Exam 7: Consumer Choice and Elasticity

Exam 1: Economics: Foundations and Models160 Questions

Exam 2: Trade-Offs, comparative Advantage, and the Market System191 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply241 Questions

Exam 4: Market Efficiency and Market Failure226 Questions

Exam 5: The Economics of Healthcare169 Questions

Exam 6: Firms,the Stock Market,and Corporate Governance255 Questions

Exam 7: Consumer Choice and Elasticity270 Questions

Exam 8: Technology, production, and Costs277 Questions

Exam 9: Firms in Perfectly Competitive Markets351 Questions

Exam 10: Monopoly and Antitrust253 Questions

Exam 11: Monopolistic Competition and Oligopoly304 Questions

Exam 12: GDP: Measuring Total Production and Income200 Questions

Exam 13: Unemployment and Inflation207 Questions

Exam 14: Economic Growth, the Financial System and Business Cycles172 Questions

Exam 15: Aggregate Demand and Aggregate Supply Analysis120 Questions

Exam 16: Money, banks, and the Federal Reserve System139 Questions

Exam 17: Monetary Policy180 Questions

Exam 18: Fiscal Policy131 Questions

Exam 19: Comparative Advantage, international Trade, and Exchange Rates247 Questions

Select questions type

The demand curve for each seller's product in perfect competition is horizontal at the market price because

(Multiple Choice)

4.8/5  (37)

(37)

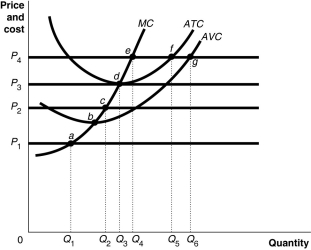

Figure 7-7  Figure 7-7 shows cost and demand curves facing a profit-maximising, perfectly competitive firm.

-Refer to Figure 7-7.At price P2,the firm would

Figure 7-7 shows cost and demand curves facing a profit-maximising, perfectly competitive firm.

-Refer to Figure 7-7.At price P2,the firm would

(Multiple Choice)

4.9/5 (40)

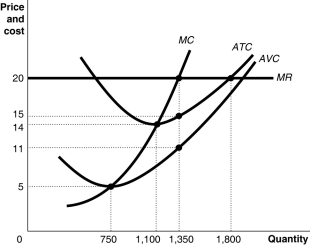

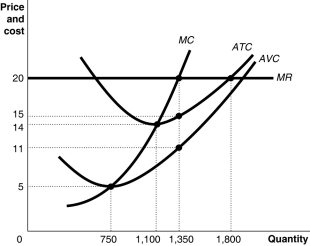

Figure 7-9  -Refer to Figure 7-9.Suppose the prevailing price is $20 and the firm is currently producing 1350 units.In the long-run equilibrium,the firm represented in the diagram

-Refer to Figure 7-9.Suppose the prevailing price is $20 and the firm is currently producing 1350 units.In the long-run equilibrium,the firm represented in the diagram

(Multiple Choice)

4.8/5 (37)

Figure 7-5  Figure 7-5 shows cost and demand curves facing a typical firm in a constant-cost, perfectly competitive industry.

-Refer to Figure 7-5.If the market price is $20,what is the firm's profit-maximising output?

Figure 7-5 shows cost and demand curves facing a typical firm in a constant-cost, perfectly competitive industry.

-Refer to Figure 7-5.If the market price is $20,what is the firm's profit-maximising output?

(Multiple Choice)

5.0/5 (35)

Jason,a high-school student,mows lawns for families in his neighbourhood.The going rate is $12 for each lawn-mowing service.Jason would like to charge $20 because he believes he has more experience mowing lawns than the many other teenagers who also offer the same service.If the market for lawn-mowing services is perfectly competitive,what would happen if Jason raised his price?

(Multiple Choice)

4.7/5 (39)

A perfectly competitive firm in a constant-cost industry produces 3000 units of a good at a total cost of $36 000.The prevailing market price is $15.What will happen to the number of firms in the industry and to the industry's output in the long run?

(Multiple Choice)

4.9/5 (43)

Firms in perfect competition produce the productively efficient output level in the short run and in the long run.

(True/False)

4.9/5 (36)

Assume that the LCD and plasma television set industry is perfectly competitive.Suppose a producer develops a successful innovation that enables it to lower its cost of production.What happens in the short run and in the long run?

(Multiple Choice)

4.8/5 (36)

Figure 7-9

-Refer to Figure 7-9.Suppose the prevailing price is $20 and the firm is currently producing 1350 units.In the long-run equilibrium

(Multiple Choice)

4.8/5 (39)

Figure 7-7 Figure 7-7 shows cost and demand curves facing a profit-maximising, perfectly competitive firm.

-Refer to Figure 7-7.At price P4,the firm would produce

(Multiple Choice)

4.8/5 (34)

If a firm's fixed cost exceeds its total revenue,the firm should stop production by shutting down temporarily.

(True/False)

4.8/5 (46)

What is the difference between 'shutting down temporarily' and 'exiting the industry'?

(Essay)

4.9/5 (29)

A wheat farmer and a firm in a perfectly competitive market are similar in that

(Multiple Choice)

4.9/5 (31)

Assume the market for organic produce sold at farmers' markets is perfectly competitive.All else being equal,as more farmers choose to produce and sell organic produce at farmers' markets,what is likely to happen to the equilibrium price of the produce and profits of the organic farmers in the long run?

(Multiple Choice)

4.8/5 (31)

A perfectly competitive industry achieves allocative efficiency because

(Multiple Choice)

4.9/5 (41)

Which of the following is not an assumption of perfectly competitive markets?

(Multiple Choice)

4.7/5 (39)

Of the following industries,which are perfectly competitive? For those that are not perfectly competitive,explain why.

a.Restaurants

b.Corn

c.University education

d.Local radio and television

(Essay)

4.8/5 (36)

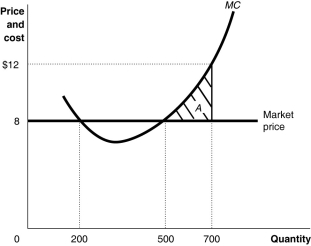

Figure 7-1  -Refer to Figure 7-1.If the firm is producing 700 units,

-Refer to Figure 7-1.If the firm is producing 700 units,

(Multiple Choice)

4.9/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)