Exam 11: Flexible Budgeting and Analysis of Overhead Costs

Exam 1: The Changing Role of Managerial Accounting in a Dynamic Business Environment62 Questions

Exam 2: Basic Cost Management Concepts85 Questions

Exam 3: Product Costing and Cost Accumulation in a Batch Production Environment80 Questions

Exam 4: Process Costing and Hybrid Product-Costing Systems84 Questions

Exam 5: Activity-Based Costing and Management85 Questions

Exam 6: Activity Analysis, Cost Behavior, and Cost Estimation93 Questions

Exam 7: Cost-Volume-Profit Analysis89 Questions

Exam 8: Variable Costing and the Costs of Quality and Sustainability64 Questions

Exam 9: Financial Planning and Analysis: the Master Budget95 Questions

Exam 10: Standard Costing and Analysis of Direct Costs80 Questions

Exam 11: Flexible Budgeting and Analysis of Overhead Costs91 Questions

Exam 12: Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard72 Questions

Exam 13: Investment Centers and Transfer Pricing95 Questions

Exam 14: Decision Making: Relevant Costs and Benefits90 Questions

Exam 15: Target Costing and Cost Analysis for Pricing Decisions99 Questions

Exam 16: Capital Expenditure Decisions104 Questions

Exam 17: Allocation of Support Activity Costs and Joint Costs81 Questions

Exam 18: The Sarbanes-Oxley Act, Internal Controls, and Management Accounting14 Questions

Exam 19: Compound Interest and the Concept of Present Value24 Questions

Exam 20: Inventory Management14 Questions

Select questions type

The manufacturing overhead applied to Work-in-Process Inventory by a company that uses standard costing would be computed as:

(Multiple Choice)

4.8/5  (40)

(40)

Riskless Insurance uses budgets to forecast and monitor overhead throughout the organization. The following budget formula relates to the processing of applications for automobile policies in any given month:

Total overhead = $6.80APH + $13,500

where APH = application processing hours

The typical automobile insurance policy has an estimated processing time of 1.5 hours.

During June, management originally anticipated that 320 applications would be processed. Activity was lower than expected, with only 280 applications completed by month-end, and the following costs were incurred: variable overhead, $2,950; fixed overhead, $13,700.

Required:

A. What volume level of applications and processing hours would have been used if Sitka had constructed a static budget?

B. Construct a flexible budget that shows the expected monthly variable and fixed overhead costs of processing 270, 300, and 330 applications.

C. From a cost perspective, did the company perform better or worse than anticipated in June? Show calculations to support your answer.

(Essay)

4.9/5 (40)

Draco, Inc. has the following overhead standards:

Variable overhead: 4 hours at $8 per hour

Fixed overhead: 4 hours at $10 per hour

The standards were based on a planned activity of 20,000 machine hours when 5,000 units were scheduled for production. Actual data follow.

Variable overhead incurred: $167,750

Fixed overhead incurred: $210,000

Machine hours worked: 19,800

Actual units produced: 5,100

Draco's variable-overhead spending variance is:

(Multiple Choice)

4.8/5 (31)

A production manager was recently given a performance report that showed a sizable unfavorable variable-overhead efficiency variance. The manager was puzzled as to how the department could be inefficient in the use/incurrence of this cost.

Required:

Briefly explain the nature of this variance to the manager. Does the variance really have much to do with variable overhead efficiencies or inefficiencies? Discuss.

(Essay)

4.8/5 (42)

Alexandria Corporation applies fixed manufacturing overhead to production on the basis of machine hours worked. The following data relate to the month just ended:

Actual fixed overhead incurred: $1,245,000

Budgeted fixed overhead: $1,200,000

Anticipated machine hours: 240,000

Standard machine hours per finished unit: 8

Actual finished units completed: 31,250

Required:

A. Compute Alexandria's standard fixed-overhead rate per machine hour.

B. Determine Alexandria's fixed-overhead budget variance and fixed-overhead volume variance.

C. Calculate the amount of fixed overhead applied to production.

D. Consider the two events that follow and determine whether the event will affect the fixed-overhead budget variance, the fixed-overhead volume variance, both variances, or neither variance. Assume that Alexandria has not yet revised its standards to reflect these events if a revision is warranted.

