Exam 11: Flexible Budgeting and Analysis of Overhead Costs

Exam 1: The Changing Role of Managerial Accounting in a Dynamic Business Environment62 Questions

Exam 2: Basic Cost Management Concepts85 Questions

Exam 3: Product Costing and Cost Accumulation in a Batch Production Environment80 Questions

Exam 4: Process Costing and Hybrid Product-Costing Systems84 Questions

Exam 5: Activity-Based Costing and Management85 Questions

Exam 6: Activity Analysis, Cost Behavior, and Cost Estimation93 Questions

Exam 7: Cost-Volume-Profit Analysis89 Questions

Exam 8: Variable Costing and the Costs of Quality and Sustainability64 Questions

Exam 9: Financial Planning and Analysis: the Master Budget95 Questions

Exam 10: Standard Costing and Analysis of Direct Costs80 Questions

Exam 11: Flexible Budgeting and Analysis of Overhead Costs91 Questions

Exam 12: Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard72 Questions

Exam 13: Investment Centers and Transfer Pricing95 Questions

Exam 14: Decision Making: Relevant Costs and Benefits90 Questions

Exam 15: Target Costing and Cost Analysis for Pricing Decisions99 Questions

Exam 16: Capital Expenditure Decisions104 Questions

Exam 17: Allocation of Support Activity Costs and Joint Costs81 Questions

Exam 18: The Sarbanes-Oxley Act, Internal Controls, and Management Accounting14 Questions

Exam 19: Compound Interest and the Concept of Present Value24 Questions

Exam 20: Inventory Management14 Questions

Select questions type

A flexible budget for 15,000 hours revealed variable manufacturing overhead of $90,000 and fixed manufacturing overhead of $120,000. The budget for 25,000 hours would reveal total overhead costs of $210,000.

(True/False)

4.9/5  (35)

(35)

Sussex Company uses a standard cost system and prepared the following budget for May when 24,000 machine hours of activity were anticipated: variable overhead, $48,000; fixed overhead: $240,000. Actual data for May were:

Standard machine hours allowed for output attained: 25,000

Actual machine hours worked: 24,000

Variable overhead incurred: $50,000

Fixed overhead incurred: $250,000

The standard variable overhead rate for May is:

(Multiple Choice)

4.8/5 (34)

Herman Company, which applies overhead to production on the basis of machine hours, reported the following data for the period just ended:

Actual units produced: 13,000

Actual fixed overhead incurred: $742,000

Standard fixed overhead rate: $15 per hour

Budgeted fixed overhead: $720,000

Planned level of machine-hour activity: 48,000

If Herman estimates four hours to manufacture a completed unit, the company's fixed-overhead budget variance would be:

(Multiple Choice)

4.8/5 (42)

Hempstead Corporation plans to manufacture 8,000 units over the next month at the following costs: direct materials, $480,000; direct labor, $60,000; variable manufacturing overhead, $150,000; straight-line depreciation, $24,000, and other fixed manufacturing overhead, $272,000. The result is total budgeted cost of $990,000.

Shortly after the conclusion of the month, Hempstead reported the following costs: Direct materials used \ 490,500 Direct labor 69,600 Variable manufacturing overhead 132,000 Depreciation 24,000 Other fixed manufacturing overhead 272,000 Total 988,100

Howard Krueger and his crews turned out 7,200 units-a remarkable feat given that the company's manufacturing plant was closed for several days because of blizzards and impassable roads. Krueger was especially pleased with the fact that total actual costs were less than budget. He was thus very surprised when Hempstead's general manager expressed unhappiness about the plant's financial performance.

Required:

A. Prepare a performance report that fairly compares budgeted and actual costs for the period just ended-namely, the report that the general manager likely used when assessing performance.

B. Should Krueger be praised for "having met the budget" or is the general manager's unhappiness justified? Explain, citing any apparent problems for the firm.

(Essay)

4.9/5 (33)

The following selected information was extracted from the accounting records of Austin, Inc.:

Planned manufacturing activity: 40,000 machine hours

Standard variable-overhead rate per machine hour: $16

Budgeted fixed overhead: $100,000

Variable-overhead spending variance: $92,000U

Variable-overhead efficiency variance: $102,000F

Fixed-overhead budget variance: $25,000U

Total actual overhead: $675,000

Required:

Determine the following: actual fixed overhead, actual variable overhead, actual machine hours worked, standard machine hours allowed for actual production, and the fixed-overhead volume variance.

(Essay)

4.8/5 (35)

Bavaria's budget for variable overhead and fixed overhead revealed the following information for an anticipated 40,000 hours of activity: variable overhead, $348,000; fixed overhead, $600,000.

The company actually worked 43,000 hours, and actual overhead incurred was: variable, $365,500; fixed, $608,000.

Required:

A. Compute the company's total cost variance for variable overhead and fixed overhead if the firm uses a static budget to help assess performance.

B. Repeat part "A" assuming the use of a flexible budget.

C. Which of the two budgets (static or flexible) is preferred for performance evaluations? Why?

(Essay)

4.9/5 (42)

Draco, Inc. has the following overhead standards:

Variable overhead: 4 hours at $8 per hour

Fixed overhead: 4 hours at $10 per hour

The standards were based on a planned activity of 20,000 machine hours when 5,000 units were scheduled for production. Actual data follow.

Variable overhead incurred: $167,750

Fixed overhead incurred: $210,000

Machine hours worked: 19,800

Actual units produced: 5,100

Draco's fixed-overhead budget variance is:

(Multiple Choice)

5.0/5 (42)

A flexible budget for 15,000 hours revealed variable manufacturing overhead of $90,000 and fixed manufacturing overhead of $120,000. The budget for 20,000 hours would reveal total overhead costs of:

(Multiple Choice)

4.8/5 (34)

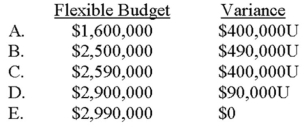

Sand Box Company is choosing new cost drivers for its accounting system. One driver is labor hours; the other is a combination of machine hours for unit variable costs and number of setups for a pool of batch-level costs. Data for the past year follow. Budget Actual Labor hours 200,000 200,000 Machine hours 360,000 450,000 Number of setups 3,000 3,300 Unit variable cost pool \ 1,600,000 \ 2,000,000 Batch-level cost pool \ 900,000 \ 990,000 Assume that both cost pools are combined into a single pool, and labor hours is the driver. The total flexible budget for the actual level of labor hours and the total variance for the combined pool are:

(Multiple Choice)

4.8/5 (44)

The difference between budgeted fixed manufacturing overhead and the fixed overhead applied to production is the:

(Multiple Choice)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)