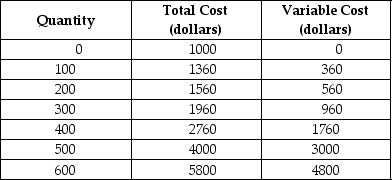

Table 7-1

Table 7-1 shows the short-run cost data of a perfectly competitive firm that produces plastic camera cases. Assume that output can only be increased in batches of 100 units.

-Refer to Table 7-1.If the market price of each camera case is $8 and the firm maximises profit,what is the amount of the firm's profit or loss?

Table 7-1 shows the short-run cost data of a perfectly competitive firm that produces plastic camera cases. Assume that output can only be increased in batches of 100 units.

-Refer to Table 7-1.If the market price of each camera case is $8 and the firm maximises profit,what is the amount of the firm's profit or loss?

(Multiple Choice)

4.9/5 (42)

The short-run supply curve for a perfectly competitive firm is that part of the firm's marginal cost curve that lies above the minimum point of its average variable cost curve.

(True/False)

4.9/5 (43)

In the long run,perfectly competitive firms earn zero economic profit.Why do firms enter an industry when they know that in the long run they will not earn any profit?

(Essay)

4.8/5 (42)

Suppose the equilibrium price in a perfectly competitive industry is $10 and a firm in the industry charges $12.Which of the following will happen?

(Multiple Choice)

4.7/5 (40)

Maximising average profit is equivalent to maximising total profit.

(True/False)

4.8/5 (41)

Which of the following is the best example of a perfectly competitive industry?

(Multiple Choice)

4.9/5 (37)

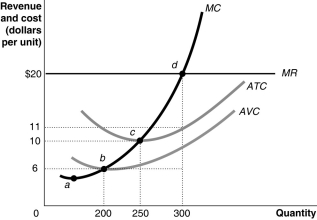

Figure 7-8  -Refer to Figure 7-8.The firm's short-run supply curve is its

-Refer to Figure 7-8.The firm's short-run supply curve is its

(Multiple Choice)

4.8/5 (41)

The perfectly competitive market structure benefits consumers because

(Multiple Choice)

4.8/5 (33)

Marty's Bird House suffers a short-run loss.Marty can reduce his loss below the amount of his total fixed costs by continuing to produce if his revenue

(Multiple Choice)

4.8/5 (47)

If a perfectly competitive firm achieves productive efficiency,then

(Multiple Choice)

4.9/5 (38)

In early 2007,Pioneer and JVC,two Japanese electronics firms,each announced that their profits were going to be lower than expected because they both had to cut prices for LCD and plasma television sets.Which of the following could explain why these firms did not simply raise their prices and increase their profits?

(Multiple Choice)

4.8/5 (27)

Consider the market for wheat which is a perfectly competitive market.Is the market demand curve the same as the demand curve facing an individual producer? If not,explain how and why they are different? Illustrate your answer graphically.

(Essay)

4.8/5 (31)

What is a long-run supply curve? What does a long-run supply curve look like on a perfectly competitive market graph?

(Essay)

4.9/5 (44)

Figure 7-8

-Refer to Figure 7-8.At the profit-maximising output level,the firm earns

(Multiple Choice)

4.8/5 (30)

Assume that firms in a perfectly competitive market are earning economic profits.Which of the following statements describes the change in market price and output as a result of the entry of new firms into this market?

(Multiple Choice)

4.7/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)