Exam 14: Decision Making: Relevant Costs and Benefits

Exam 1: The Changing Role of Managerial Accounting in a Dynamic Business Environment62 Questions

Exam 2: Basic Cost Management Concepts85 Questions

Exam 3: Product Costing and Cost Accumulation in a Batch Production Environment80 Questions

Exam 4: Process Costing and Hybrid Product-Costing Systems84 Questions

Exam 5: Activity-Based Costing and Management85 Questions

Exam 6: Activity Analysis, Cost Behavior, and Cost Estimation93 Questions

Exam 7: Cost-Volume-Profit Analysis89 Questions

Exam 8: Variable Costing and the Costs of Quality and Sustainability64 Questions

Exam 9: Financial Planning and Analysis: the Master Budget95 Questions

Exam 10: Standard Costing and Analysis of Direct Costs80 Questions

Exam 11: Flexible Budgeting and Analysis of Overhead Costs91 Questions

Exam 12: Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard72 Questions

Exam 13: Investment Centers and Transfer Pricing95 Questions

Exam 14: Decision Making: Relevant Costs and Benefits90 Questions

Exam 15: Target Costing and Cost Analysis for Pricing Decisions99 Questions

Exam 16: Capital Expenditure Decisions104 Questions

Exam 17: Allocation of Support Activity Costs and Joint Costs81 Questions

Exam 18: The Sarbanes-Oxley Act, Internal Controls, and Management Accounting14 Questions

Exam 19: Compound Interest and the Concept of Present Value24 Questions

Exam 20: Inventory Management14 Questions

Select questions type

St. Joseph Hospital has been hit with a number of complaints about its food service from patients, employees, and cafeteria customers. These complaints, coupled with a very tight local labor market, have prompted the organization to contact Nationwide Institutional Food Service (NIFS) about the possibility of an outsourcing arrangement.

The hospital's business office has provided the following information for food service for the year just ended: food costs, $890,000; labor, $85,000; variable overhead, $35,000; allocated fixed overhead, $60,000; and cafeteria net income, $80,000.

Conversations with NIFS personnel revealed the following information:

• NIFS will charge St. Joseph Hospital $14 per day for each patient served. Note: This figure has been "marked up" by NIFS to reflect the firm's cost of operating the hospital cafeteria.

• St. Joseph's 250-bed facility operates throughout the year and typically has an average occupancy rate of 70%.

• Labor is the primary driver for variable overhead. If an outsourcing agreement is reached, hospital labor costs will drop by 90%. NIFS plans to use St. Joseph facilities for meal preparation.

• Cafeteria net income is expected to increase by 15% because NIFS will offer an improved menu selection.

Required:

A. What is meant by the term "outsourcing"?

B. Should St. Joseph outsource its food-service operation to NIFS?

C. What factors, other than dollars, should St. Joseph consider before making the final decision?

(Essay)

4.8/5  (30)

(30)

Fester Company is considering whether to sell Retox at the split-off point or subject it to further processing and produce a more refined product known as Retox-F. Consider the following items:

I. The selling price of Retox-F.

II. The joint processing cost of Retox.

III. The separable cost of producing Retox-F.

Which of the above items is (are) relevant to Foster's decision to process Retox into Retox-F?

(Multiple Choice)

4.7/5 (36)

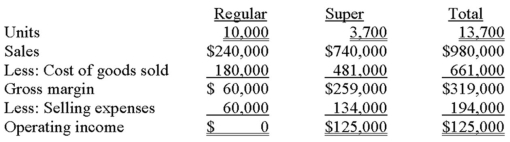

HiTech manufactures two products: Regular and Super. The results of operations for 20x1 follow.  Fixed manufacturing costs included in cost of goods sold amount to $3 per unit for Regular and $20 per unit for Super. Variable selling expenses are $4 per unit for Regular and $20 per unit for Super; remaining selling amounts are fixed.

HiTech wants to drop the Regular product line. If the line is dropped, company-wide fixed manufacturing costs would fall by 10% because there is no alternative use of the facilities. What would be the impact on operating income if Regular is discontinued?

