Exam 7: Consumer Choice and Elasticity

Exam 1: Economics: Foundations and Models160 Questions

Exam 2: Trade-Offs, comparative Advantage, and the Market System191 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply241 Questions

Exam 4: Market Efficiency and Market Failure226 Questions

Exam 5: The Economics of Healthcare169 Questions

Exam 6: Firms,the Stock Market,and Corporate Governance255 Questions

Exam 7: Consumer Choice and Elasticity270 Questions

Exam 8: Technology, production, and Costs277 Questions

Exam 9: Firms in Perfectly Competitive Markets351 Questions

Exam 10: Monopoly and Antitrust253 Questions

Exam 11: Monopolistic Competition and Oligopoly304 Questions

Exam 12: GDP: Measuring Total Production and Income200 Questions

Exam 13: Unemployment and Inflation207 Questions

Exam 14: Economic Growth, the Financial System and Business Cycles172 Questions

Exam 15: Aggregate Demand and Aggregate Supply Analysis120 Questions

Exam 16: Money, banks, and the Federal Reserve System139 Questions

Exam 17: Monetary Policy180 Questions

Exam 18: Fiscal Policy131 Questions

Exam 19: Comparative Advantage, international Trade, and Exchange Rates247 Questions

Select questions type

The supply curve of a perfectly competitive firm in the short run is

(Multiple Choice)

4.9/5  (38)

(38)

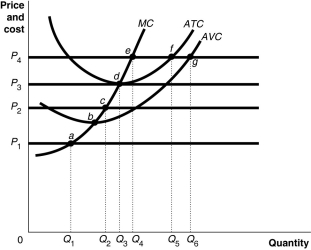

Figure 7-7  Figure 7-7 shows cost and demand curves facing a profit-maximising, perfectly competitive firm.

-Refer to Figure 7-7.At price P1,the firm would

Figure 7-7 shows cost and demand curves facing a profit-maximising, perfectly competitive firm.

-Refer to Figure 7-7.At price P1,the firm would

(Multiple Choice)

4.7/5 (40)

Assume that a perfectly competitive market is in long-run equilibrium.Suppose as a result of a health hazard associated with the industry's product,demand decreases drastically.What is the immediate result of this event?

(Multiple Choice)

4.9/5 (35)

How are market price,average revenue,and marginal revenue related for a perfectly competitive firm and why?

(Essay)

4.9/5 (37)

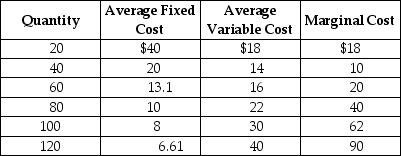

Table 7-3

Table 7-3 shows the short-run cost data of a perfectly competitive firm. Assume that output can only be increased in batches of 20 units.

-Refer to Table 7-3.If the market price is $45 the firm will produce

Table 7-3 shows the short-run cost data of a perfectly competitive firm. Assume that output can only be increased in batches of 20 units.

-Refer to Table 7-3.If the market price is $45 the firm will produce

(Multiple Choice)

4.9/5 (35)

Which of the following offers the best reason why restaurants are not considered to be perfectly competitive firms?

(Multiple Choice)

4.8/5 (43)

A very large number of small sellers who sell identical products implies

(Multiple Choice)

4.8/5 (34)

If a typical firm in a perfectly competitive industry is earning profits,then

(Multiple Choice)

4.9/5 (32)

In a perfectly competitive market,the term 'price taker' applies to

(Multiple Choice)

4.9/5 (34)

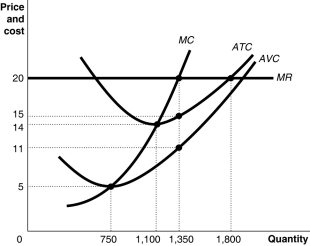

Figure 7-5  Figure 7-5 shows cost and demand curves facing a typical firm in a constant-cost, perfectly competitive industry.

-Refer to Figure 7-5.If the market price is $20,what is the average profit at the profit-maximising quantity?

Figure 7-5 shows cost and demand curves facing a typical firm in a constant-cost, perfectly competitive industry.

-Refer to Figure 7-5.If the market price is $20,what is the average profit at the profit-maximising quantity?

(Multiple Choice)

4.8/5 (39)

If,as a perfectly competitive industry expands,it can supply larger quantities only at a higher long-run equilibrium price,it is

(Multiple Choice)

4.7/5 (37)

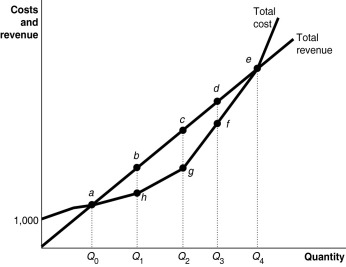

Figure 7-2  -Refer to Figure 7-2.The firm breaks even at an output level of

-Refer to Figure 7-2.The firm breaks even at an output level of

(Multiple Choice)

4.9/5 (47)

For a perfectly competitive firm,at the profit-maximising output,average revenue equals marginal cost.

(True/False)

4.8/5 (41)

Letters are used to represent the terms used to answer this question: price (P),quantity of output (Q),total cost (TC)and average total cost (ATC).Which of the following equations is equal to a firm's profit?

(Multiple Choice)

4.8/5 (40)

What is meant by productive efficiency? How does a perfectly competitive firm achieve productive efficiency?

(Essay)

4.8/5 (46)

After an increase in demand in a constant-cost industry,firms will find themselves with higher average cost curves.

(True/False)

4.8/5 (33)

In long-run perfectly competitive equilibrium,which of the following is false?

(Multiple Choice)

4.9/5 (35)

A perfectly competitive firm breaks even at a price equal to its minimum average total cost.

(True/False)

4.8/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)