Exam 14: Decision Making: Relevant Costs and Benefits

Exam 1: The Changing Role of Managerial Accounting in a Dynamic Business Environment62 Questions

Exam 2: Basic Cost Management Concepts85 Questions

Exam 3: Product Costing and Cost Accumulation in a Batch Production Environment80 Questions

Exam 4: Process Costing and Hybrid Product-Costing Systems84 Questions

Exam 5: Activity-Based Costing and Management85 Questions

Exam 6: Activity Analysis, Cost Behavior, and Cost Estimation93 Questions

Exam 7: Cost-Volume-Profit Analysis89 Questions

Exam 8: Variable Costing and the Costs of Quality and Sustainability64 Questions

Exam 9: Financial Planning and Analysis: the Master Budget95 Questions

Exam 10: Standard Costing and Analysis of Direct Costs80 Questions

Exam 11: Flexible Budgeting and Analysis of Overhead Costs91 Questions

Exam 12: Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard72 Questions

Exam 13: Investment Centers and Transfer Pricing95 Questions

Exam 14: Decision Making: Relevant Costs and Benefits90 Questions

Exam 15: Target Costing and Cost Analysis for Pricing Decisions99 Questions

Exam 16: Capital Expenditure Decisions104 Questions

Exam 17: Allocation of Support Activity Costs and Joint Costs81 Questions

Exam 18: The Sarbanes-Oxley Act, Internal Controls, and Management Accounting14 Questions

Exam 19: Compound Interest and the Concept of Present Value24 Questions

Exam 20: Inventory Management14 Questions

Select questions type

Which of the following costs can be ignored when making a decision?

Free

(Multiple Choice)

4.9/5  (32)

(32)

Correct Answer: Verified

Verified

C

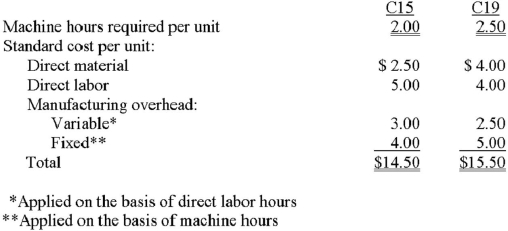

Fowler Industries produces two bearings: C15 and C19. Data regarding these two bearings follow.  The company requires 8,000 units of C15 and 11,000 units of C19. Recently, management decided to devote additional machine time to other product lines, resulting in only 31,000 machine hours per year that can be dedicated to production of the bearings. An outside company has offered to sell Fowler the bearings at prices of $13.50 for C15 and $13.50 for C19.

Required:

A. Assume that Fowler decided to produce all C15s and purchase C19s only as needed. Determine the number of C19s to be purchased.

B. Compute the net benefit to the company of manufacturing (rather than purchasing) a unit of C15. Repeat the calculation for a unit of C19. (Note: in answering this question, do not take into consideration any machine hours constraint).

C. Fowler lacks sufficient machine time to produce all of the C15s and C19s needed. Which component (C15 or C19) should Fowler manufacture first with the limited machine hours available? Why? Be sure to show all supporting computations.

The company requires 8,000 units of C15 and 11,000 units of C19. Recently, management decided to devote additional machine time to other product lines, resulting in only 31,000 machine hours per year that can be dedicated to production of the bearings. An outside company has offered to sell Fowler the bearings at prices of $13.50 for C15 and $13.50 for C19.

Required:

A. Assume that Fowler decided to produce all C15s and purchase C19s only as needed. Determine the number of C19s to be purchased.

B. Compute the net benefit to the company of manufacturing (rather than purchasing) a unit of C15. Repeat the calculation for a unit of C19. (Note: in answering this question, do not take into consideration any machine hours constraint).

C. Fowler lacks sufficient machine time to produce all of the C15s and C19s needed. Which component (C15 or C19) should Fowler manufacture first with the limited machine hours available? Why? Be sure to show all supporting computations.