Fixed manufacturing costs included in cost of goods sold amount to $3 per unit for Regular and $20 per unit for Super. Variable selling expenses are $4 per unit for Regular and $20 per unit for Super; remaining selling amounts are fixed.

HiTech wants to drop the Regular product line. If the line is dropped, company-wide fixed manufacturing costs would fall by 10% because there is no alternative use of the facilities. What would be the impact on operating income if Regular is discontinued?

(Multiple Choice)

4.8/5 (35)

Allegiance, Inc. has $125,000 of inventory that suffered minor smoke damage from a fire in the warehouse. The company can sell the goods "as is" for $45,000; alternatively, the goods can be cleaned and shipped to the firm's outlet center at a cost of $23,000. There the goods could be sold for $80,000. What alternative is more desirable and what is the relevant cost for that alternative?

(Multiple Choice)

4.8/5 (51)

A trade-off in a decision situation sometimes occurs between information:

(Multiple Choice)

4.8/5 (41)

Ortega Interiors provides design services to residential and commercial clients. The residential services produce a contribution margin of $450,000 and have traceable fixed operating costs of $480,000. Management is studying whether to drop the residential operation. If closed, the fixed operating costs will fall by $370,000 and Ortega's income will:

(Multiple Choice)

4.8/5 (45)

Riverside Company manufactures G and H in a joint process. The joint costs amount to $80,000 per batch of finished goods. Each batch yields 20,000 liters, of which 40% are G and 60% are H. The selling price of G is $8.75 per liter, and the selling price of H is $15.00 per liter.

Required:

A. If the joint costs are allocated on the basis of the products' sales value at the split-off point, what amount of joint cost will be charged to each product?

B. Riverside has discovered a new process by which G can be refined into Product GG, which has a sales price of $12 per liter. This additional processing would increase costs by $2.10 per liter. Assuming there are no other changes in costs, should the company use the new process? Show calculations.

(Essay)

4.8/5 (32)

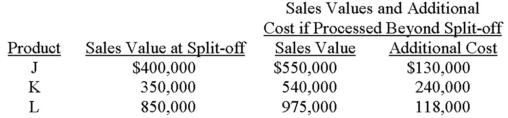

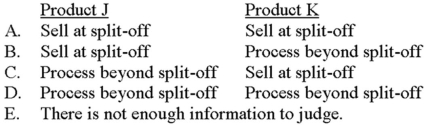

Stoffers Corporation manufactures products J, K, and L in a joint process. The company incurred $480,000 of joint processing costs during the period just ended and had the following data that related to production:  An analysis revealed that all costs incurred after the split-off point are variable and directly traceable to the individual product line.

Required:

A. If Stoffers allocates joint costs on the basis of the products' sales values at the split-off point, what amount of joint cost would be allocated to product J?

B. If production of J totaled 50,000 gallons for the period, determine the relevant cost per gallon that should be used in decisions that explore whether to sell at the split-off point or process further? Briefly explain your answer.

C. At the beginning of the current year, Stoffers decided to process all three products beyond the split-off point. If the company desired to maximize income, did it err in regards to its decision with product J? Product K? Product L? By how much?

An analysis revealed that all costs incurred after the split-off point are variable and directly traceable to the individual product line.

Required:

A. If Stoffers allocates joint costs on the basis of the products' sales values at the split-off point, what amount of joint cost would be allocated to product J?

B. If production of J totaled 50,000 gallons for the period, determine the relevant cost per gallon that should be used in decisions that explore whether to sell at the split-off point or process further? Briefly explain your answer.

C. At the beginning of the current year, Stoffers decided to process all three products beyond the split-off point. If the company desired to maximize income, did it err in regards to its decision with product J? Product K? Product L? By how much?

(Essay)

4.9/5 (38)

Laredo manufactures Nuts and Bolts from a joint process (cost = $80,000). Five thousand pounds of Nuts can be sold at split-off for $20 per pound; ten thousand pounds of Bolts can be sold at split-off for $15 per pound. For product costing purposes Laredo allocates joint costs using the relative sales value method.