1. A raw material shortage halted production for two days.

2. An additional assembly-line supervisor was hired at the beginning of the month.

(Essay)

4.8/5 (34)

What is the most common treatment of the fixed-overhead budget variance at the end of the accounting period?

(Multiple Choice)

4.8/5 (34)

Bushnell, Inc. has a standard variable overhead rate of $4 per machine hour, with each completed unit expected to take three machine hours to produce. A review of the company's accounting records found the following:

Actual variable overhead: $210,000

Variable-overhead efficiency variance: $18,000U

Variable-overhead spending variance: $30,000F

How many units did Bushnell actually produce during the period?

(Multiple Choice)

4.9/5 (39)

Jackson Corporation uses a standard cost system, applying manufacturing overhead on the basis of machine hours. The company's overhead standards per unit are shown below.

Variable overhead: 4 hours at $9 per hour

Fixed overhead: 4 hours at $6* per hour

*Based on planned monthly activity of 120,000 machine hours

Actual data for May were:

Number of units produced: 29,000

Number of machine hours worked: 125,000

Variable overhead costs incurred: $1,085,000

Fixed overhead costs incurred: $755,000

Required:

A. Calculate the spending and efficiency variances for variable overhead.

B. Calculate the budget and volume variances for fixed overhead.

(Essay)

4.9/5 (36)

In an effort to reduce record-keeping, companies that sell perishable goods will often enter the standard cost of direct material, direct labor, and manufacturing overhead directly into what account?

(Multiple Choice)

4.8/5 (37)

Robert Company, which applies overhead to production on the basis of machine hours, reported the following data for the period just ended:

Actual units produced: 12,000

Actual variable overhead incurred: $77,700

Actual machine hours worked: 18,800

Standard variable overhead cost per machine hour: $4.50

If Robert estimates 1.5 hours to manufacture a completed unit, the company's variable-overhead spending variance is:

(Multiple Choice)

4.9/5 (23)

The activity measure selected for use in a variable- and fixed-overhead flexible budget:

(Multiple Choice)

4.8/5 (38)

Briefly describe the procedures that are used to apply manufacturing overhead to production for companies that use (1) normal costing systems and (2) those that use standard costing systems.

(Essay)

5.0/5 (27)

Draco, Inc. has the following overhead standards:

Variable overhead: 4 hours at $8 per hour

Fixed overhead: 4 hours at $10 per hour

The standards were based on a planned activity of 20,000 machine hours when 5,000 units were scheduled for production. Actual data follow.

Variable overhead incurred: $167,750

Fixed overhead incurred: $210,000

Machine hours worked: 19,800

Actual units produced: 5,100

Draco's fixed-overhead volume variance is:

(Multiple Choice)

4.9/5 (41)

Martin Company, which applies overhead to production on the basis of machine hours, reported the following data for the period just ended:

Actual units produced: 9,000

Actual variable overhead incurred: $54,400

Actual machine hours worked: 16,000

Standard variable overhead cost per machine hour: $3.50

If Martin estimates two hours to manufacture a completed unit, the company's variable-overhead efficiency variance is:

(Multiple Choice)

4.9/5 (40)

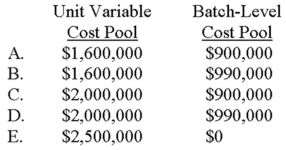

Sand Box Company is choosing new cost drivers for its accounting system. One driver is labor hours; the other is a combination of machine hours for unit variable costs and number of setups for a pool of batch-level costs. Data for the past year follow. Budget Actual Labor hours 200,000 200,000 Machine hours 360,000 450,000 Number of setups 3,000 3,300 Unit variable cost pool \ 1,600,000 \ 2,000,000 Batch-level cost pool \ 900,000 \ 990,000 Assume that the two separate pools are used. The flexible budget dollar amounts for the actual level of machine hours and actual number of setups are:

(Multiple Choice)

4.8/5 (45)

Briefly explain the nature of the fixed-overhead volume variance. Be sure to address the issue of capacity utilization in your response.

(Essay)

4.9/5 (32)

Which of the following statements is/are correct concerning the application of overhead in a standard costing system driven by process hours?

(Multiple Choice)

4.9/5 (29)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)