Free

(Essay)

4.8/5 (45)

Correct Answer:Verified

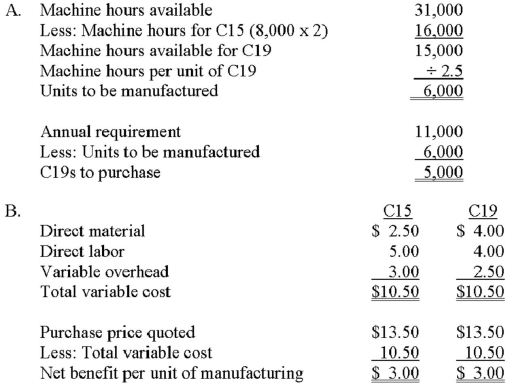

C. C15 consumes 2 hours of machine time, thus providing a net benefit of $1.50 per hour ($3 ÷ 2). In contrast, C19 consumes 2.5 hours of time and produces a benefit of $1.20 per hour ($3 ÷ 2.5). On the basis of this information, the company should focus on C15.

C. C15 consumes 2 hours of machine time, thus providing a net benefit of $1.50 per hour ($3 ÷ 2). In contrast, C19 consumes 2.5 hours of time and produces a benefit of $1.20 per hour ($3 ÷ 2.5). On the basis of this information, the company should focus on C15.

The cost of inventory currently owned by a company is an example of a (n):

Free

(Multiple Choice)

4.8/5 (29)

Correct Answer:Verified

B

Lido manufactures A and B from a joint process (cost = $80,000). Five thousand pounds of A can be sold at split-off for $20 per pound or processed further at an additional cost of $20,000 and then sold for $25 per pound. If Lido decides to process A beyond the split-off point, operating income will:

(Multiple Choice)

5.0/5 (38)

Laredo manufactures Nuts and Bolts from a joint process (cost = $80,000). Five thousand pounds of Nuts can be sold at split-off for $20 per pound; ten thousand pounds of Bolts can be sold at split-off for $15 per pound. For product costing purposes Laredo allocates joint costs using the relative sales value method.

The amount of joint cost allocated to Bolts would be:

(Multiple Choice)

4.9/5 (37)

Cornwall Corporation manufactures faucets. Several weeks ago, the company received a special-order inquiry from Yates, Inc. Yates desires to market a faucet similar to Cornwall's model no. 55 and has offered to purchase 3,000 units. The following data are available:

• Cost data for Cornwall's model no. 55 faucet: direct materials, $45; direct labor, $30 (2 hours at $15 per hour); and manufacturing overhead, $70 (2 hours at $35 per hour).

• The normal selling price of model no. 55 is $180; however, Yates has offered Cornwall only $115 because of the large quantity it is willing to purchase.

• Yates requires a design modification that will allow a $4 reduction in direct-material cost.

• Cornwall's production supervisor notes that the company will incur $8,700 in additional set-up costs and will have to purchase a $3,300 special device to manufacture these units. The device will be discarded once the special order is completed.

• Total manufacturing overhead costs are applied to production at the rate of $35 per labor hour. This figure is based, in part, on budgeted yearly fixed overhead of $624,000 and planned production activity of 24,000 labor hours.

• Cornwall will allocate $5,000 of existing fixed administrative costs to the order as "¼part of the cost of doing business."

Required:

A. One of Cornwall's staff accountants wants to reject the special order because "financially, it's a loser." Do you agree with this conclusion if Cornwall currently has excess capacity? Show calculations to support your answer.

B. If Cornwall currently has no excess capacity, should the order be rejected from a financial perspective? Briefly explain.

C. Assume that Cornwall currently has no excess capacity. Would outsourcing be an option that Cornwall could consider if management truly wanted to do business with Yates? Briefly discuss, citing several key considerations for Cornwall in your answer.

(Essay)

4.9/5 (37)

Product costs incurred after the split-off point in a joint processing environment are called:

(Multiple Choice)

4.9/5 (34)

Lido manufactures A and B from a joint process (cost = $80,000). Ten thousand pounds of B can be sold at split-off for $15 per pound or processed further at an additional cost of $20,000 and later sold for $16. If Lido decides to process B beyond the split-off point, operating income will:

(Multiple Choice)

4.9/5 (38)

A firm that decides to emphasize those goods with the highest contribution margin per unit may have made an incorrect decision when the company has capacity constraints in the form of limited resources.

(True/False)

4.8/5 (40)

Tri-County, Inc. is studying whether to expand operations by adding a new product line. Which of the following choices correctly denotes the costs that should be considered in this decision?