The amount of joint cost allocated to Nuts would be:

(Multiple Choice)

4.7/5 (40)

A factory that makes a part has significant idle capacity. The factory's opportunity cost of making this part is equal to:

(Multiple Choice)

5.0/5 (33)

Summers Corporation is composed of five divisions. Each division is allocated a share of Summers's overhead to make divisional managers aware of the cost of running the corporate headquarters. The following information relates to the Metro Division: Sales \ 7,500,000 Variable operating costs 5,100,000 Traceable fixed operating costs 1,900,000 Allocated corporate overhead 300,000 If the Metro Division is closed, 100% of the traceable fixed operating costs can be eliminated. What will be the impact on Summers's overall profitability if the Metro Division is closed?

(Multiple Choice)

4.8/5 (35)

Waltherboro Company recently discontinued the manufacture of product J15. The standard costs for this product were: Direct material \ 50 Direct labor 20 Variable overhead 14 Fixed overhead 35 Total \1 19

There are 800 units of this product in finished-goods inventory. The units are technologically obsolete, and the following alternatives are being considered:

1. Dispose of as scrap. The proceeds from the sale will equal the cost of transportation to the disposal site.

2. Sell to an exporter for sale in a developing country. The sales price to the exporter would be $12 per unit.

3. Remanufacture the products to convert them into model J16, a model that normally sells for $200. The additional cost to convert the J15 units would be $45; the standard cost to manufacture J16 is $125. Presently, there is sufficient capacity to manufacture product J16 directly or to do the necessary conversion work on J15.

Required:

A. Determine the current carrying value of the J15 inventory.

B. Evaluate each alternative and determine the financial benefit to Waltherboro if the alternative is pursued.

(Essay)

4.9/5 (40)

Two months ago, Victory Corporation purchased 4,500 pounds of Hydrol, paying $15,300. The demand for this product has been very strong since the acquisition, with the market price jumping to $4.05 per pound. (Victory can buy or sell Hydrol at this price.) The company recently received a special-order inquiry, one that would require the use of 4,200 pounds of Hydrol. Which of the following is (are) relevant in deciding whether to accept the special order?

(Multiple Choice)

4.9/5 (36)

Occular is studying whether to drop a product because of ongoing losses. Costs that would be relevant in this situation would include variable manufacturing costs as well as:

(Multiple Choice)

4.9/5 (44)

A firm that decides to emphasize those goods with the highest contribution margin per unit may have made an incorrect decision when the company:

(Multiple Choice)

4.8/5 (39)

Smythe Manufacturing has 27,000 labor hours available for producing X and Y. Consider the following information:  If Smythe follows proper managerial accounting practices, how many units of Product X should it produce?

If Smythe follows proper managerial accounting practices, how many units of Product X should it produce?

(Multiple Choice)

5.0/5 (46)

Indiana Corporation has $200,000 of joint processing costs and is studying whether to process J and K beyond the split-off point. Information about J and K follows.  If Indiana desires to maximize total company income, what should the firm do with regard to Products J and K?

If Indiana desires to maximize total company income, what should the firm do with regard to Products J and K?

(Multiple Choice)

4.8/5 (40)

The concept of a relevant cost can be defined as a past cost that differs among alternatives.

(True/False)

4.8/5 (39)

Johnstone Company makes two products: Carpet Kleen and Floor Deodorizer. Operating information from the previous year follows. Carpet Kleen Floor Deodorizer Units produced and sold 5,000 4,000 Machine hours used 5,000 2,000 Sales price per unit \ 7 \ 10 Variable cost per unit \ 4 \ 8 Fixed costs of $20,000 per year are presently allocated equally between both products. If the product mix were to change, total fixed costs would remain the same.

The contribution margin per machine hour for Floor Deodorizer is:

(Multiple Choice)

4.8/5 (34)

Laredo manufactures Nuts and Bolts from a joint process (cost = $80,000). Five thousand pounds of Nuts can be sold at split-off for $20 per pound; ten thousand pounds of Bolts can be sold at split-off for $15 per pound. For product costing purposes Laredo allocates joint costs using the relative sales value method.

The amount of joint cost allocated to Nuts and Bolts, respectively, would be:

(Multiple Choice)

4.9/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)