Exam 7: Consumer Choice and Elasticity

Exam 1: Economics: Foundations and Models160 Questions

Exam 2: Trade-Offs, comparative Advantage, and the Market System191 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply241 Questions

Exam 4: Market Efficiency and Market Failure226 Questions

Exam 5: The Economics of Healthcare169 Questions

Exam 6: Firms,the Stock Market,and Corporate Governance255 Questions

Exam 7: Consumer Choice and Elasticity270 Questions

Exam 8: Technology, production, and Costs277 Questions

Exam 9: Firms in Perfectly Competitive Markets351 Questions

Exam 10: Monopoly and Antitrust253 Questions

Exam 11: Monopolistic Competition and Oligopoly304 Questions

Exam 12: GDP: Measuring Total Production and Income200 Questions

Exam 13: Unemployment and Inflation207 Questions

Exam 14: Economic Growth, the Financial System and Business Cycles172 Questions

Exam 15: Aggregate Demand and Aggregate Supply Analysis120 Questions

Exam 16: Money, banks, and the Federal Reserve System139 Questions

Exam 17: Monetary Policy180 Questions

Exam 18: Fiscal Policy131 Questions

Exam 19: Comparative Advantage, international Trade, and Exchange Rates247 Questions

Select questions type

A perfectly competitive firm produces 3000 units of a good at a total cost of $36 000.The fixed cost of production is $20 000.The price of each good is $10.Should the firm continue to produce in the short run?

(Multiple Choice)

4.8/5  (34)

(34)

If a perfectly competitive firm's price is above its average total cost,the firm

(Multiple Choice)

4.7/5 (29)

Assume the market for organically-grown produce is perfectly competitive.All else being equal,as farmers find it less profitable to produce and sell organic produce in this market,

(Multiple Choice)

4.7/5 (36)

What is always true at the quantity where a firm's average total cost equals average revenue?

(Multiple Choice)

4.9/5 (33)

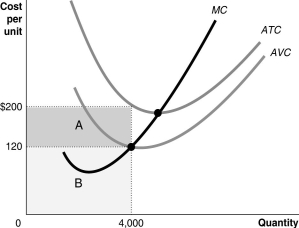

Figure 7-6  -Refer to Figure 7-6.Suppose the firm produces 4000 units.What does the shaded area labelled B represent?

-Refer to Figure 7-6.Suppose the firm produces 4000 units.What does the shaded area labelled B represent?

(Multiple Choice)

4.9/5 (38)

A constant-cost,perfectly competitive market is in long-run equilibrium.At present,there are 1000 firms each producing 400 units of output.The price of the good is $60.Now suppose there is a sudden increase in demand for the industry's product which causes the price of the good to rise to $64.In the new long-run equilibrium,how will the average total cost of producing the good compare to what it was before the price of the good rose?

(Multiple Choice)

4.7/5 (40)

Allocative efficiency is achieved in an industry when firms supply those goods and services that provide consumers with a marginal benefit equal to the marginal cost of producing those goods and services.

(True/False)

4.8/5 (30)

Which of the following does not hold true for a perfectly competitive firm in long-run equilibrium?

(Multiple Choice)

4.8/5 (40)

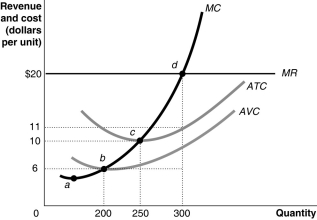

Figure 7-8  -Refer to Figure 7-8.Total revenue at the profit-maximising level of output is

-Refer to Figure 7-8.Total revenue at the profit-maximising level of output is

(Multiple Choice)

4.9/5 (47)

If,for the last bushel of apples produced and sold by an apple farm,marginal revenue exceeds marginal cost,then in producing that bushel the farm

(Multiple Choice)

4.7/5 (35)

For a perfectly competitive firm,average revenue is equal to

(Multiple Choice)

4.8/5 (36)

If price = marginal cost at the output produced by a perfectly competitive firm and the firm is earning an economic profit,then

(Multiple Choice)

4.8/5 (37)

In the short run,a firm that incurs losses might choose to produce rather than shut down if the amount of its revenue is less than its fixed cost.

(True/False)

4.8/5 (40)

In the short run,a firm might choose to produce rather than shut down even if its market price is less than its average total cost of production.

(True/False)

4.9/5 (38)

For a given quantity,the total profit of a perfectly competitive firm is equal to the vertical distance between the firm's total revenue curve and its total cost curve.

(True/False)

4.8/5 (34)

Figure 7-8

-Refer to Figure 7-8.The total cost at the profit-maximising output level equals

(Multiple Choice)

4.8/5 (37)

A perfectly competitive firm produces 3000 units of a good at a total cost of $36 000.The price of each good is $10.Calculate the firm's short-run profit or loss.

(Multiple Choice)

4.8/5 (38)

If a perfectly competitive apple farm's marginal revenue exceeds the marginal cost of the last bushel of apples sold,what should the farm do to maximise its profit?

(Multiple Choice)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)