(Multiple Choice)

4.9/5 (39)

The following costs are relevant to the decision situation cited except:

(Multiple Choice)

4.9/5 (42)

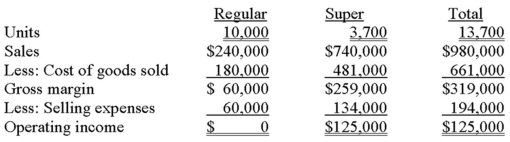

HiTech manufactures two products: Regular and Super. The results of operations for 20x1 follow.  Fixed manufacturing costs included in cost of goods sold amount to $3 per unit for Regular and $20 per unit for Super. Variable selling expenses are $4 per unit for Regular and $20 per unit for Super; remaining selling amounts are fixed.

Disregard the information in the previous question. If HiTech eliminates Regular and uses the available capacity to produce and sell an additional 1,500 units of Super, what would be the impact on operating income?

Fixed manufacturing costs included in cost of goods sold amount to $3 per unit for Regular and $20 per unit for Super. Variable selling expenses are $4 per unit for Regular and $20 per unit for Super; remaining selling amounts are fixed.

Disregard the information in the previous question. If HiTech eliminates Regular and uses the available capacity to produce and sell an additional 1,500 units of Super, what would be the impact on operating income?

(Multiple Choice)

4.9/5 (38)

"It's close to a $40,000 loser and we ought to devote our efforts elsewhere," noted Karenne Whitmore, after reviewing financial reports of her company's attempt to offer a reduced-price daycare service to employees. The daycare's financial figures for the year just ended follow. Revenues \ 120,000 Variable costs 45,000 Traceable fixed costs 89,000 Allocated corporate overhead 24,000

If the daycare service/center is closed, 70% of the traceable fixed cost will be avoided. In addition, the company will incur one-time closure costs of $6,800.

Required:

A. Show calculations that support Whitmore's belief that the daycare center lost almost $40,000.

B. Should the center be closed? Show calculations to support your answer.

C. What problem might the company experience if the center is closed?

(Essay)

4.9/5 (38)

In early July, Jim Lopez purchased a $70 ticket to the December 15 game of the Chicago Titans. (The Titans belong to the Midwest Football League and play their games outdoors on the shore of Lake Michigan.) Parking for the game was expected to cost approximately $22, and Lopez would probably spend another $15 for a souvenir program and food. It is now December 14. The Titans were having a miserable season and the temperature was expected to peak at 5 degrees on game day. Jim is thinking about skipping the game and taking his wife to the movies and dinner, at a cost of $50. The amount of sunk cost that should influence Jim's decision to spend some time with his wife is:

(Multiple Choice)

4.9/5 (37)

Mueller has been approached about providing a new service to its clients. The company will bill clients $140 per hour; the related hourly variable and fixed operating costs will be $75 and $18, respectively. If all employees are currently working at full capacity on other client matters, the per-hour opportunity cost of being unable to provide this new service is:

(Multiple Choice)

4.9/5 (40)

Smythe Manufacturing has 27,000 labor hours available for producing X and Y. Consider the following information: Product X Product Y Required labor time per unit (hours) 2 3 Maximum demand (units) 6,000 8,000 Contribution margin per unit \ 5.00 \ 6.00 Contribution margin per labor hour \ 2.50 \ 2.00 If Smythe follows proper managerial accounting practices, which of the following production schedules should the company set? Product X Product Y A. 0 units 8,000 units B. 1,500 units 8,000 units C. 6,000 units 0 units D. 6,000 units 5,000 units E. 6,000 units 8,000 units

(Multiple Choice)

4.9/5 (38)

An architecture firm currently offers services that appeal to both individuals and commercial clients. If the firm decides to discontinue services to individuals because of ongoing losses, which of the following costs could the company likely avoid?

(Multiple Choice)

5.0/5 (38)

Gorski Corporation manufactures parts that are used in the production of washers and dryers. The following costs are associated with part no. 65: Direct materials \ 50 Direct labor 19 Variable manufacturing overhead 22 Fixed manufacturing overhead 15 Variable selling costs 11 The company received a special-order inquiry from an appliance manufacturer in Spain for 15,000 units of part no. 65. Only $3 of fixed manufacturing will be incurred on the order, and the variable selling costs per unit will amount to only $5. Since Gorski has excess capacity, the minimum price that Gorski should charge the Spanish manufacturer is:

(Multiple Choice)

4.9/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)